In defence of active investing

With the emergence in recent years of passive Exchange traded funds (ETFs) a ferocious contest has developed between those pushing the virtues of passive investing, and those defending the craft of active investing.

As the passive investing industry has swelled the companies delivering the products have grown assets under management exponentially to become multinational behemoths supported by well-trained sales representatives with rote-learned statistics at the ready to criticise the active fund managers as soon as a moment of vulnerability arises.

In this Wire, I will attempt to bring to the surface a few underappreciated pieces of information investors should contemplate when looking to build a portfolio of passive and active exposures.

Is active, active?

When looking at an active fund, investors need to investigate the fund managers investment strategy and portfolio exposures. The question is whether those funds categorised as active funds are truly active? For many so-called ‘active’ managers their portfolio exposures closely replicate index weightings with only a small fraction of positions being truly active in its asset allocation.

The problem is that while the industry has evolved many firms haven’t. Many firms categorised as active funds are really passive funds masquerading as active funds due either to historical misclassification or (let’s face it) pursuit of higher fees.

The simple argument is that many fund managers categorised as being active are not true active funds yet get included and caught up as active in the statistics.

We hold these truths to be self-evident, that all active funds are created equal… Hang on!

There is a tendency to lump all active managers together as though everyone’s created equal. In actual fact, not all active managers are the same. Sure, some fund managers will have the sole focus of making as much money as possible for their investors. However, others adhere to a different mandate whether that be a pursuit an income, or the most stable risk-adjusted return possible.

When looking at active funds the portfolio risk and volatility need to be considered. At times lower returns are a reflection of lower risk and risk aversion. Some active fund managers will willingly sacrifice returns compared to index in order to reduce risk.

Active doesn’t necessarily imply an active pursuit of outperformance in returns. Some fund managers will actively seek to outperform a certain indices ‘risk’ by delivering a higher Sharpe Ratio for instance. Something like that won’t be captured in a pure return comparison.

Like a fine wine

When the analysis focuses on those funds that have been around for a longer period of time the performance of active funds relative to the index improves considerably.

It’s not uncommon is some markets for the majority of active funds that have been around for 3-5 years to outperform their benchmarks on a rolling five-year basis.

There is also good evidence that managers who perform well over the longer-term can experience significant periods of underperformance in the short term.

Many of the new funds that come to market haven’t necessarily been given sufficient time to build a track record and develop performance yet nevertheless are included in the analysis of passive and active funds. With the exception of the occasional blow-up, is there really any point measuring a fund with a 3-5-year investment horizon after only 12 months?

The Case of the Disappearing Funds

Often the analysis examining the performance of active funds compared to the index makes the assumption that any fund which has closed or been merged into another fund has underperformed. Although most funds that close or merge have indeed underperformed, not all have. As such accounting for these properly would improve the numbers for active fund managers.

A Fair Comparison

In today’s world, the easiest way to gain exposure to an index is via ETFs. As an investor however you must consider that although ETFs are cheap, they aren’t free. Assuming a 0.50% annual fee for passive NASDAQ exposure, over a 20-year period that passive fund will have an underperformance against the benchmark of approx. 9.50%.

So, while many active funds may have underperformed the index, 100% of passive funds will underperform. The fair comparison, therefore, is not active funds versus the market index, rather the performance of active funds versus an index ETFs.

Is bigger better?

Index investing based on a market capitalisation is by definition simplistic, catering for the investor who unapologetically has no interest in understanding a business or trying to value it. As we see it the major risk is that as momentum builds in index ETF investing an unavoidable divergence develops between stock prices and fundamental valuations.

From our perspective blindly investing more money into one company over another company simply because it’s ‘bigger’ is fraught with danger.

Investors aren’t drawing on anything to distinguish between good companies and bad companies. Bad company’s get rewarded just as much as good companies.

Our fear is that investors who herd together and oversimplify the inherently complex exercise of investing, after an initial period of success, may find themselves in one of the following situations:

- Overexposed to a single sector that has outperformed and become overvalued (think the NASDAQ).

- Overexposed to a single sector that has underperformed and unlikely to experience a meaningful change of fortune (think the ASX 200).

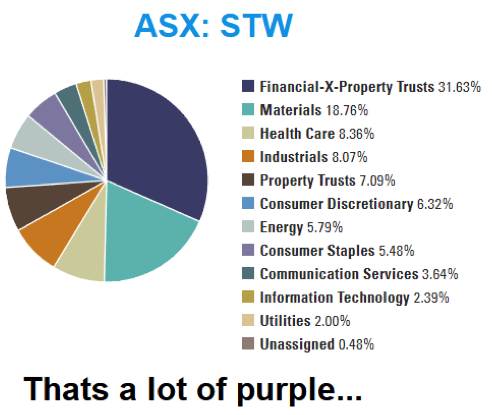

ASX 200 Passive Exposure (ASX: STW)

Let’s take a look at a real-world example. The ASX: STW will seek to closely match the performance of the ASX 200 which given the narrow breadth of the ASX means a heavy weighting towards the largest 20 business on the ASX.

The ASX top 20 has been a consistent underperformer in recent years. We’d argue there is a very good reason for this. As discussed in a previous wire ‘Old-world’ versus the ‘new age’, most of the index is weighted to large, mature companies that pay most of their earnings out as a dividend, leaving very little for growth.

It just so happens that the larger businesses in Australia tend to be more mature older style operations, while in the US it is true to the contrary.

Let’s take a moment to break down ASX: STW. Investing in ASX: STW automatically givens investors significant exposure to 5 banks (4 retail banks and an investment bank). Even if investors are comfortable with some exposure to banks, investors need to ask themselves whether they necessarily want 32 per cent of their portfolio exposed to one sector facing headwinds from a weakening housing market.

Or whether they want ASX:TLS whose earnings and dividends have fallen over 10 years in the face of increasing competition?

Or ASX: WOW a business with declining margins and growing threats from offshore entrant?

Or how about 18.5 per cent exposure to the Materials space at the mercy of the cyclical iron ore price or coal price?

Or finally 5.79 per cent to OPEC influenced energy sector with all the volatility and vagaries of the oil price?

That’s 57 per cent of the portfolio tied up across three sectors with a breadth of exposure that is narrowed towards what are arguably the more mature sectors of the global economy. The future success of many investors is being determined by the profit outlooks for literally a handful of companies and even fewer sectors of the economy.

I’m not saying having exposure to these things is wrong. Investors may well want exposure to all these sectors. However, I’d put it to you that a significant portion of investors in ASX: STW wouldn’t have scratched below the surface to understand the granular composition of what it is they are investing in.

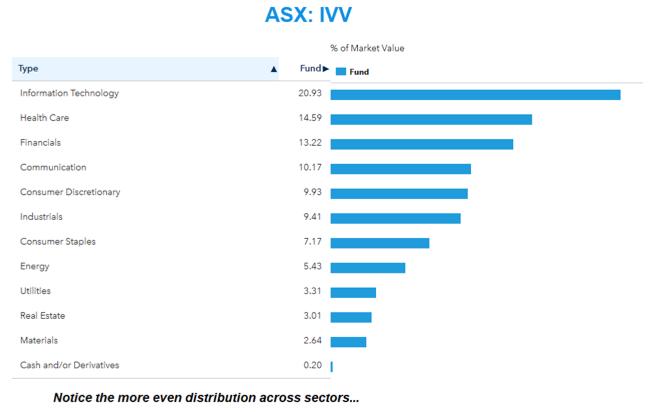

S&P 500 Passive Exposure (ASX: IVV)

Comparatively, the S&P 500 ETF provides only ~20 per cent combined exposure to financials, energy and materials.

Technology, for instance, makes up more than 20 per cent for the S&P 500 Index, the largest sector exposure lead by the FAANG stocks (Facebook, Apple, Amazon, Netflix and Google). This compares with the ASX 200 where tech makes up less than 3 per cent. Healthcare comes in second 14.5 per cent (8.5 per cent on the ASX).

Concluding remarks

When looking at the sector breakdowns at Medallion we’ve long had a belief that investors can improve their chances of capital growth by identifying economic themes, and fundamental changes in the business landscape that can help focus investor attention towards the businesses with the brightest outlook.

For that reason, we’ve tended to have a preference for Technology and Healthcare over Banking and Mining and would have a natural preference for ASX: IVV over ASX: STW. However, in saying that we remain cautious about piling money into any ETF.

When the market is rising and the risks appear low, index investing looks attractive. But what happens when the index starts to fall, and investors through ETFs find themselves indirectly invested in a concentrated narrow range of Banking company’s or a bunch of hyped up Technology businesses?

It’s one thing to say just own an ETF, but it’s important to understand the holdings beneath the surface.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

3 topics

2 stocks mentioned

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Michael is Managing Director of Medallion Financial Group with a number of years experience in financial markets, specialising in financial strategies and investment management.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management