Infrastructure is the hottest ticket in town

Alternative managers are continuing to see increased interest from traditionally conservative clients and it seems infrastructure is the hottest ticket in town. With President Trump’s (still unannounced) plans to drive over $1trn of infrastructure investment in the US, China pledging over US$100bn in investment for “One Belt One Road”, Blackstone Group announcing plans for a US$100bn infrastructure investment fund and the Australian Federal budget offering strong support for infrastructure it’s hard to argue otherwise.

The US barely makes the grade

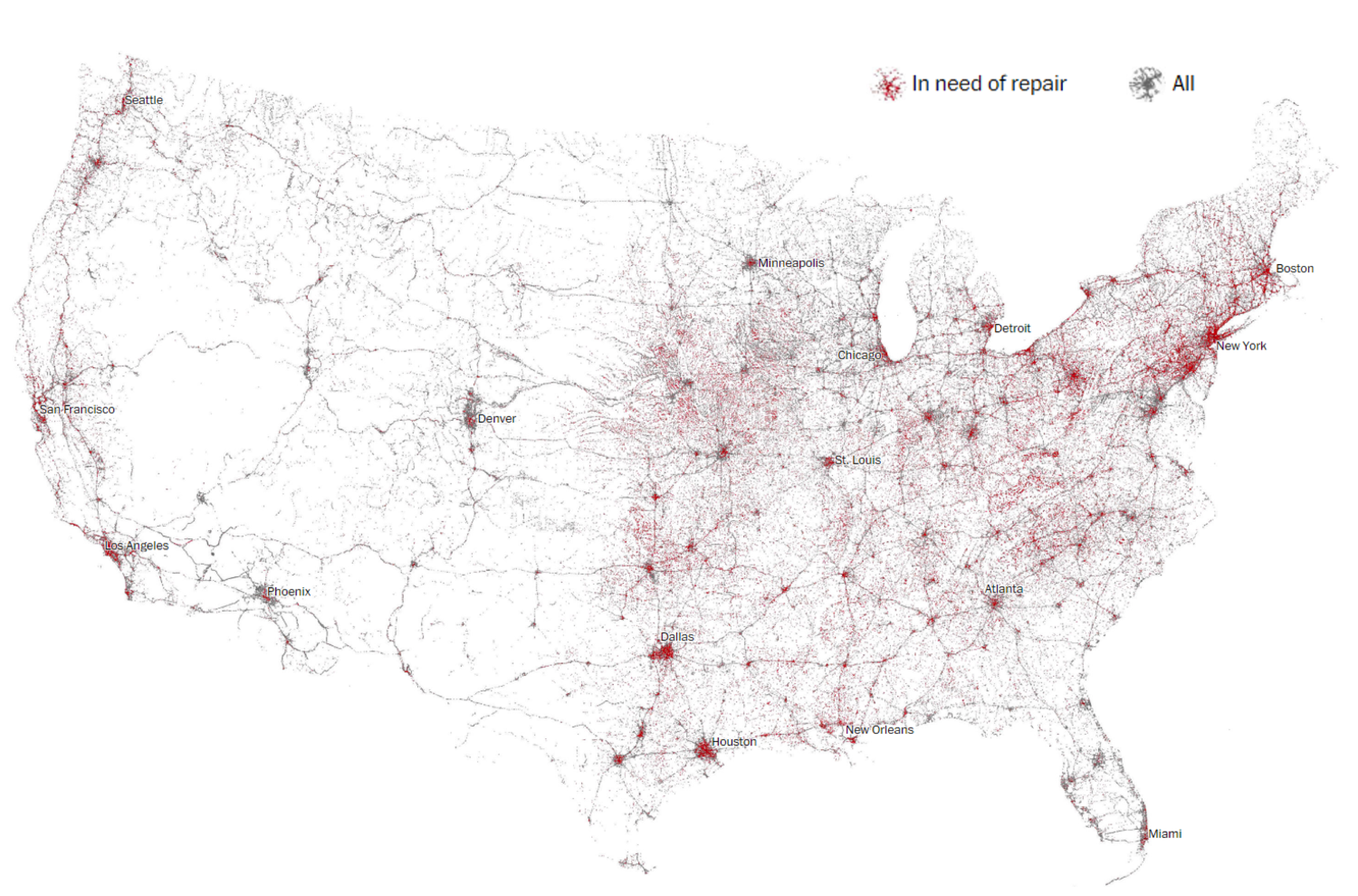

Not only is there plenty of cash looking to invest into infrastructure but there is plenty of need. In the US the American Society of Civil Engineer’s 2017 report gave America’s infrastructure a cumulative grade of D+, while the Road and Transportation Builders Association classified 60,000 (10%) of America’s 600,000 bridges as structurally deficient – see map below.

10% of America’s 600,000 bridges are structurally deficient

Source: The Washington Post, American Road & Transportation Builders Association.

How will they fund the upgrade?

With so many investors looking to infrastructure and a clear need for more investment it should be simple right? Not so according to our infrastructure team who are currently looking towards the US for their first North American acquisition. The biggest challenge according to them is not how to finance infrastructure but how to fund it. At first this may seem like an odd distinction but it is key if we are to understand the challenges to private sector involvement in infrastructure and the ability to execute on the significant capital looking to invest. Public Private Partnerships (PPPs) require a stream of cash flows to support the construction and/or operation of infrastructure, the funding. Generally, this either takes the form of government payments (from tax revenue) or usage charges (tolls). While tolls are suitable for new projects they are generally politically difficult to introduce on previously free roads and bridges.

PPPs are unlikely to fill the gap

This may pose a problem for President Trump’s planned infrastructure boom, 64% of infrastructure spending comes from the public sector (despite electricity, gas and oil infrastructure being 90% owned by the private sector) and many of the assets that need investment, such as the Interstate Highway System, are still publically owned. Political resistance to tolls on these assets has been strong, after all the interstate highway system is the ultimate representation of American freedom. Add to this the opposition to increasing taxes to fund infrastructure (i.e. through raising the gasoline tax for the first time since 1993) and it becomes clear that PPP deals may not be as forthcoming as hoped. While we still believe an increase in infrastructure spending is likely, we would caution the early optimism for a boom in PPPs. New sources of funding are likely needed.

Investors should exercise caution and aim for defensive assets

The other challenge for investors looking to get into the space, according to our infrastructure team, is not to get too caught up in the thematic frenzy. It is important to focus on the key characteristic of good infrastructure assets; well regulated, long-term cash flows with stable market structure and defensible characteristics. To put it bluntly, investors need to focus on the details not the headlines.

More insights

For more from Colonial First State Global Asset Management's Economics & Market Research team click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

First Sentier Investors is a global asset management group focused on providing high quality, long-term investment capabilities to clients. We bring together teams of active, specialist investors who share a common commitment to responsible investment principles.

We are a stand-alone asset management business and the home of investment teams AlbaCore Capital Group, FSSA Investment Managers, Igneo Infrastructure Partners, RQI Investors and Stewart Investors. All our investment teams – whether in-house or individually branded – operate with discrete investment autonomy, according to their investment philosophies.

6 stocks mentioned

First Sentier Investors

First Sentier Investors is a global asset management group focused on providing high quality, long-term investment capabilities to clients. We bring together teams of active, specialist investors who share a common commitment to responsible...

First Sentier Investors

First Sentier Investors is a global asset management group focused on providing high quality, long-term investment capabilities to clients. We bring together teams of active, specialist investors who share a common commitment to responsible...

Comments

Comments

Sign In or Join Free to comment