Is Australia’s current account surplus firing up the Australian dollar?

“Inclusive economic institutions require secure property rights and economic opportunities not just for the elite but for a broad cross-section of society.” Daron Acemoglu, Why Nations Fail.

The Australian dollar has rebounded from a trough below USD 0.56 on 19 March, at the height of the equity market weakness, to almost USD 0.69 today. That’s a tidy 22% rise from its trough. Now, while recent weeks have seen the US dollar edging onto a weaker trend, with new fiscal stimulus and recovery hopes in Europe pushing the euro from USD 1.08 to USD 1.116 over the past two weeks (a 3.3% gain), the Australian dollar has been outperforming across the board, with the Aussie TWI up 20% since 19 March and by over 5% since mid-May.

In addition to Australia’s better-than-expected COVID-19 experience, and with the Reserve Bank of Australia in its June meeting statement yesterday saying "it is possible that the depth of the downturn will be less than earlier expected”, Australia’s booming trade surplus (and now current account surplus for a year) is likely also adding some support to the Australian dollar. While services exports (tourism and education) took a hit in Q1 2020, volumes of coal and iron exports held up, while elevated prices adding firepower to the 4% of GDP trade surplus.

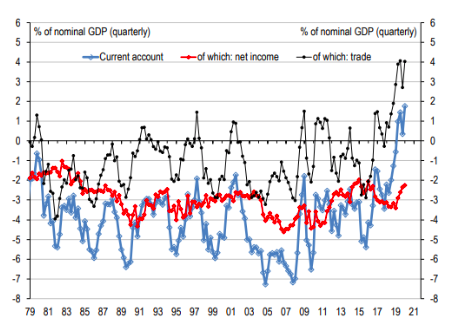

As far as the broader economy goes, this is cash sloshing into the country, and enough to offset our net income deficit (largely servicing our overseas debt) to deliver a current account surplus. As the chart from UBS (and the Australian Bureau of Statistics) shows, this is not something Australia has experienced for at least the last 40 years. Mining, a key beneficiary of this income, has also been one of the stronger sectors in Q1 this year (along with manufacturing), showing rising sales, capex and profits. It’s likely that this income—and a positive net exports contribution helped by weak imports—will contribute to a Q1 GDP print today that is ‘less bad’ than earlier expected—and we may even sneak a positive.

From a portfolio perspective, holding 100% in global equities unhedged would have partially protected returns as global markets corrected lower in March, but will have also muted returns to the upside as global equity markets have rallied higher through April and May. With the Australian dollar now at UBS’s end-2020 forecast of USD 0.69, there has to be some risk it moves well into the USD 0.70’s in the year ahead as a likely synchronised (likely ‘U-shaped’) global recovery post-COVID-19 takes hold. A structurally better external trade position and better fiscal starting point are also likely to support the currency. A renewed US-China trade war seems one of the only likely nemeses for the Australian dollar from here.

Australia’s trade and current account surpluses support the Australian dollar higher

Source: Australian Bureau of Statistics, UBS.

Be the first to know

We share Crestone Wealth Management views on a range of macro topics that we're watching. Click the ‘FOLLOW’ button below to be the first to hear from us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment