Is CBA symptomatic of a perverse cycle?

Clime Investment Management

Clime Investment Management

The revelations that the Commonwealth Bank of Australia (CBA) is being taken to court over alleged AUSTRAC reporting and compliance breaches will overshadow its annual result this week. The action is a civil one and a massive penalty is likely. However the monetary penalty is unlikely to affect the CBA share price. For instance, a theoretical but massive $1 billion fine is a mere 1/140th of the bank’s market capitalisation and would represent just 1.5% of shareholder equity. Based on the FY 17 reported net profit of $9.9 billion, it could be paid from bank pre-tax earnings in just one month!

Therefore the CBA’s intrinsic valuation will be hardly affected by this event but it may soon become clear that the premium rating by the market for CBA compared to its Australian peers (WBC, ANZ and NAB) must be challenged. We will examine this aspect a little later.

Earlier this week, the CBA board released the following statement whereby it wiped out short-term incentives that may have been payable to key executives for FY17 and declared it will reduce non-executive board fees by 20% in FY 18. While this is noble, it hardly addresses the damage done to the reputation of the bank. Further, the “give up” by directors and executives will be dwarfed by the fine that will be borne by shareholders.

“Statement by the Chairman of the Commonwealth Bank of Australia, Catherine Livingstone AO, on executive remuneration

Tuesday, 8 August 2017 (Sydney): Yesterday the Commonwealth Bank of Australia Board met to consider the bank’s financial results and the remuneration for senior executives for the 2017 financial year.

In determining the final 2017 financial year outcomes for remuneration, the Board gave consideration to risk and reputation matters impacting the Group.

The remuneration outcomes will be disclosed in detail in the CBA Annual Report to be released next week. This year, the Board recognises heightened public interest in executive remuneration, particularly having regard to the civil penalty proceedings initiated last week by the Australian Transaction Reports and Analysis Centre (AUSTRAC).

Therefore, in advance of the presentation of CBA’s financial results tomorrow, the Board advises that it has decided to reduce to zero the Short-Term Variable Remuneration outcomes for the CEO and Group Executives for the financial year ended 30 June 2017.

In reaching this conclusion the overriding consideration of the Board was the collective accountability of senior management for the overall reputation of the Group.

The Board also recognised that it has shared accountability and therefore has decided to reduce Non-Executive Director fees by 20 per cent in the current 2018 financial year.

The remuneration arrangements for the CEO and Group Executives are made up of both fixed and at risk short and long-term variable remuneration. The ‘at risk’ components are based on performance against key financial and non-financial measures. Full details of the remuneration outcomes and the Board’s full consideration will be disclosed next week in the Annual Report.

Mr Narev retains the full confidence of the Board.

Catherine Livingstone AO

Chairman

Commonwealth Bank of Australia”

Time will tell who was actually responsible for this breach and this will be made public – particularly if the CBA defends the action in the legal proceedings. However, the presenting of evidence into court could cause immense embarrassment for a range of executives that may have failed to comply with clear and well understood legal requirements. These requirements are designed to thwart the movement of illegal cash transfers and close the tax net around the black economy. Compliance of the banking system with cash movement monitoring is crucial to Australia’s fiscal and social well-being. Tax should not be avoided and the proceeds of crime should be confiscated.

The CBA board has noted the “risk and reputational issues” that are flowing from the alleged AUSTRAC reporting contraventions. This is important for CBA shareholders to understand because the relative rating of CBA shares on the stock market has consistently been at a premium to its peers. This premium is reflected in a higher multiple of its share price to its NTA per share. This rating also reflects years of superior performance in terms of the return on shareholders’ equity.

Despite this premium rating, it has not resulted in a superior share price performance by CBA over the last 3 years. Indeed the share price today is exactly the same as it was in August 2014. The big banks have been affected by a range of headwinds but have all benefited from a surge in household debt that has helped grow their balance sheets and profits.

While household debt has exploded in a rampant property surge in SE Australia, the low interest rate cycle has crimped margins and the regulated requirement for more capital has inhibited profitability (see below).

Figure 1. CBA Share price, 2012 - current

Source. ASX

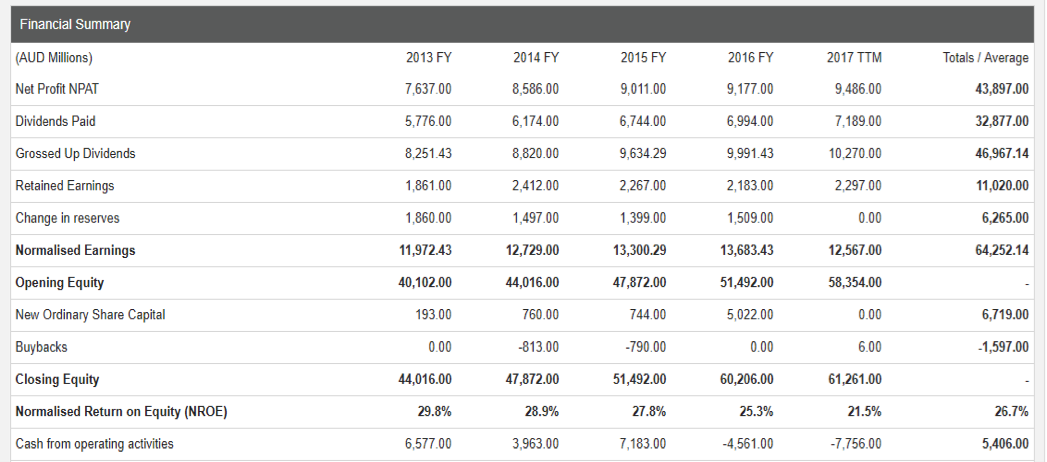

The next chart from “StocksInValue” tracks the last 5 years financial performance by CBA (to March 2017) and it requires some clarification for readers before we delve into the numbers and trends.

First, the term “normalised earnings” needs to be defined. It is calculated by adding the franking paid on dividends to the reported Net Profit. The franking can be calculated by taking “Dividends paid” from “Grossed up dividends”. Then the “Normalised return on equity” needs to be understood as it draws upon the “Normalised earnings” (that include franking credits) in the calculation. The return is thus normalised earnings divided by average equity per share in a financial year.

Figure 2. CBA Financial Summary

Source. StocksInValue

So what do we see from the above table?

First, CBA is a highly profitable bank as measured by its normalised return on equity. It has produced significantly superior returns to its peers and this results from years of good credit and capital management. The return of 21.5% over the last 12 months exceeds the average of WBC, ANZ and NAB by approximately 5%.

Second, CBA has been a superior payer of franked dividends. Over the last 5 years $33 billion of dividends have been paid from earnings of $44 billion. The payout ratio of 75% is high, but this is the norm across the banking sector. The franking level reflects the high tax payments made by CBA. Over five years about $20 billion in company tax has been paid and $14 billion in franking credits paid to ordinary shareholders.

Third, there is a noticeable decline in normalised return on equity (from 29.8% to 21.5% over 5 years). This is a measure of profitability and so while profits are rising, the profitability is falling. This is important because it is profitability that mainly determines the multiple of equity (or NTA per share) that a company’s shares trade at.

Fourth, to see this point more clearly, we focus on the incremental returns coming from retained or raised equity. Over the last 5 years, CBA has grown equity by $18 billion (from $42 billion to $60 billion) and lifted earnings by $1.8 billion (from $7.6 billion to $9.4 billion). The incremental return is thus averaging 10%, or 15% adjusted for franking credits.

The incremental returns on equity for CBA are falling and this has dragged down the overall return on equity. While this is concerning, the decline is actually more acute because of the massive amount of hybrid equity raised over the last 5 years. These $5 billion of hybrid raisings have helped CBA (and all major banks) to meet the more stringent risk-adjusted capital ratio requirements set by APRA. However, while it is adding to tier 1 capital, it is generating a low return for the banks after the servicing of dividends to the hybrid owners.

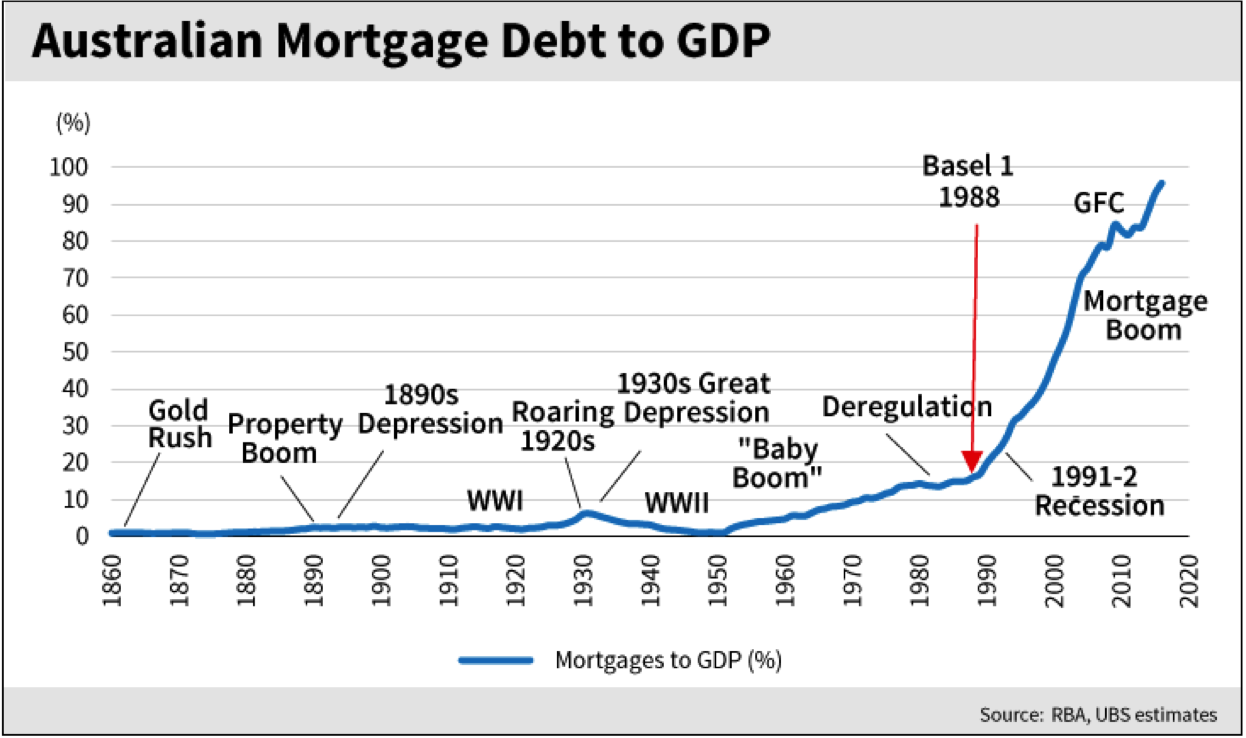

The new risk weightings imposed by APRA reflect the fact that CBA and its peers had for many years understated the true level of risk in their mortgage assets (their loan books). The result was simple – CBA and its peers could generate excessive (and in CBA’s case, exceptional) returns on equity by leveraging up their balance sheets and understating the need for capital.

While CBA is an exceptional bank, it has clearly benefited (like all the Australian banks) from an extraordinarily prolongued period of sustained economic growth, significant household debt creation and arguably lax capital regulation. The sustained growth period has meant that the last 20 years have been a benign period for bad debts for Australian banks. This remarkable period of super-charged debt creation is shown in the following chart. The banks grew their mortgage loan books funded by cheap deposits and equity grown via a range of hybrid capital raisings that super-charged the returns on ordinary equity. Arguably there was no better bank at achieving this outcome than CBA.

Figure 3. Australian Mortgage to GDP (%)

Source. RBA, UBS estimates

Banks are financial intermediaries that create essential leverage in the economy, leverage required to promote capital investment and growth. Leverage funds short-term working capital and provides bridging finance for companies prior to raising or earning capital. It provides funding for consumers when cash is short, and it supports the workings of governments. Debt has many critical roles - but it should not be excessively relied upon. Having noted this, can anyone claim that there is not too much debt in the Australian household sector?

The growth in bank balance sheets over the last 20 years directly reflects the growth in household leverage; it is well documented that today, over 80% of new loans written by banks are mortgage debt related. It seems that the CBA (like its peers) has taken on the appearance of large building societies. They have done so with an excessive focus on asset growth that clearly benefited executive bonus payments.

What is CBA worth?

While CBA has not underperformed the flat equity market over the last 3 years, it has been its high yield that has benefited shareholders and allowed it to outperform the accumulation index. The last 3 years have seen pre-tax annual returns of about 7%, largely generated by fully franked dividends.

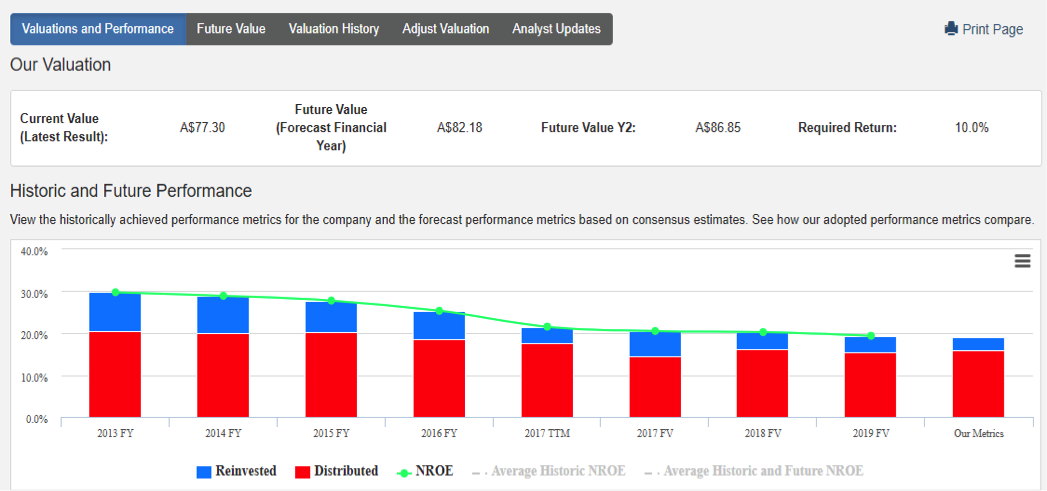

The flat share price and the recent decline following the AUSTRAC legal action has brought the share price below Clime’s assessment of intrinsic value of CBA as at June 2017 ($82.18). Looking out to 2018, we see value growing to $86.95. Together with dividends, this indicates that a 10% potential investment return is developing, based on CBA achieving market consensus earnings.

Figure 4. CBA Valuation, Historic and Future Performance

Source. StocksInValue

After a long period of excessive market price to intrinsic value observations, we now see the share price correctly reflecting the lower return on equity. Subject to further negative news flow, CBA shares will start to look interesting at about $76 (ex dividend) or at a 10% discount to 2018 value.

Why the discount?

Simply because we believe that the years of frantic loan growth and under-capitalised balance sheets are behind CBA. However, these same observations hold true for all the major banks.

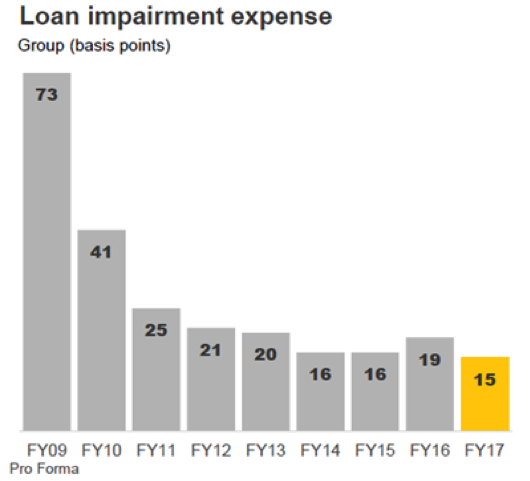

CBA’s loan impairment expenses are at very low levels

Figure 5. CBA Loan Impairment Expense

Source: CBA, 9 August 2017

So while the CBA has created its own unique set of problems, we perceive that slower asset growth, lower ROEs and higher retained earnings will be a common feature of all banks in the next few years. What is unknown is the work-through of the excessive level of household debt that prevails across the Australian economy and within bank balance sheets. So long as bad debts don’t rise, the banks will drift through this cycle; but any significant lift in interest rates or unexpected “black swan” international event could have serious consequences. Indeed more serious than those proposed for senior CBA executives.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

2 topics

1 stock mentioned

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Comments

Comments

Sign In or Join Free to comment