Is private sector indebtedness an impediment to the RBA raising rates?

Since 2014 Australia’s private sector has been on a borrowing binge which has seen private sector debt rise to levels last seen prior to the GFC in 2008. But to what extent is this build up in debt acting as an impediment to the Reserve Bank of Australia raising rates?

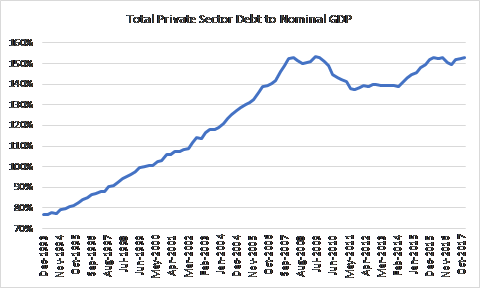

As the chart below highlights (Chart 1) private sector debt as a proportion of nominal GDP has been rising since 2014 and is now back at levels last seen prior to the Global Financial Crisis (GFC) in 2008. Taking this as a measure of private sector indebtedness it is easy to conclude that there is little scope for the Reserve Bank of Australia (RBA) to raise rates. However, this simplistic comparison may be misleading as it compares a stock variable (level of private sector debt) with a flow variable (income as measured by nominal GDP). To achieve a more realistic assessment you need to compare flows with flows.

Chart 1 :

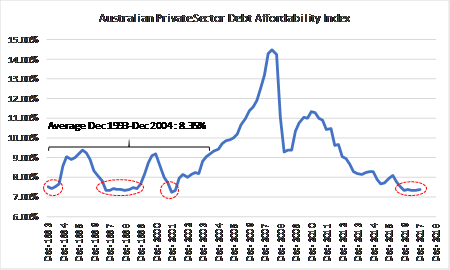

Converting debt levels to a flow variable requires calculating a debt servicing affordability measure based on the cost of servicing debt. To quantify the level of income applied to pay interest on private sector debt, a private sector affordability index is calculated (Chart 2). As the index measures the proportion of income required to service debt a low reading on the index indicates a high level of debt affordability.

Chart 2 :

Considering the history of the index since Dec 1993 several points are worth noting. Firstly, despite the historically high levels of gross debt, low nominal interest rates have meant that the level of debt affordability is still quite attractive. Secondly, Australia has seen similar levels of debt affordability in the past namely in 1993, from 1997-1999 and again in 2001. Considering private sector indebtedness in terms of debt affordability the answer would therefore appear to be that there is little reason to believe that overall debt levels are an impediment to the RBA raising rates.

It is important to consider another dimension to the potential impacts of higher private sector debt levels on RBA policy. Namely that high debt levels, while not preventing the RBA from raising rates per sae, may limit the extent to which they can raise rates. That is, loan affordability may be more sensitive to increases in interest rates resulting in a more cautionary approach by the RBA.

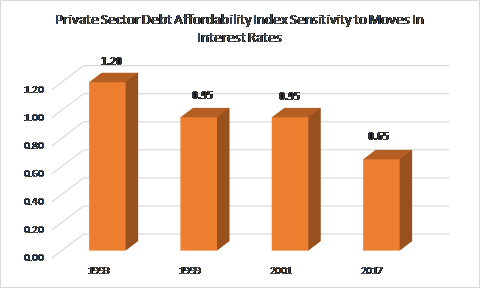

Quantifying this secondary impact is more complex. One way to quantify the relative sensitivity is to start by taking similar points in the debt affordability index at each of the lows in 1993, 1999, 2001 and 2017. Increases in lending rates can then be simulated until the debt affordability index rises back towards some predefined common base (assumed to be the average reading from Dec 1993 - Dec 2004 of 8.35%). The increase in lending rates necessary to reach the Dec 1993 - Dec 2004 average for debt affordability are plotted below (Chart 3).

Chart 3 :

What stands out is that over time, as gross debt levels have increased, the sensitivity of loan affordability to increases in lending rates has also increased. Accordingly, the current levels of debt provide the RBA with around half the amount of headroom to raise rates compared to achieving a comparable impact on debt affordability in 1993; i.e. the sensitivity of debt affordability to increases in interest rates has nearly doubled in the last 25 years.

Implications for RBA policy setting in the future

There are several potential implications for RBA policy setting which can be drawn from the analysis.

Firstly, despite the current levels of private sector indebtedness, the current levels of debt affordability associated with low interest rates provides the RBA with sufficient headroom to raise rates.

Secondly, the level of headroom available to the RBA may not be as great as the level of debt affordability may first suggest. The elevated levels of private debt, by increasing the sensitivity of loan affordability to interest rates, has the potential to limit the extent to which the RBA can raise rates without adversely impacting upon private sector sentiment. As a guide, the back of the envelope calculations suggest that the RBA has scope to raise rates by around 0.5% before debt affordability begins to rise above the longer term historical averages.

Finally, with more limited scope to raise rates before having potentially adverse impacts on private sector sentiment the RBA is likely to approach such actions with more caution. Increased caution is likely to manifest itself in several ways. Initially it is likely that the RBA will need more solid grounds, such as rising inflation, to justify any increase in official cash rates. Further, while initial rate rises may be viewed as relatively low risk, the impact of increases beyond the initial 0.5% become more difficult for the RBA to predict. This suggests that increases in cash rates materially higher than 2% will be implemented more gradually thereby providing the RBA with adequate scope to evaluate the impacts upon the private sector.

Overall, the current levels of private sector debt, while not preventing the RBA from modestly increasing interest rates, are likely to encourage the RBA to adopt a more cautious and gradual approach to adjusting monetary policy in the next few years.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

2 topics

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment