Is Santos a buy, hold, or sell after its big fall? Latest big broker recommendations

Is the plunge in Santos shares post XRG’s exit a major buy the dip opportunity, or a falling sword? We investigate the latest broker calls.

Santos (ASX: STO) shares slumped more than 10% yesterday after the XRG consortium scrapped its $36 billion takeover bid for the ASX listed oil and gas producer. The abrupt exit left Santos investors jilted for the second time in two years, and nursing a big loss in the value of their shares as investors quickly dismantled its takeover premium.

For readers seeking the full story of how and why the deal collapsed, please refer back to yesterday’s article, but in short:

- XRG walked away citing “a combination of factors.”

- Santos confirmed no issues were found in due diligence.

- Disputes over risk allocation, regulatory approvals, and domestic gas commitments scuppered the two reaching a binding agreement.

- Shares have fallen back to ~$6.80, well below the $8.89 indicative offer and even lower than where they were trading pre-bid.

Aussie investors love a bargain – and Santos’ +10% free fall in the last 24-hours could represent a major buy the dip opportunity. In this article, we’ll explore the latest research from several major investment banks to help you answer the burning question: Are Santos shares a buy, hold, or sell?

Immediate broker reactions

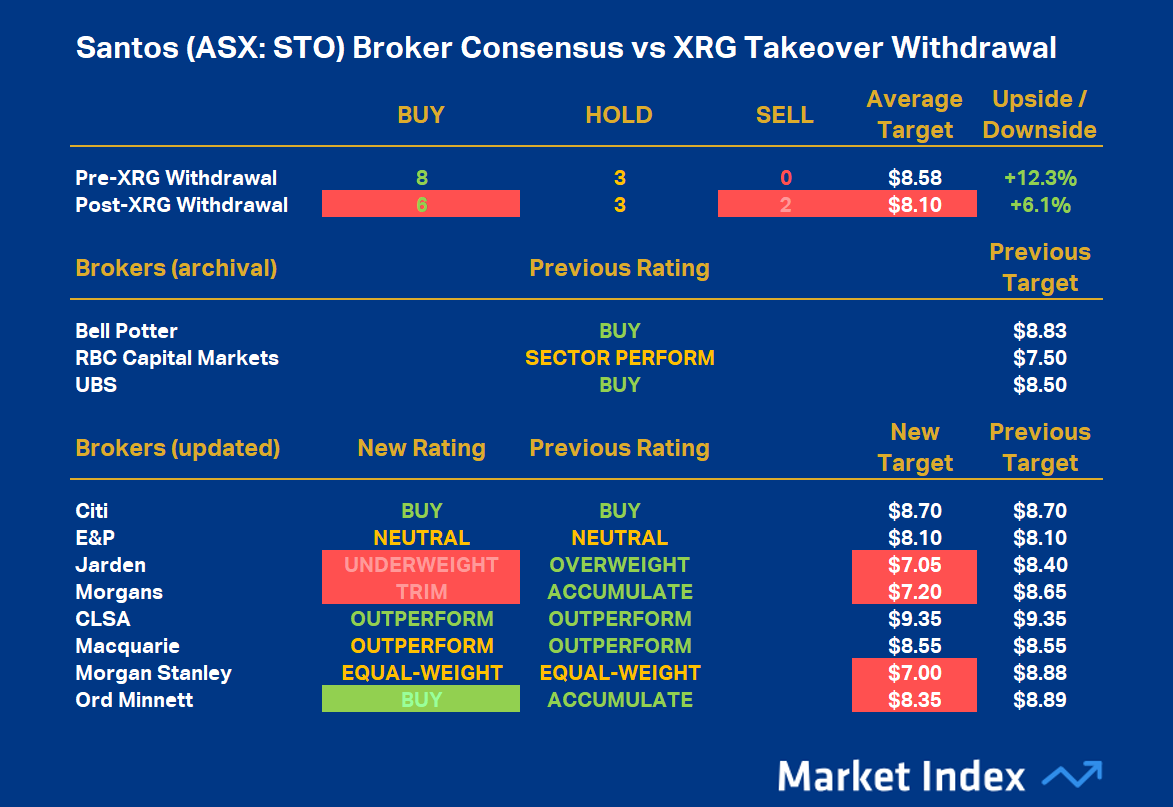

Citi – Retained Buy rating, Target Price unchanged at $8.70

- Notes: “The XRG withdrawal creates fresh questions around STO’s strategic pathway after three failed approaches since 2018.”

- But maintains a constructive stance, forecasting a total return of ~17.5% over the next 12-months.

- With event driven traders likely now departed, sees shareholder rotation as pivotal, with “the pace of long-only re-entry” likely to dictate where shares reset.

- Highlights improved cash flow visibility and growth project de-risking since June.

- Risks remain around PNG LNG, Barossa completion, and soft oil demand in 2025.

Evans & Partners – Retained Neutral rating, Valuation unchanged at $8.10

- Retains Neutral rating citing ongoing doubts after yet another failed deal.

- Notes FIRB and political risks were always high, reinforcing why the firm downgraded its rating when the bid was first announced (great call E&P!).

- Sees risk-reward improving with Barossa and Alaska poised to transform cash generation, notes, “Once the dust settles, it is likely an interesting opportunity may be forming. Santos has been delivering on its growth projects, with Barossa + Alaska to transform its free cash generation and set the business up”

Jarden – Downgrades rating to Underweight (from Overweight), Target Price cut to $7.05 (from $8.40)

- Responded to the withdrawal by cutting its rating to a more cautious stance.

- Warns that the market will scrutinise Santos’s board and its handling of negotiations.

- Expects near-term share price weakness before any recovery can set in.

- Believes investor focus will now shift back to core LNG and oil operations.

Morgan Stanley – Retains Equal-weight rating, Target Price cut to $7.00 (from $8.88)

- Reverts to a fundamental DCF valuation now that “corporate premium has evaporated”.

- Sees STO fairly valued around $7.00 with no discount or premium applied.

- Expects near-term volatility as markets digest the failed deal.

- Notes strong free cash flow yield and a resilient balance sheet as support.

- Barossa first gas (Q3/25) and domestic gas policy reviews flagged as key catalysts.

- Concludes: “We see Santos as fairly valued at these levels, with no discount or premium applied.”

Ord Minnett – Upgrades rating to Buy (from Accumulate), Target price cut to $8.35 (from $8.89)

- Sees collapse as an opportunity: no portfolio valuation or liability concerns arose during due diligence.

- Believes regulatory and political hurdles were the only stumbling blocks.

- Screens STO as undervalued on earnings multiples.

- Forecasts attractive dividends from 2025, rising further as new production ramps.

- Argues the share price weakness should be used as a buying opportunity.

The new consensus

%20Broker%20Consensus%20vs%20XRG%20Takeover%20Withdrawal.png)

To obtain a Broker Consensus Rating, we assign a Rating Value of +1 to any broker rating better than HOLD/NEUTRAL/MARKETWEIGHT; a Rating Value of 0 for any broker rating equivalent to HOLD/NEUTRAL/MARKETWEIGHT; and a Rating Value of -1 to any broker rating worse than HOLD/NEUTRAL/MARKETWEIGHT.

We then take the average of all Rating Values and assign a Broker Consensus Rating of BUY to values +0.5 or above; a Broker Consensus Rating of HOLD for values between -0.5 and +0.5; and a Broker Consensus Rating of SELL for values -0.5 or below.

The Broker Consensus Target is simply the average of the target prices we have on file for each broker. Typically, brokers define their target price as a 12-month forecast, and each target price is based on a broker’s fundamental valuation assumptions. We have only assessed broker ratings and target prices within the last 3 months to account for recent relevance.

STO’s average Rating Value is +0.36, resulting in a Broker Consensus Rating of NEUTRAL. This is effectively a downgrade from its prior average Rating Value of +0.73 and Broker Consensus Rating of BUY.

STO’s Broker Consensus Target is $8.10 (down 5.5% from $8.58 prior to the 18-Sep withdrawal of XRG’s takeover offer). This suggests brokers collectively believe the stock is now around 6.1% undervalued based upon yesterday's closing price of $7.64.

Conclusion: Less confident, execution risk prominent

There are likely still a few broker reports to roll in, but it’s clear from the responses so far that the major broking firms are less confident in Santos as an investment prospect after yesterday’s shock announcement. The spread of broker ratings has widened, as evidenced by the decline in Santos’ average Rating Value from a very strong +0.73 (an average Rating Value of 1 equates to a total buy consensus) to just +0.36 – arguably now only a “Solid Hold”.

Similarly, the range of valuations for Santos’s shares has widened from a previously very narrow $8.10-$9.35 to the updated range of $7.00-$9.35 – an 80% increase.

Most of the brokers did point out improving fundamentals, but there were many that remained cautious, highlighting execution risk and the probable permanent removal of a corporate premium (i.e., they’re not betting on a third time lucky at the altar for Santos any time soon!).

For investors, the decision boils down to one’s confidence in Santos’s execution. If management can deliver Barossa, Pikka and PNG LNG on schedule and on budget, then the upside case of towards $9 per share looks credible. Otherwise, it appears the market has done what it’s best at: Appropriately pricing the risk and reward given all of the information available to it.

This article first appeared on Market Index on Friday 19 September, 2025.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl has a passion for technical analysis and has taught his unique brand of price-action trend following to thousands of Aussie investors.

........

Investing is risky. Inevitably you will endure losses. If you can't cope with losing, don't invest.

%20Broker%20Consensus%20vs%20XRG%20Takeover%20Withdrawal.png){kind=link}

5 topics

1 stock mentioned

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Carl has over 30-years investing experience and has helped investors navigate several bull and bear markets over this time. He is a well respected markets commentator who specialises in how the global macro impacts Australian and US equities. Carl...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management