Is Telstra (finally) cheap?

Only 12 months back, Telstra (ASX: TLS) shares were trading at around $5.00. The fall since then has been precipitous. Which has got a lot of investors asking: does it finally represent good value?

Given its declining share price, we have taken the opportunity on a couple of occasions this year to consider whether TLS had become attractive on valuation grounds, the most recent commentary was when TLS was trading at around $3.90/share.

In those previous visits, we came to the view that TLS did not (yet) provide a sufficiently interesting valuation case. However, since then, the price has fallen further to around $3.50 with little new information, and it looks like it may be time to reconsider. Today, TLS trades close to our previous estimate of intrinsic value, and in a market where most things look expensive, that is potentially interesting.

Given that the value question has become more pointed, our analysis needs to be more comprehensive, and it will take some time to work through the numbers and firm up a possible investment thesis. In the meantime, however, we noticed something about TLS that we thought was a little bit interesting.

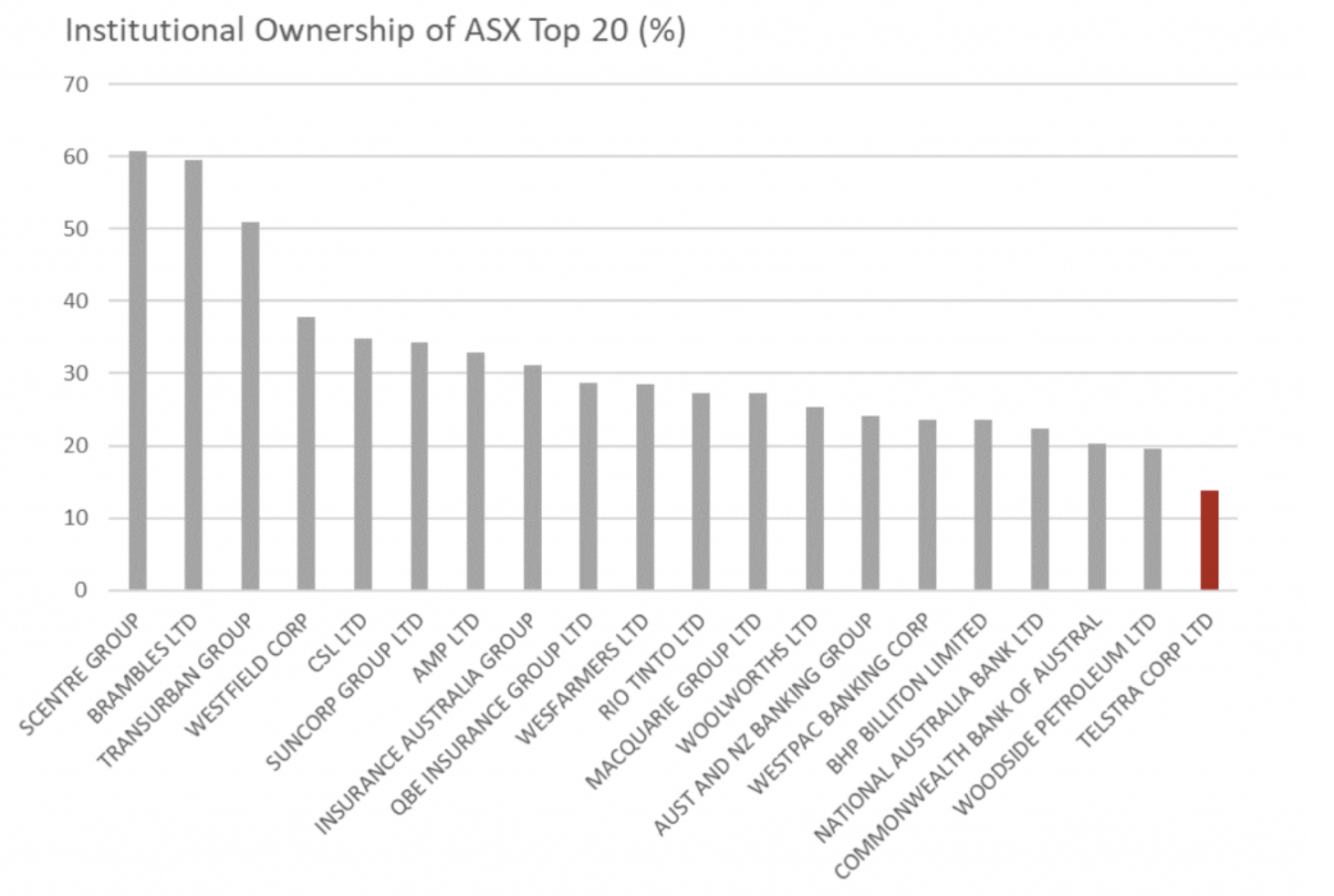

The chart below shows the institutional ownership, as a percentage of shares outstanding, of the top 20 ASX-listed companies. Interestingly, TLS stands alone as the least institutionally-owned top 20 stock, by a significant margin.

It looks as though ownership of TLS may have been strongly skewed to retail shareholders rather than institutions, and we expect that this is a reflection of TLS’s historic dividend policy and yield. We expect that while retail investors are attracted to a strong dividend, institutional investors are more likely to look past the dividend at earnings and valuation. With its previous policy of paying out close to 100 per cent of earnings as dividends, TLS offered a lot of dividend relative to its underlying earnings and growth potential.

With the most recent results announcement, TLS has signalled a move to a more typical dividend policy. Going forward it plans to distribute 70-90 per cent of underlying earnings, plus 75 per cent of net 1-off nbn receipts, giving it greater scope to invest for long-term growth, but at the cost of a sharp reduction in dividends.

Potentially, this triggers a migration from the TLS share register, as the retail investors who had been there for the dividend start to look elsewhere for yield. These investors need to sell to someone, but with limited existing institutional owners, and potential buyers needing to come up to speed on valuation, it may be that a surplus of selling pushes TLS below its fair value equilibrium, at least for a while.

We need to work through the valuation in greater detail to arrive at a considered view on whether TLS is indeed below the level justified by its fundamentals, but in the meantime, we thought this was a potentially interesting dynamic.

The Montgomery Alpha Plus Fund owns shares in Telstra

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our investment process. Tim remains a shareholder of Montgomery Investment Management.

1 stock mentioned

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Tim Kelley has retired from Montgomery Investment Management, effective 30 September 2021. Tim’s final project has been drafting our investment guidelines to integrate environmental, social and corporate governance (ESG) considerations into our...

Expertise

Comments

Comments

Sign In or Join Free to comment