Is Woolworths regaining its mojo?

Daniel Mueller

Vertium Asset Management

Woolworths “is a wonderful organisation, with enormous upside.” This was the first thing former CEO Grant O’Brien said about Woolworths in his inaugural address to the market in November 2011, shortly following his appointment.

And why not think that?

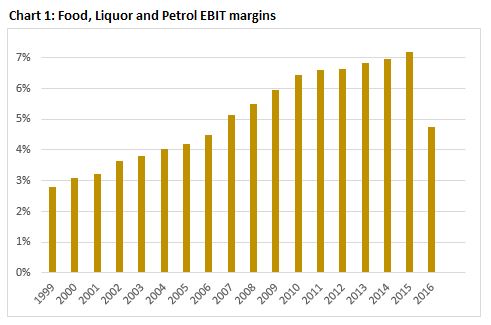

Woolworths had a fantastic history of expanding margins and growing profits. And towards the end of O’Brien’s tenure, Food, Liquor & Petrol (FLP) EBIT margins reach a world leading 7.17% in FY15. And in a deflationary pricing environment, sales growth averaged a not-too-shabby 3.20%.

Yet, this was as good as it got for Woolworths. Seemingly overnight, O’Brien was gone and the Food EBIT margin was just 4.50% at the 1H17 result (with Liquor now being reported separately). Like-for-like sales growth was negative in FY16 and despite returning to modest growth in recent quarters, the company has well and truly lost its mojo.

So how does it regain it under new CEO Brad Banducci?

To answer this question, we need to go back to see how it gained such a strong competitive position in the first place and how this was lost.

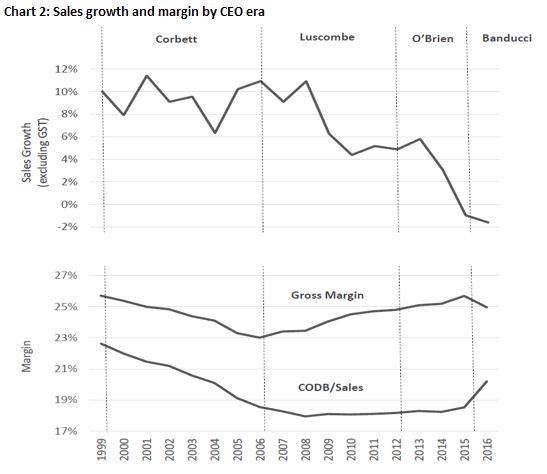

This chart illustrates how margins changed over time and what went wrong, through the prism of each CEO’s tenure.

The Roger Corbett era: 1999 – 2006

In 1999, incoming CEO, Roger Corbett, inherited a business with multiple issues. Cost blow-outs at new warehouses, inefficient state-based buying offices and IT and logistics systems that needed to be revamped were just a few. But the biggest issue was Coles was rapidly gaining market share and threatening to overtake Woolworths as the market leader. In less than two years, Coles had narrowed the gap from 750 basis points to just 450 at the start of Corbett’s tenure.

Corbett’s response was to implement the now vaunted ‘double-loop’ strategy. This involved reducing costs and lowering prices (or in Woolworths management speak “investing cost savings in price”), which benefited customers. This led to strong volume growth. With operating leverage, stronger volumes expanded EBIT margins, which rewarded shareholders. This became a virtuous cycle of productivity gains where both customers and shareholders were winners.

The strategy resulted in impressive average sales growth of 8.65% in Food & Liquor, while their EBIT margins grew from 3.17% to 5.03%.

Beyond the EBIT margin: stepping through gross margins and CODB

In recent years, much of the market’s focus has been on EBIT margin. For years, analysts debated whether Woolworths’ world-leading margin was sustainable or whether it needed to decrease so that the company could recalibrate for growth. But one needs to look deeper into the EBIT margin to find the real reason for Woolworths’ strength during the Corbett era.

A key goal of the double-loop strategy was to extract cost savings of 0.20% p.a. of sales and invest at least half of this saving in lower prices. So in theory, the cost of doing business (CODB) should decrease to reflect these cost savings, but gross profit margins should decline to reflect the investment of these cost savings in lower prices. When we see how this played out during the Corbett era it is apparent he did two things well:

- lower prices for consumers, resulting in the gross margin shrinking, but

- the CODB dropped, more than offsetting the lower gross margin.

The result was strong EBIT growth with both customers and shareholders winning.

Corbett retired in 2006 and was regarded as one of Australia’s greatest CEOs. His shoes were to prove rather large to fill.

The Michael Luscombe era: 2007 – 11

The new CEO’s chair was barely warm when Woolworths drifted away from the double-loop strategy. Sure, the Luscombe era started with a further two years of lower CODB as a percentage of sales. But these cost saving weren’t passed on to consumers. Thus, gross margins began to expand. And they would expand each year for the next nine years. Luscombe’s strategy was simply to ‘milk the cow’. By year three of his tenure, CODB stabilised while the gross margin continued its upward trajectory. Food & Liquor EBIT margins were now well over 7%, unprecedented anywhere else in the world for a supermarket retailer. Fantastic for shareholders but not so good for customers because sales growth was slowing.

But Luscombe began to take one eye off the core supermarkets business. Growth was now to be fuelled by acquisitions, culminating with the Masters JV with Lowes.

By the time the Luscombe era ended, Woolworths was seemingly still a strong business and milking the cow hadn’t adversely impacted earnings or the share price. The market hadn’t paid much attention to the canary in the coalmine: sales growth. This had averaged 10.9% p.a. growth during the Corbett era and 10.2% during the first two years of the Luscombe era. But it slowed dramatically in Luscombe’s last three years to just 5.3% p.a.

But why should investors worry?

Earnings growth was on a tear, the EBIT margin was world leading and the share price was heading one way.

But as Luscombe’s successor was to discover, it takes time to steer a big ship around (whether in the right or wrong direction).

The Grant O’Brien: 2012 – 15

The O’Brien era initially proved to be more of the same. Food & Liquor sales grew at 5.19% p.a. for the first two years and while sales per square metre decreased in FY12, it returned to growth in FY13. And the EBIT margin was just four basis points shy of 8% at the end of year three.

The source of EBIT margin expansion was similar to the Luscombe era. CODB increased slightly but was fairly stable. Gross margins continued to expand.

But unlike his predecessor, O’Brien was faced with a rapidly changing competitive environment that punished complacency, particularly in regards to pricing. By achieving the highest EBIT margin of any supermarket retailer in the world, Woolworths attracted the glaze of some powerful offshore supermarket retailers. During the O’Brien era, Aldi ramped up its expansion and reached 6% market share (10% on the east coast of Australia). Under Wesfarmers’ ownership, Coles overtook Woolworths in same store sales growth in FY10 and had taken its ‘everyday low prices’ mantle. And with less than 10 stores, Costco had grabbed 1% market share in just seven years.

The impact on Woolworths?

Customers considered it more expensive than its competitors and sales growth began to turn negative.

Things fell apart quite rapidly

While juggling too many balls at once, it seemed like management simply dropped them all at the same time. O’Brien announced his retirement in June 2015 (effective from February 2016), leaving behind an unfortunate legacy. This included two notorious firsts in FY16:

- supermarket sales declined slightly for the first time this century, leading to a 40.8% EBIT decrease in Food & Petrol, and

- Big W reported a first-time loss before interest and tax of $14.9 million.

At least O’Brien pulled the plug on the disastrous Home Improvement venture, stemming losses in 2H16 for a full year loss of $218.8 million before interest and tax, a marginal 2.6% improvement on the prior year.

Rounding out the woeful FY16 result, New Zealand Food EBIT decreased by 6.2% and Hotels EBIT decreased by 11.1%

The Brad Banducci era: 2016 – ?, back to the past

While it is early days, Banducci has been quick to go back to the Corbett double-loop formula where customers and shareholders both win. He has quickly rebased margins by reducing prices.

This has led to the Banducci era kicking off to a positive start, with a return to positive same-store sales growth in the first quarter of FY17. And sales growth for the most recent quarter was just over 5% and it looks like the double-loop strategy is beginning to work.

But let’s not get too ahead of ourselves. It is early days and we need to see traction.

Given the skinny margins of supermarket retailers, there is a lot of operating leverage, so we would need to see traction in both sales and CODB before gaining clarity on a sustained turnaround. Also, we should not expect a return to the EBIT margin glory days.

Looking under the bonnet of EBIT margins

The most successful supermarket retailers in the world (e.g. Aldi, Costco) operate on low EBIT margins and don’t allow these to expand. But EBIT margins don’t tell the whole story. Investors need to look under the bonnet and break down EBIT into gross margin and CODB. And for evidence that the double loop is working, we would need to see declining CODB as a percentage of sales, coupled with lower gross margins. In other words, we don’t want to see Woolworths milking their customers but rather passing on any cost savings in the form of lower prices.

Banducci appears to have recognised this. Unlike his two predecessors, we think he will ensure Woolworths remains competitive on price and won’t allow margins to expand. But in an Australian supermarket landscape that now includes Aldi and Costco, it remains to be seen whether he can lead Woolworths back to the glory days of the Corbett era.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching and analysing Australian companies.

Prior to Vertium, Daniel was a Senior Equities Analyst / Portfolio Manager at Forager Funds where he was responsible for assisting with Forager’s Australian equities portfolio.

Before Forager, Daniel held similar roles at Morningstar, Northward Capital, Investors Mutual, Cannae Capital and MMC Asset Management.

6 topics

1 stock mentioned

Daniel Mueller

Vertium Asset Management

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching...

Expertise

Daniel Mueller

Vertium Asset Management

Daniel joined Vertium Asset Management in 2017 as a Portfolio Manager / Equity Analyst and brings with him nearly 15 years’ Australian equity investment management experience. At Vertium, Daniel assists the CIO and is responsible for researching...

Expertise

Comments

Comments

Sign In or Join Free to comment