It's all about growth in Buy Now Pay Later

Last week I sat down with Shaw & Partners Analyst Jono Higgins for an update on the BNPL stocks as we enter a strong period for online retail. I rate Jono highly in this space and his insights are well worth a listen.

The “Buy Now Pay Later” space now enjoys annual turnover of $14bn after just 5-years with around 30% of Australians now using either Z1P and APT but only 5% of Americans are at this point in time, hence the obvious path of growth.

Online shopping has accelerated through the COVID-19 pandemic and we believe it won’t be reversed when a vaccine is eventually found, subsequently we’ve seen 10-years of growth for the BNPL stocks in just 6-months but the cynics will obviously say that’s as good as it gets.

I've summarised some of the key takeaways and presented our views around the sector, or you can watch the recording of our conversation below.

Timing

In the next few weeks, we will see much of the sector report for the last quarter, the numbers should be excellent following strong retail sales. Also, to compound the optimism we are now entering the strongest quarter of the year as we all gear up for Christmas, in other words the next few months should be a purple patch for the sector. After the recent aggressive corrections we believe this is an ideal time from a risk reward perspective to be long the sector.

Current cycle tailwinds

1 – A number of large businesses are taking strategic stakes in the Australian BNPL sector such as Tencent’s (700 HK) 5% in APT and Westpac existing stake in Z1P, plus Amazon (AMZN US) own a bunch of warrants that will allow them to buy into the stock in the future. Consolidation is not yet on the table but the likes of Mastercard (MA US) and Visa (V US) can buy say Z1P without raising equity i.e. its probably just a matter of when, not if.

2 – The cost of capital is rapidly falling as the companies show excellent risk profiles for their customers plus of course it helps that central banks are cutting rates and stimulating the global economy.

Valuation

At this stage we believe it’s not about profits, it’s all about growth as the companies reinvest earnings. In the future we can compare the stocks to PYPL which trades on 22x gross profit but its way too early in our opinion.

Risks

Obviously the main question is how much is built into share price of these growth businesses and yet again it brings me back to our view on the market as a whole “buy weakness & sell strength” – remember the sector has been weak of late. We believe there are 3 main areas of risk:

1 – Competition: we saw recently the impact on the local stocks when PayPal (PYPL US) stated its intention to enter the fray but at this stage in our opinion their offering isn’t as attractive as the Australian competition. Undoubtedly competition will increase but as we mentioned earlier if the US takes up this new method of credit like Australia the sectors set to boom leaving plenty on the table for new players. Margins will also fall as competition increases but that may easily not unfold for 2 years, we need to watch the timeline carefully in this rapidly evolving space. However, as the sector slowly matures the winners of BNPL will have plenty of room to diversify into the likes of car & home loans from a large and happy customer base.

2 – Market : we believe the market itself is the largest risk to these high Beta stocks, if fund managers decide to sell off the high growth stocks BNPL will be included, the NASDAQ is the best barometer of growth valuations and at MM we are bullish at least short-term.

NB High Beta stocks usually move in an exaggerated manner both up and down to the index.

3 – Execution: Obviously high growth businesses need to implement their strategy carefully, investors like ourselves must watch this carefully.

Zip Co (Z1P) $6.17

Zip is our favourite major stock in the space, especially as its trading at a 65% discount to APT. The companies currently accumulating a whopping 6,500 new customers daily, I wish MM was!

MM is bullish Z1P with an initial target 25-30% higher.

Zip (Z1P) Chart

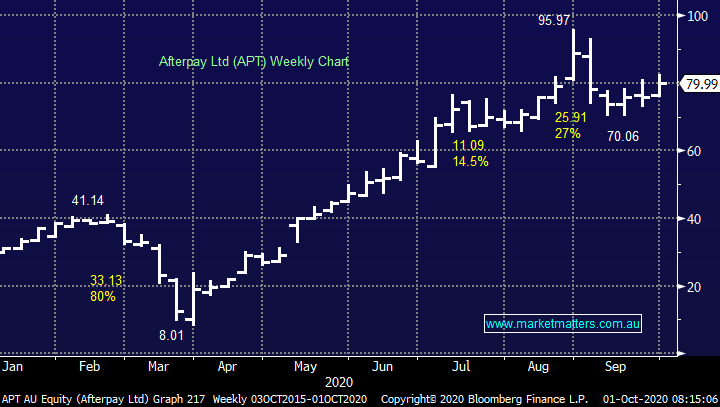

Afterpay Ltd (APT) $79.99

APT is the sector heavyweight with a current market cap of almost $23bn. We like the stock around $80 but see a little more upside and value in Z1P.

MM is bullish APT looking for a test of $100.

Afterpay Ltd (APT) Chart

Get regular market updates

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them. Click here for your free trial.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

........

Any advice provided is of a general nature only.

3 topics

2 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment