It’s always darkest before the dawn

Charlie Aitken

Aitken Investment Management

US equities have led the recent correction in global equities. We have been swinging around on Twitter headlines with index futures traders deciding the short-term direction of markets. Pretty much everything has been moving up and down in tandem, led by gyrations in index futures markets.

I actually deleted Twitter, Instagram and Facebook from my iPhone apps recently as I believe without them it helps you see more clearly without noise. So don’t be concerned I haven’t liked your photos recently!

We have been devoid of fundamental company news due to the blackout period on Wall St, and simultaneously we have been without on market buyback support due to the same company blackout period. That changes this week, as we get a proper taste of US Q1 earnings which will be strong and buybacks will also be allowed to recommence.

I believe the market focus will switch from macro risk events to bottom-up stock fundamentals and with the S&P500 now back at a reasonable valuation; there is a good chance strong US company earnings + buybacks recommencing will put a floor under Wall St. If I am right and we head back to a fundamental earnings focus, then I am of the view that this correction is over. I need US earnings to beat expectations, and I feel they will.

With the help of our prime broker Morgan Stanley, I thought it would be useful to preview this all-important US Q1 earnings season. Even if you only invest in Australia, this is important as it will decide the direction of Wall St and the ASX in sympathy as we have seen this year.

US equities are the dog, and every other equity index the tail.

We have used a lot of charts to make this easy to understand, remembering it is the critical swing factor of the next month and next quarter.

1Q18 Earnings preview & Calendar

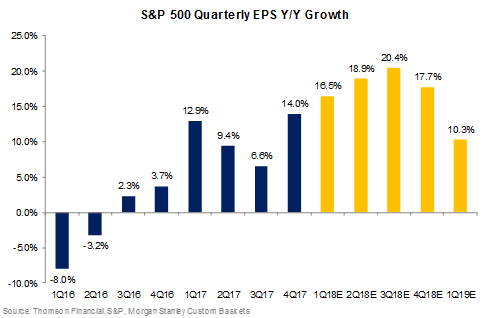

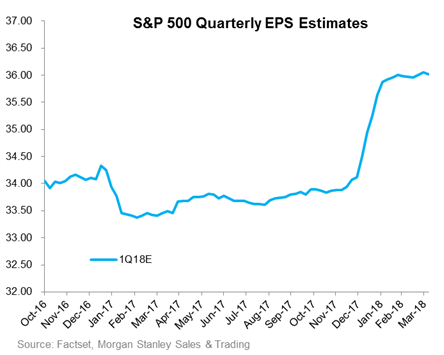

1Q18 is expected to see +16.5% YoY EPS growth, which is the highest YoY EPS growth since 3Q11. Elevated earnings growth prospects reflect tax reform benefits as well as healthy organic growth. Given that companies generally do tend to beat more often than miss, and Y/Y growth does jump higher during earnings seasons historically, the S&P 500 has a chance of seeing even higher-than-16.5% YoY earnings growth. Additionally, MS research has noted that there could be a further boost to earnings from certain accounting rule changes which allowed some firms to move revenue recognition forward while moving expenses backward, thus boosting earnings this quarter.

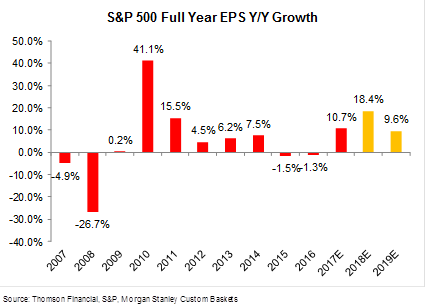

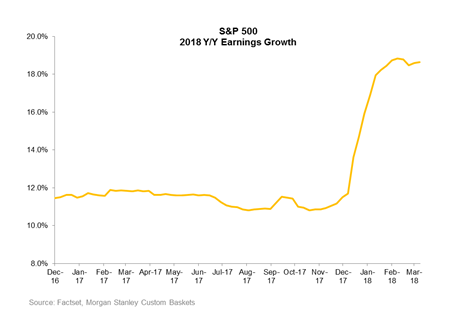

Full year 2018 EPS growth is currently forecast to be +18.4% for the S&P 500 (2018e EPS $158.61). 2018 Y/Y EPS Growth jumped meaningfully higher in January when post tax-reform benefits were baked into analysts’ estimates.

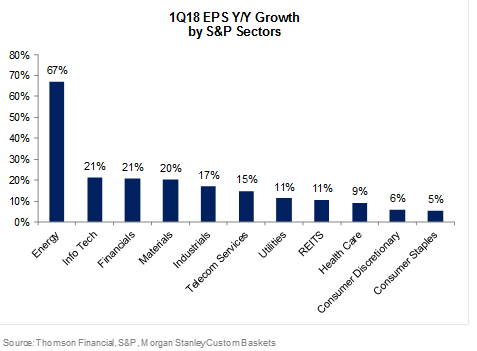

1Q18 EPS Growth By Sector

Energy is projected to see +67% Y/Y EPS growth in 1Q18, the highest among all GICS sectors. Tech and Financials follow up with +21% YoY rate, and Materials at 20%. Consumer sectors are projecting the lowest Y/Y EPS growth: Discretionary +6% and Staples +5%. No sector is projecting an earnings decline in 1Q18.

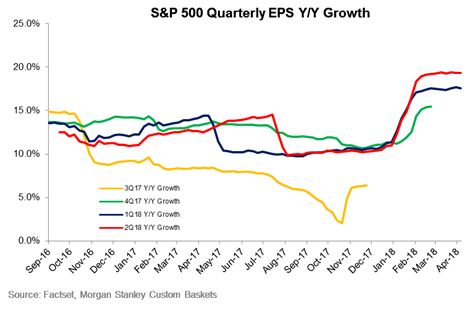

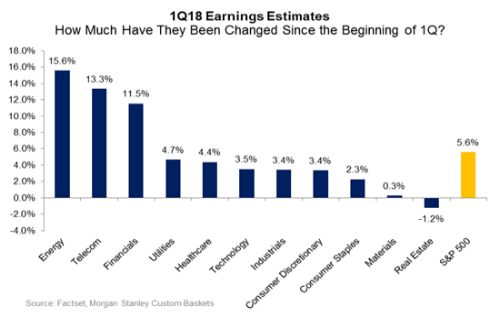

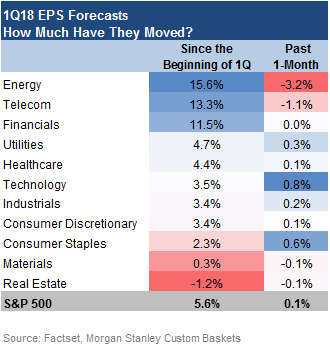

1Q18 earnings estimate revisions for the S&P 500 have been revised up +5.6% since the beginning of 1Q. The SPX 1Q18 EPS estimates initially jumped higher in January and have held steady over the past two months, breaking away from the typical downward revision path seen historically. This unusual positive revision in EPS estimates is not surprising, given the timing of US tax reform.

With the exception of REITs, every other GICS sector saw 1Q18 estimates revise upwards since the beginning of the quarter. Energy saw the largest upward revisions to EPS estimates YTD (+15.6%), although the sector also did see a pullback in estimates over the past month (-3.2%). Tech sector saw just modest upward revisions YTD, but the sector does stand out as having seen the most upward revisions out of all sectors over the past month (+0.8%).

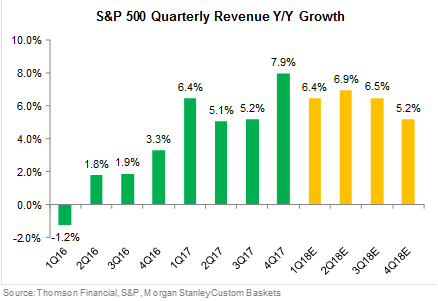

Revenue Growth

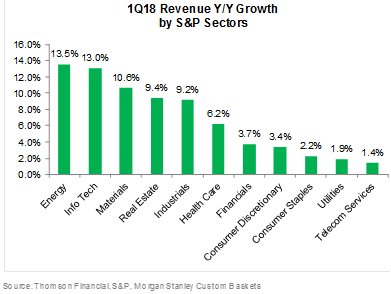

1Q18 is projected to see +6.4% Y/Y revenue growth, which is lower than last quarter’s growth but still on the elevated side vs recent few years. Energy and Tech are expected to see the highest Y/Y revenue growth at +13.5% and +13.0% respectively. Meanwhile, various defensive sectors are expected to see the lowest revenue growth: Staples +2.2%, Utilities +1.9%, and Telcos +1.4%.

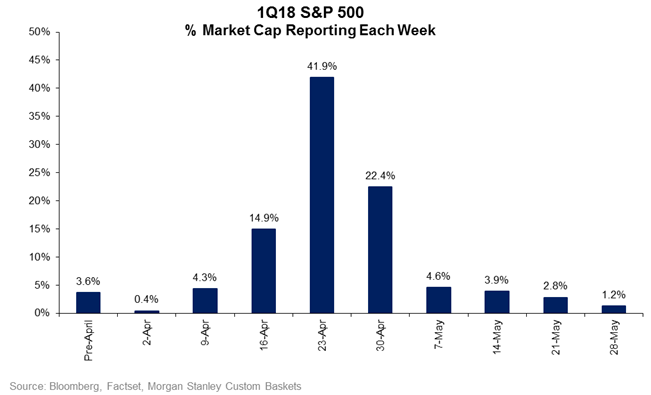

1Q18 Earnings Calendar

By the end of the month of April, 63% of the S&P 500 will have reported earnings. The biggest week for 1Q18 earnings season is the week of April 23rd, when 41.9% of the S&P market cap is projected to report.

All in all, I am of the view Wall St will pass the Q1 earnings test and be supportive for global equities.

We all need to remember bull markets never end when economies and earnings are still growing strongly.

They end on "euphoria” where we see significant P/E expansion and reckless buying of anything. I don’t think we are at that point and I remain of the view we are in a structural bull market for equities.

Markets have been devoid of fundamental information for months. At the same time, volatility picking up has exacerbated moves in markets that are devoid of stock-specific information.

That all changes this week and I believe +16.5% yoy earnings growth in Q1 from US companies should be the fundamental catalyst to end this correction and see money and short-covering come in from the sidelines.

As they say, it’s always darkest before the dawn and I think it’s prudent to selectively take advantage of lower prices you see in global equities ahead of the pending recovery, while increasing short bets against the bond markets...

About AIM

We employ a high-conviction thematic long-short strategy, investing primarily in listed global equities, as well as selected commodities, currencies and derivatives. Find out more

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire