It’s not all doom and gloom for Real Estate

.png)

Omar Khan

Freehold Investment Management

Australia’s national cabinet met on Friday May 8 and in a positive move, set out a three-step process to re-open most parts of the economy for a new ‘COVID normal’.

For the property sector, residential inspections and public auctions are now open, but with some restrictions. While Freehold sees this as a positive move to kick-start the residential real estate economy, we are expecting some level of price decline in residential markets given the level of uncertainty that has understandably arisen in the past few months.

The key factors impacting the residential market include:

- On the positive side; low interest rates and the expectation of a significant and targeted government stimulus initiative, and

- On the negative side; consumer confidence, unemployment and a significant fall in immigration impacting population growth.

Broad market uncertainty had been influencing lending

Since social distancing restrictions took hold across Australia in early March, there has been a number of clear impacts on the residential real estate sector.

1. Like most businesses, the sector has had to rethink how it conducts business. While development sites and construction activity remained open throughout the crisis, selling has been curtailed by viewings being on an appointment-only basis. This has also meant limited real estate project marketing.

2. The underlying value of real estate became unclear as buyers stood on the sidelines, or were unable to transact.

3. Initial forecasts that Australia’s unemployment rate would reach a peak of 15%, since revised downwards, caused concerns as to whether banks would continue to settle on the sold stock.

4. Uncertainty around the ultimate health toll on the nation, in addition to forecast unemployment, had the effect of driving borrowing costs up for developers and lending being curtailed or stopped by many non-bank lenders.

Through this period, we continued to manage the Freehold Debt Income Fund portfolio with a clear approach across all our positions. All projects that are in construction have continued to be delivered to ensure they reach the point of liquidity and maximum value. Where construction has not commenced, works have been delayed where possible, in order to maintain liquidity and gain better visibility of the economic outlook. All positions continued to pay their interest on time, and no position is in breach of its covenants.

There are signs the economy is starting to re-open

The uncertainty noted above led to borrowing rates spiking at the peak of the crisis. However, as it has become evident that Australia has controlled the level of infections, borrowing costs to developers are now reverting back to mid-2019 levels.

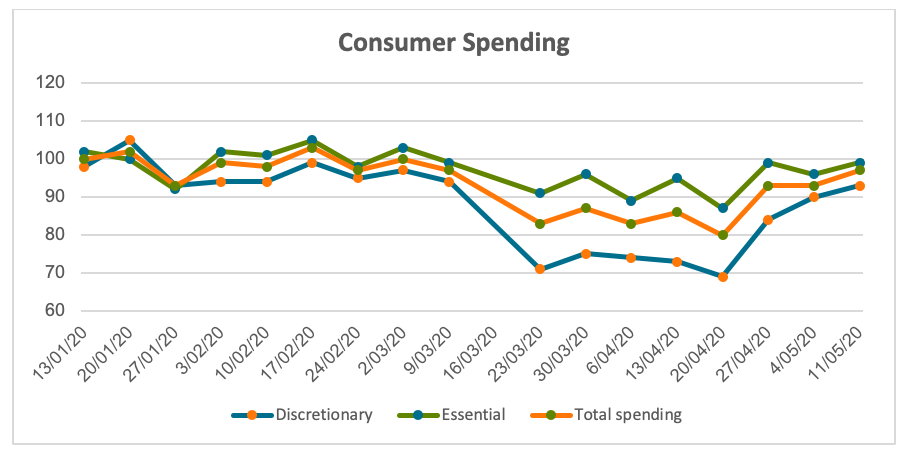

Consumer spending patterns, based on data from about 250,000 Australian consumers and data collected by AlphaBeta, indicates consumer spending is now just 3% below pre-crisis levels.

Source: Alpha Beta

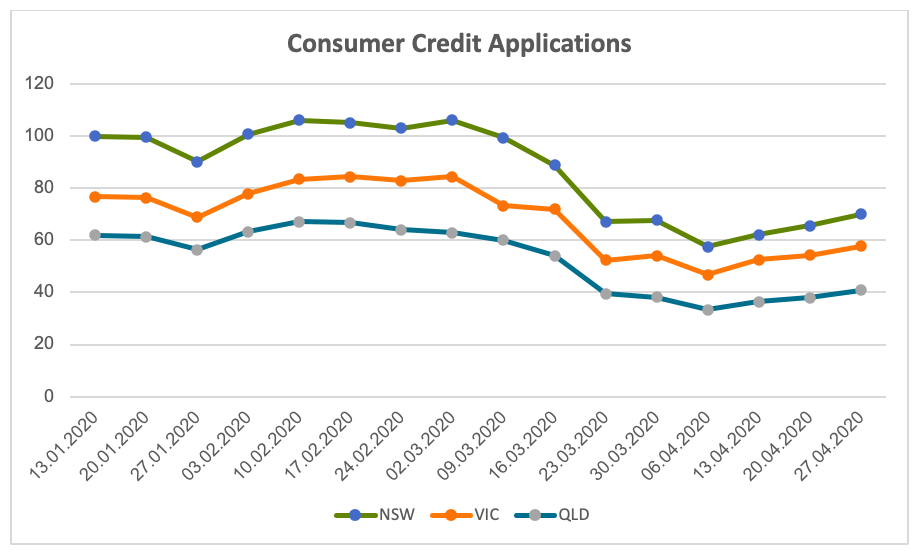

Secondly, credit applications, which are considered a lead indicator of consumption, fell sharply in March, particularly in our largest markets of NSW and Victoria. However, as reported by economists Alpha Beta, while these applications are still well below their peak levels in January 2020, levels have since stabilised.

Source: Alpha Beta

If we look at the projects the Freehold Debt Income Fund is invested in as a guide, we have observed little evidence of any material fall over in settlements. Pleasingly, sales activity has also continued, albeit in smaller volumes. Interested parties that have booked appointments feel secure in their employment and presented with a clear intent to purchase. There is also eagerness to take advantage of the softer market with some developers offering discounts of between 2.5 – 5.0%.

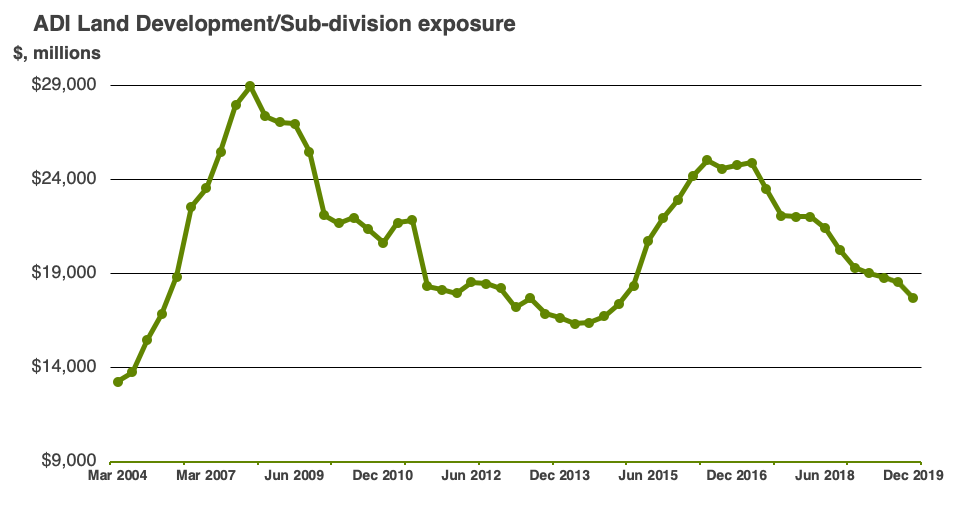

Non-bank lenders continue to grow their market share

The pullback from real estate debt by Australian banks has been evident for a few years and the current economic climate is likely to continue that trend, and if banks do lend, it will be with more onerous terms.

Source: APRA Quarterly ADI Statistics December 2019

Our view is that because less stock will be released over the next 12 – 18 months on the back of both the Royal Commission slow down of 2018/19 and more recent events, and it is also likely to take longer to sell existing stock, there will be higher demand for residual stock facilities. These facilities finance completed inventory, and allow construction facilities, which charge higher interest, to be repaid. The residual stock facility is repaid once the remaining stock has been sold and settled to end purchasers.

Not all pigs are equal

Freehold has been placing capital into residual stock facilities since early 2018. From a risk and downside protection perspective, residual stock facilities are attractive because the projects they finance:

- are complete, so there is no construction risk;

- has reached its maximum value;

- carries less risk than trying to sell an undeveloped site;

- are more attractive to purchasers than off the plan or semi-constructed projects; and

- can be placed in the rental market if required, and then ultimately sold to end purchasers.

It is worth noting that not all residual stock facilities are the same. When considering facilities, the quality of the stock and the price point that it is trying to target is essential. In any market where it is taking longer to sell, you want your stock to be at the top of the demand stack to purchasers. The Freehold Debt Income Fund has about ~15% of its capital invested in residual stock facilities, and we’re open to increasing that exposure subject to the quality of opportunities presented.

Conclusion

Over the next 6 – 12 months, there will be less housing stock released into a government stimulated market with improving consumer sentiment. We see these as positive signs for the real estate debt sector as this should protect capital values, and bring new projects to market. For investors, this is likely to mean an increased number of opportunities where it will be essential to focus on quality and product best aligned to consumer demand.

Focus on recurring income and low volatility

Throughout the market volatility, Freehold has been able to pay a monthly income distribution consistently, and the fund is performing above its target return of 7 – 8% p.a. Learn more about our strategy here.

Click the 'FOLLOW' button below for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

........

The information in this article has been prepared by Freehold Investment Management Limited (Freehold), AFSL 339008. This material is intended only for wholesale clients and must not be relied or acted upon by retail clients. This material provides general information only and does not take into account your individual objectives, financial situation, needs or circumstances. Before making any investment decision, you should therefore assess whether the material is appropriate for you and obtain financial advice tailored to you having regard to your individual objectives, financial situation, needs and circumstances.

.png)

2 topics

Omar Khan

Executive Director and Portfolio Manager

Freehold Investment Management

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

Expertise

Omar Khan

Executive Director and Portfolio Manager

Freehold Investment Management

Omar has over 15 years' experience across funds management and real estate. His experience extends across structuring, due diligence, capital raising, as well as managing and growing funds management businesses.

Expertise

Comments

Comments

Sign In or Join Free to comment