January Market Commentary: A Quiet Start to an Interesting Year

January was a quiet month for risk assets with President Trump’s first actions far more interesting than markets. The risk/return outlook in the medium term isn’t great for many asset classes, but there’s some signs of better economic conditions in the US which might help 2017 returns. There’s also sections on economics, high yield debt, asset management, China, emerging markets and regulation.

January brought mixed results for risk assets with gains and losses for equities and credit relatively small. Chinese (2.4%) and American (1.8%) equities rose, whilst Japanese (-0.4%), Australian (-0.8%) and European (-1.8%) equities fell. US high yield credit made gains, whilst investment grade credit pulled back a little in the face of record January issuance. Copper (8.7%), iron ore (6%) and gold (5.5%) had strong price increases but US oil (-1.8%) and natural gas (-15.6%) fell back. All eyes are on the Trump administration as it implements very different policies from what the previous administration and some pundits had expected. 2017 shapes up as being a very interesting year.

Economics

US GDP came in at 1.9% for the fourth quarter and 1.6% for last year, just beaten by the Eurozone which recorded 1.7% growth for 2016. This continues the trend of a very weak recovery with Obama finishing up without a year of GDP growth exceeding 3%. The dour past might be about change though, some US economic indicators begin 2017 in much better shape than a year ago. Conversely, the key indicators tracked by the conference board say that the US economy is in much worse shape than the official measures present.

The US isn’t alone in this experience; global growth for 2016 is expected to report at miserly levels whilst growth in debt increases much faster. Low interest rates make debt servicing far more comfortable than it would otherwise be, but the early signs of inflation in the US and Germany could mean that interest rates will be rising. Pleasingly, the debt to GDP ratio in the Euro Area fell last year. That’s despite the problems with excessive budget deficits as eight EU countries received a warning about their fiscal position. In a break from a previously staunch position, Mario Draghi left open the door to nations leaving the Euro Zone, providing they settle their bills before they leave.

The debate over the failures of quantitative easing and academic economics continues. Some are dismissing economics altogether, but others are asking whether it is just econometrics that has failed. A report from the Bank for International Settlements concluded that quantitative easing has reduced volatility but has not spurred growth.

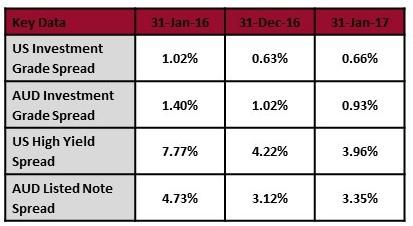

High Yield Debt

US high yield debt is now back on the bad side of valuations. The credit spread for high yield bonds peaked at 8.87% in February 2016 but is now a miserly 3.96%. The junkiest bonds, those rated CCC and below, are particularly overpriced with little room for upside. One of the forgotten rules at this point of the cycle is that you don’t have to have defaults to take losses on a high yield portfolio. A return to average credit spreads can wipe-out several years of coupons. None of this is stopping hedge funds from loading up, distressed energy companies are a particular favourite. The $90 billion of US commercial mortgage debt maturing this year and debt from retailers are other hot spots.

Matt Levine wrote an excellent piece detailing the recent fightback by bondholders against awful covenants. A proposed change would have allowed companies to default on their bonds but avoid the early redemption premium. Matt noted that such a fightback is very unusual, as bond buyers rarely read the bond documents at issue. If they do read them and find something they don’t like, they rarely charge the issuer a high rate for the onerous terms or refuse to buy. This is a cyclical process though, once a crisis hits bond buyers demand strong covenants again before forgetting their importance as the cycle progresses.

I’ve found the same behaviours, I once called the issuer‘s lawyers after they had included an irrelevant section from a previous bond. They were shocked that anyone was reading their work! My response to bad terms, such as those that are commonplace in the Australian listed note market, is to not participate at all. Private debt, syndicated loans and securitisation offer much stronger covenants and better yields. Giving up some liquidity for higher returns and lower risk is the closest thing to a free lunch in the current environment. Keep in mind that the more illiquid a deal is likely to be, the more leverage the investor has to set covenants in their preferred way. If you are in the business of selecting debt managers, asking about their approach to covenants as part of manager due diligence is a great way to separate the wheat from the chaff.

Asset Management

Asset managers and capital allocators might be set for a tough 2017 as global stocks are near all-time highs, volatility is near all-time lows and there’s record bullish positioning in many markets. The bond bull market is the third longest in over 700 years and risk free rates are the lowest in sovereign debt history. This isn’t a good setup for good returns.

The active management versus passive management debate rages on. Active continues to be the majority but is losing market share at a decent rate. The discussion could be better framed as high fees versus low fees as many investors are choosing index funds and ETFs just to get away from high fees. Low fee asset managers like Vanguard are seeing huge inflows, the result being that big asset managers are struggling to grow their profits. Bloomberg highlighted the power of Vanguard and its ability to call out excessive executive remuneration, but the incongruent position where it won’t disclose what it pays its senior managers.

The shift to lower fee managers is still taking an awfully long time to play out though. Hedge funds were beaten by index funds for the seventh year in a row in 2016, and saw redemptions of $106 billion for the year. However, hedge fund assets crossed the $3 trillion mark during 2016 as positive returns more than offset redemptions. Investors continue to ignore the basic maths of hedge funds – it takes less than 20 years for the manager to have more money than you if you pay them a 2% management fee and a 20% performance fee. What’s worse is that some hedge funds are charging more than double the 2% and 20% fees by passing on dubious costs to investors.

China

The quarterly GDP print for China was 6.8%, above expectations but below the results of recent years. The growth was very much state led, old economy growth, as seen in the continued high prices being paid for iron ore. This might be coming to end with iron ore stockpiles at record highs. Commentary by key leaders has opened the door to managing GDP figures lower with a target of around 6.5% GDP growth for 2017. China hasn’t been immune from the global trade slowdown, with its exports falling by more than its imports in 2016.

As always, GDP growth must be read alongside debt to GDP growth for the whole picture. With one version of that ratio going from 254% to 277% during 2016 China continues to be on an unsustainable path. Another article pointed out that this looks just like Japan, Spain and Thailand before they had problems. Banks have been warned again to slow down lending particularly to residential property.

Early stage warnings signs of a credit crunch are starting to show up. Bond defaults doubled in 2016, but remain low as a percentage of all bonds. Unlike the past, not all defaults are being cured and some pretty severe losses are being taken. Key interest rates are rising causing bond sales to be cancelled. A spike in funding costs and a liquidity crunch saw the PBOC inject liquidity and cut the reserve ratio for banks. Stressed companies are turning to asset backed funding to raise debt. Residential property prices have peaked and the public reporting of some property price indices has been stopped.

None of this guarantees a credit crunch in the short term, it could be another head fake like those in recent years. The wall of junk debt maturities in 2017 and 2018 will provide a test to the system. Wealth management products, entrusted loans and Dai Chi repo games are all areas of concern.

December saw FX outflows at virtually nil, a break from the roughly $1 trillion of cumulative outflows over the last 18 months. The strong outflows have seen China dumping US government bonds with Japan now the number one holder. Banks have been told they must balance their FX trades with transactions as small as US$5,000 being analysed and sometimes rejected. Overnight interest rates hit 100% as the government sought to break currency shorts. Chinese buyers are having trouble settling global real estate purchases as currency conversion requests are rejected.

Emerging Markets

Emerging markets are offering plenty of problems and potholes for investors to deal with. Mozambique defaulted on a $60 million interest payment. Turkey’s currency is collapsing as outflows surge. Non-performing loans are spiking in Nigeria. Saudi Arabia has hired PWC to find $20 billion of savings across housing, transport, health and education. B- rated Egypt sold $4 billion of US dollar bonds after getting a $12 billion loan facility from IMF in November. The next big test for Venezuela is $3 billion of debt repayments due in April.

Puerto Rico has an extended list of problems to work through and bondholders don’t yet seem to have gotten the memo. The government’s report has the territory only able to meet 21% of debt payments due in 2019, indicating that the territory wants bondholders to take a 79% haircut. Disparate groups of bondholders are jockeying for position with each group asserting that its debt has priority. As well as $70 billion in debt, Puerto Rico has a $48.8 billion hole in its pensions which are only 1.6% funded.

Greece has yet to implement two-thirds of the reforms needed to access the next round of its bailouts funding. The IMF and the EU are further apart than ever in their plans on how to help Greece deal with its excessive debt.

Regulation

Regulators brought unwanted Christmas gifts to banks and brokers with a range of fines handed out recently. Credit Suisse and Deutsche Bank were hit with penalties of $5.3 billion and $7.2 billion respectively for mis-selling mortgage backed securities. The headline numbers are far bigger than the true position, Deutsche’s penalty comprises $4.1 billion in fines and $3.1 billion in “consumer relief”. Deutsche is seeking approval for the consumer relief component to be met by lending to Lone Star, who will undertake workouts on consumer loans. This could see Deutsche make a profit on what is meant to be a penalty.

Deutsche is also being scrutinised for helping Monte De Paschi hide €367 million in losses and will pay $629 million for organising Russian mirror trades. Moody’s will pay $864 million for its role in the subprime mortgage debacle. Citadel was fined $22.6 million for front running its retail clients, a case that exposed the ugly side of high frequency trading. Ten US fund managers have been fined up to $100,000 each in a pay to play scheme with pension funds. No word if any consequences will apply to those at the pension funds who received the “pay”. JP Morgan has been ordered to pay $164,000 plus legal fees to a former employee who they fired after he refused to sell inappropriate products. John Corzine got away with a $5 million penalty for using $1 billion in client funds to cover liquidity issues at MF Global.

A sleeper issue for banks has been the Libor litigation. The US supreme court has ruled that lawsuits against the banks can proceed, with the prospect that banks will be facing billions of dollars of compensation for investors and borrowers. The issue for banks is Libor manipulation was always going to hurt someone and help someone, with the losers suing and the winners keeping their gains. If Libor is inflated borrowers lose by paying higher interest rates on their debt. If Libor is deflated, investors lose by receiving less interest than should have occurred.

The various fines for Deutsche Bank will further reduce its meagre capital position. It looked like it wouldn’t have enough capital to be able to pay bonuses in cash or preference share dividends, but the ECB has given it a temporary leave pass. Deutsche Bank is one of the key European banks arguing against higher capital floors as part of the Basel 4 reforms. These negotiations appear to have broken down with the Americans and Germans at polar opposites.

Media Worth Consuming

Obama will go down as the coolest president ever, the best basketball player but also as President Debt for building the US government debt mountain by far more than his predecessors. It unclear whether Trump will take that title from him, Trump’s policies could make the deficit far worse but his team is working on substantial spending cuts. One of Obama’s final changes was to cut the mortgage insurance payments for higher risk FHA borrowers, but Trump has killed that off already. The FHA insurance scheme now covers more than $1 trillion in mortgages, some of which bear risk characteristics similar to the subprime loans of 2004-2007.

The US fast food industry is in the spotlight as it campaigns against minimum wage increases. Some claim that low wages force US taxpayers to subsidise the industry by $7 billion per year. Some Uber drivers are travelling long distances to wealthy areas to get fares and are sleeping in carparks overnight to reduce their commute. Uber is having a big impact on the value of taxi licences, one lender has a 51.5% arrears rate on their loans secured by taxi licences.

Despite the hopes of some that standard demand and supply concepts don’t apply with minimum wages, research has found there are negative impacts to increasing minimum wages including some businesses laying off workers and others closing altogether. The EU is proposing universal basic income and higher minimum wages for citizens of member nations. The evidence for universal basic income is weak, with some claiming it has never worked and never will. An alternative scheme is for the government to provide work in exchange for welfare. Another suggestion for helping low income earners is to make work abundant and decrease the cost of living. Working against this is government regulation which is estimated to cost each American $20,000 per year.

The Economist magazine has downgraded the US from “full democracy” to “flawed democracy” joining France, Italy and Japan at the sub-par level. A Dutch woman has had her application for a Swiss passport rejected after she annoyed locals by repeatedly protesting against Swiss traditions. Iceland has slashed drug usage amongst teens by making straight forward and inexpensive changes. An unemployed college graduate made $1,000 an hour writing fake news. Bernie Madoff corners the hot chocolate market in prison. The Bank of Canada has made a Youtube video to warn about the housing bubble. Americans responded to the financial crisis by having less children and more pets.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

2 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment