Jump in ISM new orders supports US equities

JK Galbraith observed, “there are two kinds of forecasters: those who don’t know, and those who don’t know they don’t know.”

US equity markets moved higher again overnight. We are just exiting Q2 and, while the full data is yet to come, it will almost certainly portray the weakest quarter of activity in modern history for the US and many other countries. But, in a theme that is likely to be repeated over coming weeks and months, a sharp rebound in activity (at least initially) is likely to buoy optimism about the future and a recovery into 2021.

Last night, US June ADP payrolls (the private sector forerunner to Thursday’s non-farm payrolls) narrowly missed at 2.4 million versus 3.0 million jobs added. However, revisions to May were a positive 6 million (that’s a lot of jobs to suddenly find). Moreover, the manufacturing ISM (a long-term stalwart of US leading indicators before the more popular PMI industry was born) significantly beat, jumping to 52.6 from 43.1 (well above the consensus for 49).

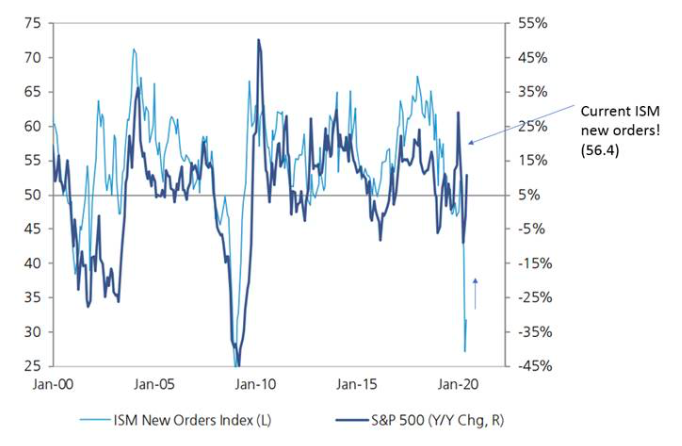

Now here’s the thing. Many equity strategists prefer to look not at the headline ISM index but the ‘new orders’ component. This is shown below plotted against the annual S&P 500 change just one month ago (in this case by UBS’s US equity strategist), with an arrow pointing to where the new orders component is now (added by Crestone). And then there’s the technical ‘suppliers delivery’ component of the ISM which many highlighted as holding up the ISM when things were collapsing, but now is constraining the rebound in the ISM in last night’s data (i.e. it would have been better!).

None of this is to say one should be bullish about the ability of equity markets to drive significantly higher from here. After an initial few months of near-term rebound (as economies transition from ‘stop’ to ‘go’) there remains much uncertainty (and scepticism) about just how fast a trajectory can be sustained when many sectors of the economy will still be operating at well below capacity, unemployment will be high and risks around geo-politics and a second wave of the virus will persist. However, all of this is to say how quickly things can change, how little we actually know about the outlook, and why we spend so much time building globally diversified portfolios that can weather the ups and downs of an uncertain market future!

US ISM new orders signal annual growth in equity

Source: UBS and Crestone.

Follow our updates

We share Crestone Wealth Management views on a range of macro topics that we're watching. Click the ‘FOLLOW’ button below to be the first to hear from us

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment