Just how mature is the current credit cycle?

A recent spate of credit downgrades in the US has thrust high yield credit into the spotlight. The Fed will be acutely aware of the ructions taking place in credit markets with a number of high profile credit funds freezing investor redemptions and junk bonds providing negative returns for the YTD. To get some perspectives on the implications of these moves Livewire asked two of our contributors if they believe we’re now nearing the end of the current credit cycle. If not, how far through the cycle are we?

The credit cycle is mature in time only

Angus Coote, Jamieson Coote Bonds

Credit cycles are slow moving beasts, which often end as a result of a central banks tapping on the brakes. After the final rate hikes in mid 2006 by the FOMC, it took to late 2007 until sub prime debt started to hit radar screens. The sub prime saga dragged on and on until its crescendo moment in late 2008 when Lehman collapsed.

As this cycle stands, it is mature in time only, as we have not even started with rate hikes from central banks, and yet already the hand grenades are going off all over the complex. The global response to the world biggest debt problem in the GFC was to increase the amount of nominal debt by more than 50%. Money has been cheap, and corporates have borrowed with vigour. The problem is much of that borrowing has funded oversupplied industries (think energy and commodities) or funded stock buy backs. Now excess supply, coupled with reduced demand, are crushing those who are over levered. This will continue until we remove that supply from the system via bankruptcy and once again find equilibrium. When the FOMC hike rates next week, despite luke warm data are decaying credit quality, make sure you check where the exit signs are. Risk markets could get very nervous if anything goes wrong.

Costs are rising but the cycle isn’t about to tip

Sam Ferraro, Evidente

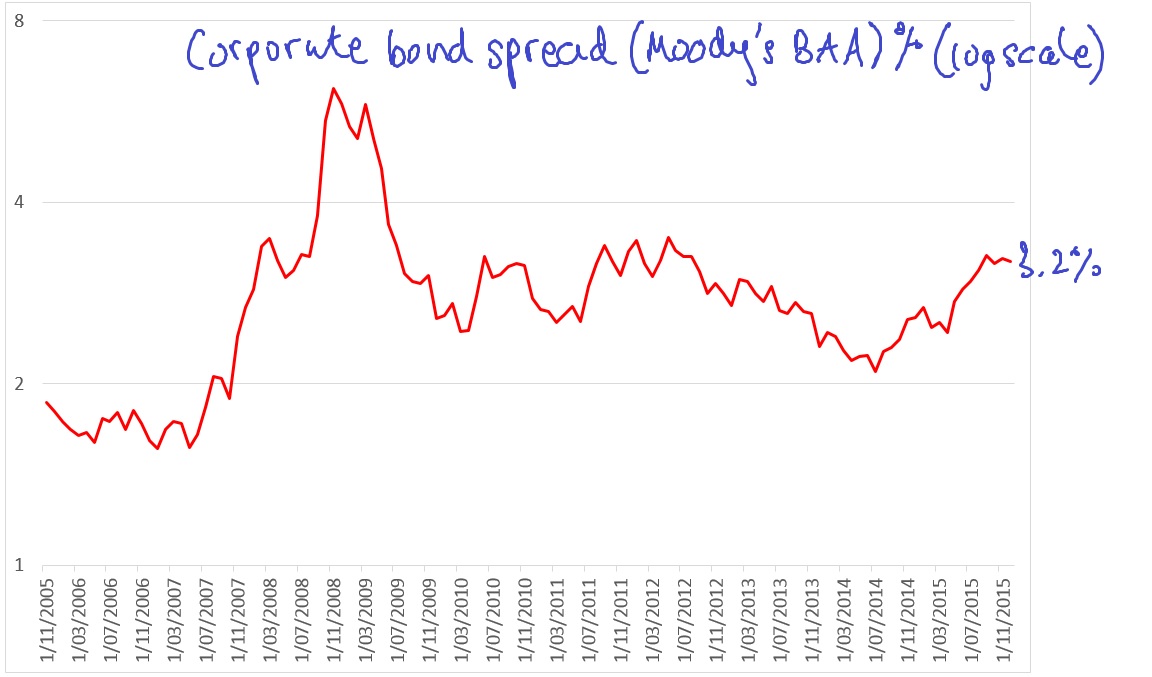

Corporate bond spreads in the United States have been rising steadily over the past eighteen months to be around 100 basis points higher than at their trough in July 2014. This clearly points to a lift in funding costs, but three developments suggest that the corporate credit cycle is not about to tip over yet. Corporate bond spreads are only marginally higher than their average post crisis (See Chart 1).

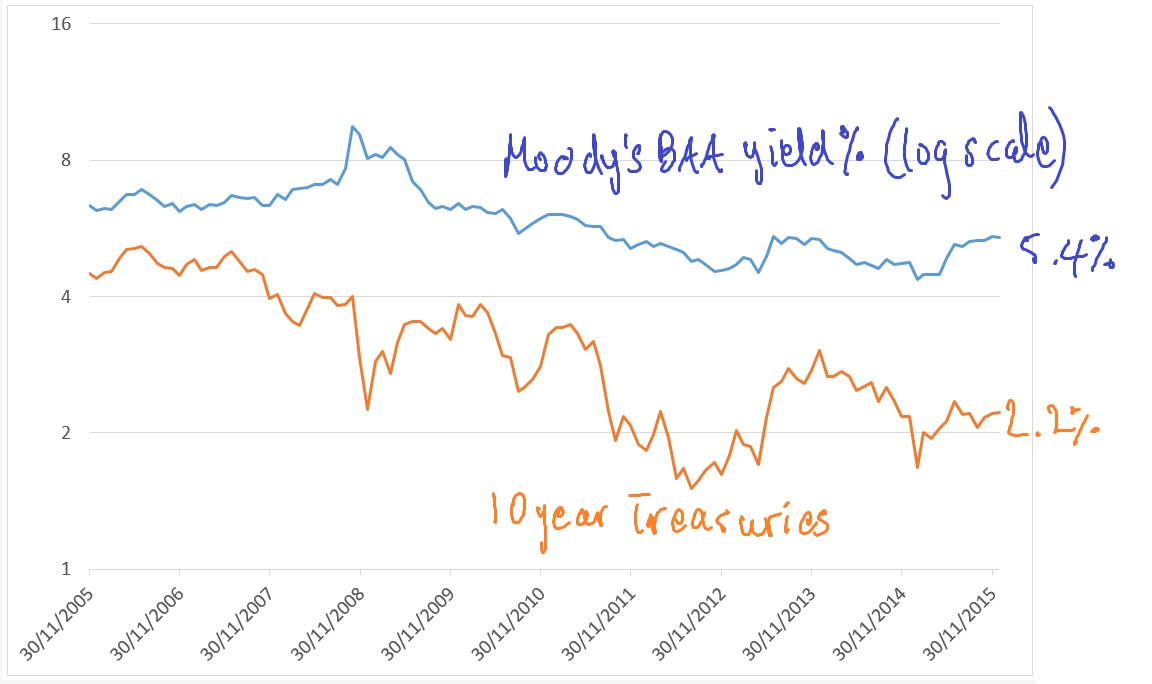

Second, swings in 10 year treasuries have dominated variation in spreads in recent years; the current yield on Moody’s seasoned BAA corporate bonds of 5.4% remains low by the standards of the past decade (see chart 2).

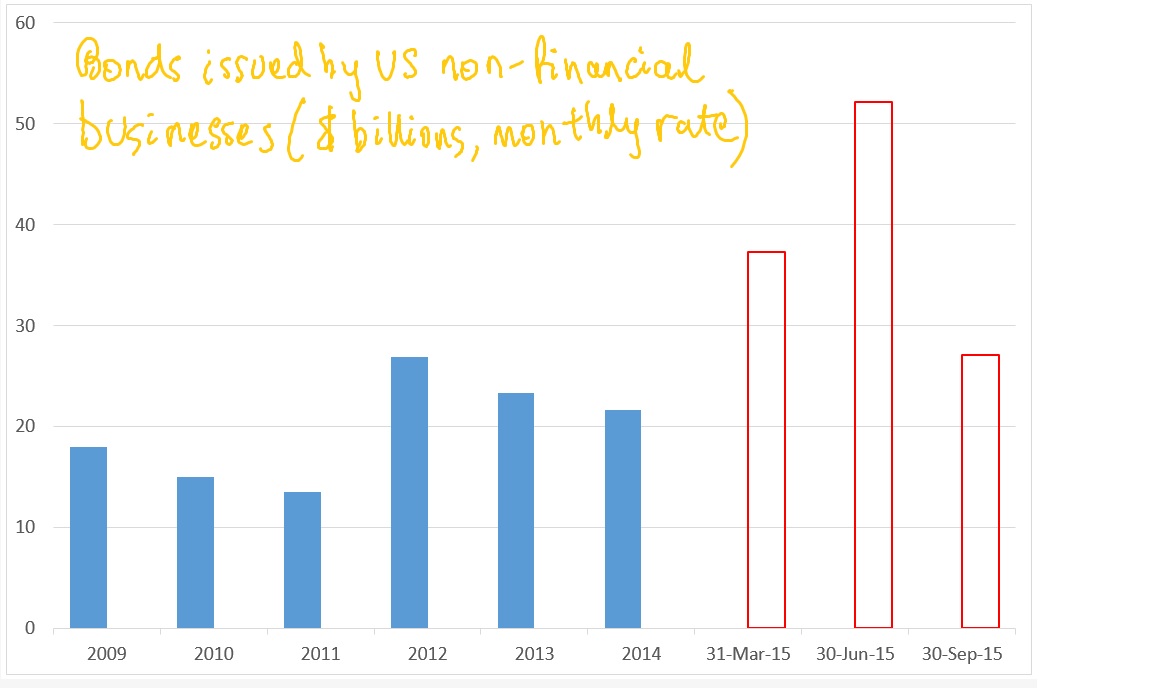

Third, the recently released Financial Accounts show that despite a drop off in the September quarter, bond issuances by non-financial businesses have remained quite strong year to date (see chart 3).

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

3 topics

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management