LICs - adapt or die

The Australian LIC industry feels a bit like Donald Trump in the lead up to the US election. After three great years of growth, both are now behind in the 'popularity polls' and looking for new direction to live another 'term'. With the majority of LICs at NTA discounts of >10%, some of them giving up on the structure altogether and converting to open ended trusts, and the recent Treasury announcement abolishing selling fees, the Australian LIC sector is at a crossroads and needs to adapt or die.

Suffering a similar near death experience 20 years ago was the UK investment company (IC) sector. The sector was written off by market commentators as being "beleaguered and in terminal decline" with NTA discounts of 20-25%, according to Ian Sayers, CEO of the UK Association of Investment Companies (AIC). Ian joined the AIC about then and rode the journey for the next two decades which saw the industry adapt so that it didn't die.

Today, the UK IC industry is in rude health. Having doubled FUM from £95bn in 2012 to £197bn today, the UK is by far the largest listed closed end fund industry globally. It is flourishing with tight NTA discounts after a 10-year sector re-rating (see chart) and innovative new asset classes focused on income. To lift the gloom about the future of the Australian LIC sector (which by the way has had similar Prozac busting growth from $20bn of assets in 2012 to $45bn today) and to learn from the UK about what could be a possible road-map for the future of the LIC industry here in Australia, we hosted a webinar with Ian from his home in London this week.

The key takeaway from the webinar (which you can view here):

NTA discounts in the UK IC sector have never been as narrow as they have been in the last 5 years. While they did widen during the COVID induced selloff in stock markets in March, they have snapped back quickly and today stand at about 5% on average compared to 10-15% in 2010 and 20-25% in the late 90's.

Key to this re-rating for the sector has been:

-

A move to income. Low interest rates = investor thirst for yield. This happened in the UK not long after the GFC as the UK slashed rates to close to zero. Zero rates is now upon us in Australia. Listed closed end vehicles have two distinct advantages over open ended funds in the generation of income for investors.

The first is the ability to pay income out of reserves. Many ICs in the UK have paid consistent dividends throughout the various crises of Brexit and COVID by tapping into profit reserves while their open ended fund cousins slashed income. This income stability has value to investors. The next dividend season in Australia for ASX companies will be interesting to watch if LICs are able to produce more consistent and higher income than equity income open ended fund peers.

The second is the ability to invest in illiquid asset classes like private credit, real estate and infrastructure. Closed end capital can invest in these asset classes as there are no redemptions to worry about. Open ended funds can't (or shouldn't) as they for the most part offer daily redemption windows for investors. All of those private, illiquid asset classes have great income producing qualities. ICs in the UK have brought those asset classes into the investing mainstream to satisfy the income and diversification needs of investors. These ICs also introduced a whole new group of investors to the IC market: institutions (pension funds and endowments) that now make up as much as 40% of the UK IC investor base. These private asset ICs have traded at much tighter discounts to NTA than their listed asset peers. Infrastructure ICs lead the way with almost all of them trading at handsome NTA premiums.

-

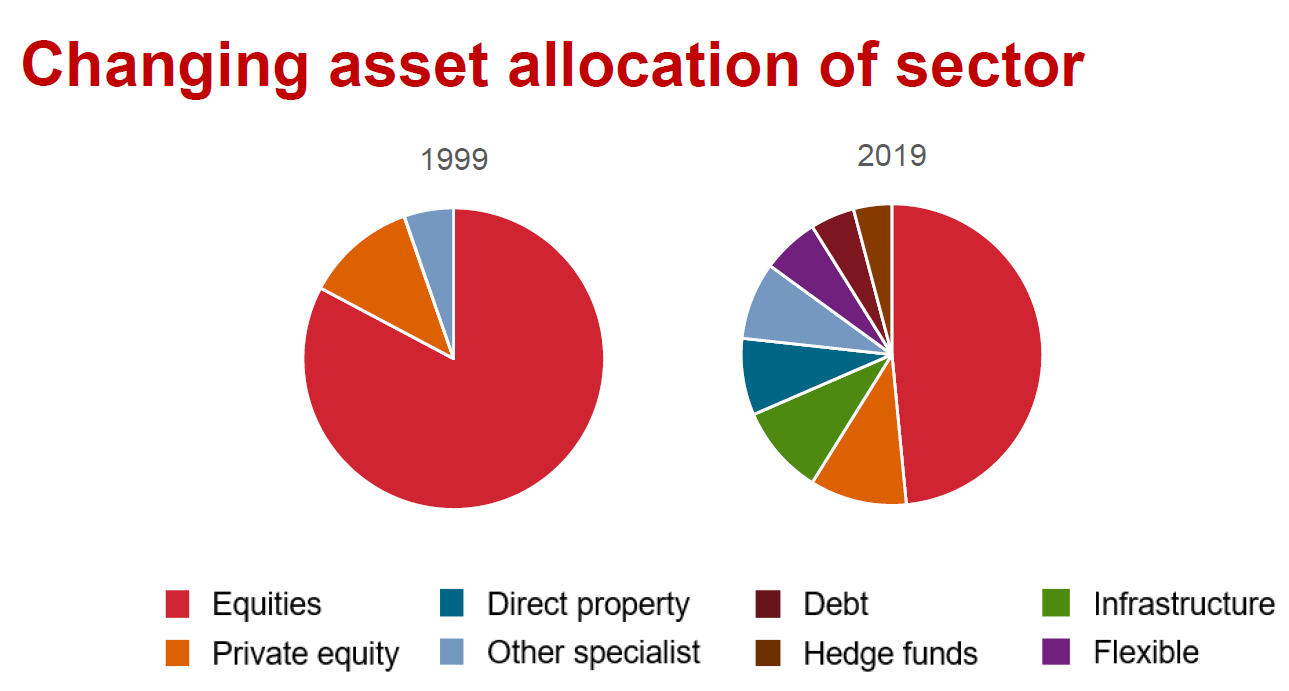

A change in asset class away from listed equities. In 1999, listed equities made up 85% of IC assets in the UK. Today they are <45%. With the emergence of ETFs as an alternate listed vehicle for investors to gain exposure to equities, especially equities outside of the home country bias (global equities), investors started to shun equity ICs in favor of ETFs. ICs managing listed equity portfolios showed no growth over this multi decade period which caused them to become the less than half the industry's assets today (see chart below). Australia's LIC market today is 90% listed equities, where the UK was 20 years ago. Adapt or die.

-

Discount management initiatives. UK ICs took action when the NTA discounts were wide. Of the various initiatives undertaken, the most effective were buybacks and continuation votes. Buybacks only became effective in time. Initially ICs were hesitant to make clear commitments on the size and price objectives of their buybacks. Over time they learnt that the only thing that worked was the Mario Draghi "whatever it takes" commitment to buy shares in large quantity if the share price traded below NTA. Foreign & Colonial and Scottish Mortgage, two ICs that trade at NTA have successfully deployed this "whatever it takes" buyback strategy. UK ICs can buy back stock as treasury shares (able to reissue them later rather than cancel them) which is an advantage over the forever shrinking effect of Australian share buybacks.

Continuation votes, generally agreed at the IPO of the IC, set a fixed term (typically 5 years) at which time shareholders get to vote on whether the Company continues as is, the Manager is replaced or the Company is wound up. This tends to have a 'pull to NTA' effect on the share price as investors know there's a potential exit at NTA at a certain date if the Company is unsuccessful. Perhaps if the costs of raising LIC capital in Australia decline as selling fees are banned, LIC managers (who pay these costs) and LIC directors (who have a contract to honor with the Manager) would be more willing to consider such an initiative.

-

A crisis to remind investors of the benefits of a closed end fund. Ever hear of Neil Woodford ? He was about as close to a fund manager 'rock star' as the UK has. In about a year after he broke out on his own, he had raised >£10bn. That was until he had to shut his open end fund last year when poor performance caused an investor run on the fund and his portfolio of illiquid listed and unlisted equities couldn't be sold to meet these redemptions. The fund has been closed for a year and investors still can't get their money out. Some assets in the fund were force sold at a fraction of their true worth. The media and regulator are having a field day at the expense of the fallen rock star who was forced to apologise via a mea culpa on YouTube. Today his funds have either been taken over to be run by other managers or are being wound up.

The same is true for many UK REITS, shutting their funds during Brexit and COVID when they couldn't meet redemptions as the liquidity in UK property stocks dried up. It takes a crisis like that to make investors realise the true benefits of closed end funds. Yes their share price can trade away from NTA which annoys the hell out of shareholders (and Boards and Managers I might add) but if you have illiquid assets in your portfolio like Woodford did or if redemptions force you to sell out at the worst possible time, that can be far worse for investors in an open ended fund. Woodford and UK property unit trusts during Brexit reminded UK investors of this key benefit of listed closed end funds which has helped the sector's NTA discount narrow.

This fascinating journey of the UK IC industry in the last decade offers plenty of optimism that all is not lost for the future of the LIC industry in Australia in the next decade. This includes how to survive after a major regulatory shakeup like the Royal Commission and the banning of stamping fees, something the UK IC sector successfully travelled through after their own equivalent regulatory over-reach moment in time called the retail distribution review (RDR) in 2013. But the industry will need to take on board some of these changes and improvements to adapt or die. Much like Donald Trump will need to do before the November election to avoid the words he loves to use on others, "you're fired", being used on him.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris is part of the Pinnacle executive management team and responsible for driving the listed products business. Pinnacle’s mission is to establish, grow and sustain a diverse and complementary stable of world-class, specialist investment managers

........

This communication was prepared by Pinnacle Investment Management Limited (ABN 66 109 659 109 AFSL 322140) (‘Pinnacle’). Past performance is for illustrative purposes only and is not indicative of future performance. Unless otherwise specified, all amounts are in Australian Dollars (AUD).

This communication is for general information only and was prepared for multiple distribution. Whilst Pinnacle believe the information contained in this communication is reliable, no warranty is given as to its accuracy, reliability or completeness and persons relying on this information do so at their own risk. Subject to any liability which cannot be excluded under the relevant laws, Pinnacle disclaim all liability to any person relying on the information contained in this communication in respect of any loss or damage (including consequential loss or damage), however caused, which may be suffered or arise directly or indirectly in respect of such information.

The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment. The information in this communication has been prepared without taking account of any person’s objectives, financial situation or needs. Any persons relying on this information should obtain professional advice before doing so. The issuer is not licensed to provide financial product advice. Please consult your financial adviser before making a decision.

Any opinions and forecasts reflect the judgment and assumptions of Pinnacle and its representatives on the basis of information at the date of publication and may later change without notice. Any projections contained in this presentation are estimates only and may not be realised in the future. The information is not intended as a securities recommendation or statement of opinion intended to influence a person or persons in making a decision in relation to investment.

Unauthorised use, copying, distribution, replication, posting, transmitting, publication, display, or reproduction in whole or in part of the information contained in this communication is prohibited without obtaining prior written permission from Pinnacle. Pinnacle and its associates may have interests in financial products and may receive fees from companies referred to during this communication.

3 topics

Chris is part of the Pinnacle executive management team and responsible for driving the listed products business. Pinnacle’s mission is to establish, grow and sustain a diverse and complementary stable of world-class, specialist investment managers

Expertise

Chris is part of the Pinnacle executive management team and responsible for driving the listed products business. Pinnacle’s mission is to establish, grow and sustain a diverse and complementary stable of world-class, specialist investment managers

Expertise

Comments

Comments

Sign In or Join Free to comment