Low-momentum, high-risk stocks suddenly in favour

Market sentiment dramatically shifted in November with the sudden announcement of promising COVID-19 vaccine results and the outcome of US elections. In an effort to get ahead of the changes in company earnings and opportunities that would be expected as life gradually returns to normal, market participants abruptly moved away from stocks that would be expected to thrive amid lockdowns and other restrictions and toward businesses that depend on the resumption of normal life.

We expected market action motivated by increasing certainty about the end of the pandemic to drive up the prices of the stocks that have suffered most during the crisis – but we also realize that this pattern will be limited to a short period. We invest for a longer horizon.

Low-momentum, High-risk Stocks Suddenly in Favor

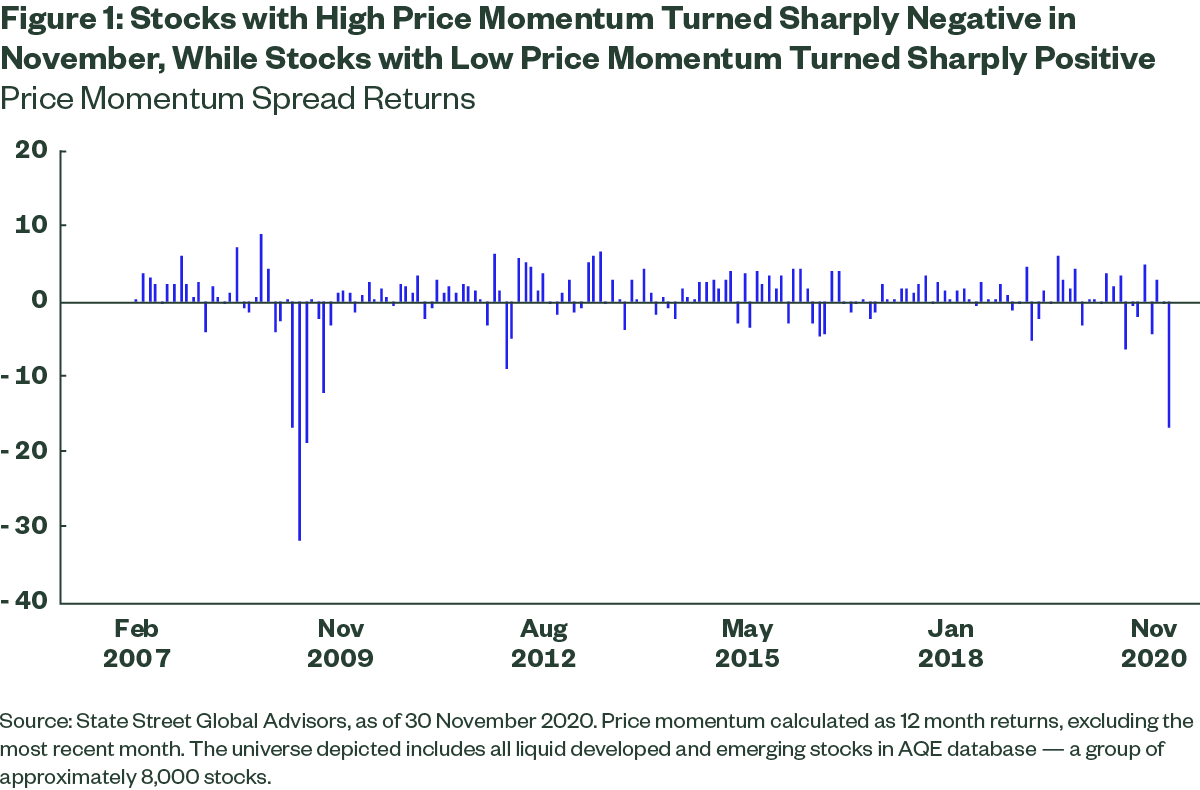

The shift in market sentiment manifested itself in sharply negative returns for stocks with high price momentum and strong positive returns for stocks with low price momentum – in short, a clear example of price reversal (see Figure 1). It’s very unusual to see a reversal of this magnitude – the last time we saw one of this size was in March 2009 – but it is characteristic of price momentum, which has a pronounced negative skew in its return payoff. (Put another way, price momentum has historically generated frequent and consistent incremental positive returns, but the occasions where returns are negative have been much more severe.)

But market movements in November weren’t just about price reversal. In many cases, the kinds of companies that experienced the strongest positive reversal also happened to be very volatile (i.e., very risky) and/or very cheap (particularly when we measure value using deep measures such as price-to-book ratio).

The spread return between high- and low-momentum stocks in the MSCI World universe was approximately 17% in November. But if we get more granular and look at the return of stocks with both low price momentum and high risk, we get an even more extreme spread return of 24%. The stocks that fall in this category of low price momentum and high risk are mostly energy companies, banks, travel and tourism companies, and real estate firms.

Potential Lessons from the Global Financial Crisis

If November does prove to be a turning point for markets, it may be instructive to consider the turning point for the last major crisis – the Global Financial Crisis (GFC) – and consider how factor returns were impacted. When markets reached the inflection point that marked the end of the GFC, price momentum experienced sharp negative returns for three months or more. In addition, value stocks rebounded, with cheap stocks as measured by price-to-book ratio leading for the first few months, followed by an expansion to broader measures of value. Risk was sharply rewarded for the first three to six months, and Quality was generally not rewarded for the first six months following the turning point.

So, if the November rally represents a genuine inflection point for the COVID-19 crisis, our experience following the GFC suggests that:

- High-risk stocks may rally for the next three to six months, but they’re unlikely to continue to outperform over the longer term.

- High-momentum stocks may underperform for the next three to six months, but will likely normalize in the months following.

- Quality may not matter much in markets for the next quarter or so.

- Cheap stocks are likely to keep rallying – starting with stocks that are undervalued on price-to-book measurements and broadening to include more robust measures of value.

Of course, current market and economic conditions are quite different from those in place during the GFC, including aggregate market level (i.e., relative peak versus relative trough), the sectors of the market experiencing the strongest performance (tech and online stocks today, compared with utilities/staples during the GFC), and the size of central bank balance sheets supporting market liquidity. There could also be near-term headwinds for some value stocks (for example, banks due to low interest rates, travel and tourism companies due to changes in travel patterns, and commercial real estate firms due to shifts in work patterns and office space utilization). Even so, we think that the post-GFC period offers some interesting and instructive lessons as we contemplate the post-COVID recovery.

The Bottom Line

Turning points in markets are tough. Investors are rarely positioned for both sides of a turning point. That’s why we’ve built our investment process to look through these turning points and buy the high-quality, reasonably valued companies that are most likely both to survive a crisis and emerge strongly when that crisis has passed.

A shift in sentiment like the one we’ve just experienced can feel painful, but the good news is that it bodes well for the future. If vaccine development and distribution continues on a positive trajectory, we believe that the initial reversal will broaden out to reward not just the cheap stocks that have suffered during the pandemic, but also those truly undervalued companies with strong balance sheets, resilient sources of earnings growth, and sustainable management policies and practices.

With that longer investment horizon in mind, here are some of the sectors where we currently see some of the most attractive opportunities:

- Technology hardware and semiconductors in the US and Japan

- Telecommunications in the US and Japan

- Insurers in the US and Japan

- Pharmaceuticals in the US

- Auto manufacturers in Europe

Access high quality companies at attractive prices

Rather than building portfolios around the stocks weights represented in the benchmark index, our approach explores the market’s full opportunity set, constructing a portfolio based on stocks total return and total risk characteristics. Click to follow button to stay up to date with all our latest insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Many people think equity investing is all about finding companies that offer the best returns. We’re focused on the best way to form equity portfolios to deliver the best risk-adjusted returns, in line with specific return and risk objectives. Our experience is in applying our investment knowledge across as many companies as possible in a highly objective way.

........

The information provided does not constitute investment advice and it should not be relied on as such. It should not be considered solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your tax and financial advisor. All information is from SSGA unless otherwise noted and has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

The views expressed are the views of Active Quantitative Equity through December 10, 2020 and are subject to change based on market and other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected.

Investing involves risk including the risk of loss of principal. Quantitative investing assumes that future performance of a security relative to other securities may be predicted based on historical economic and financial factors, however, any errors in a model used might not be detected until the fund has sustained a loss or reduced performance related to such errors.

The trademarks and service marks referenced herein are the property of their respective owners. Third-party data providers make no warranties or representations of any kind relating to the accuracy, completeness or timeliness of the data and have no liability for damages of any kind relating to the use of such data.

The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA’s express written consent.

© 2020 State Street Corporation.

Many people think equity investing is all about finding companies that offer the best returns. We’re focused on the best way to form equity portfolios to deliver the best risk-adjusted returns, in line with specific return and risk objectives. Our...

Expertise

Many people think equity investing is all about finding companies that offer the best returns. We’re focused on the best way to form equity portfolios to deliver the best risk-adjusted returns, in line with specific return and risk objectives. Our...

Expertise

Comments

Comments

Sign In or Join Free to comment