Markets stage a late recovery

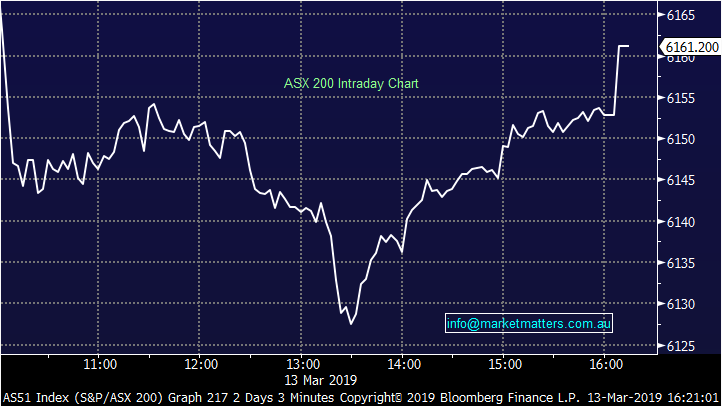

Yesterday’s momentum to the downside certainly continued through to today’s session as the local market opened strongly lower despite the UK & US markets both trading higher overnight. The ASX200 traded to a 2-week low early in the afternoon before staging a decent recovery over the last few hours including a futures led kick in the match which added 9 points.

Winners today were the losers of yesterday – Appen (APX) bounced back after its post capital raising slump to add 5.1%, whilePerpetual (PPT) just about clawed back yesterday’s softness putting on over 4% today. Sectors were mixed, Energy the worst off thanks to a UBS note we discuss below.

As a reminder, we discussed three new opportunities in the income report today – click here to read.

If any of these interest you and you wish to seek an allocation please contact James at jgerrish@shawandpartners.com.au or call (02) 9238 1561.

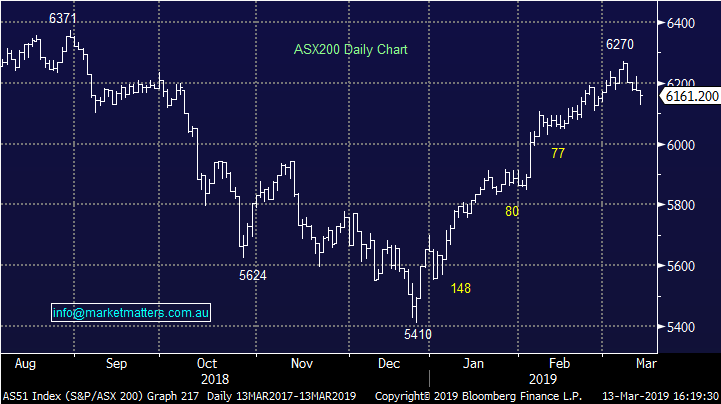

Overall today, the ASX 200 lost -13 points or -0.22% to 6161. Dow Futures are currently trading down -52pts / -0.20%.

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE

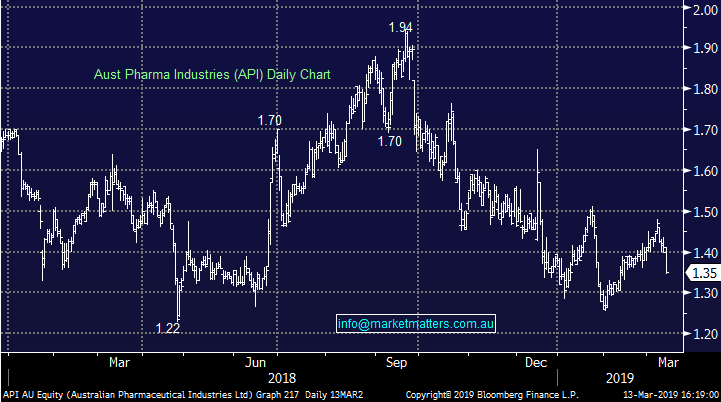

Two of the listed pharmaceutical wholesalers have slumped today following an announcement by the Sigma (SIG) board that they would not recommend the takeover offer by rival Australian Pharmaceuticals (API). Late last year, API offered $0.23 in cash and 0.31 API shares for each Sigma share, which as at yesterday’s close was worth about $0.66, 8% above Sigma’s close price. We wrote about the deal here. Today Sigma fell -12.3%, while API fell 3.57%.

Australian Pharmaceuticals (API) Chart

The deal came at a tough time for Sigma, which had recently lost a big contract with Chemist Warehouse. In the release, the board talks to the business review the company had completed, which noted “cost efficiencies of over $100 million” were identified in its business, compared to the $60m/pa efficiencies from FY22 seen in the merger. Additionally, through transformation, the EBITDA lost from the Chemist Warehouse contract would be replaced by FY23. In rejecting the proposal, the board also noted Sigma may look at corporate deals of their own as they expect “to have a strong balance sheet with minimal debt and will have upside opportunities from acquisitions.”

Sigma Healthcare (SIG) Chart

Major shareholders Allan Gray Investments clearly were disapproving of the board’s decision, the board could have taken the easy route and seen the immediate value uplift for shareholders by accepting the deal. Instead they went with the tougher route. In fairness, the proposal would have seen rigorous regulatory scrutiny and would likely had a number of hurdles to jump. We are cautious.

Broker Moves: UBS spent some time discussing the energy sector today, cutting their oil price deck which resulted in downgrades to Woodside and Santos. The changes were only marginal, revising this year’s assumed price down ~4%, while amending next year ~1% lower. The bank believes oil will largely trade between $US60-80/bbl despite noting economic headwinds, solid US production and a soft demand outlook. In this range, oil producers are not seen as incentivised to drastically change production levels.

· AusNet Downgraded to Hold at Morgans Financial; PT A$1.73

· Woodside Downgraded to Neutral at UBS; PT A$35.25

· Santos Downgraded to Neutral at UBS; PT A$7

· Carnarvon Rated New Buy at Canaccord; PT A$0.50

· Janus Henderson Upgraded to Overweight at JPMorgan; PT $29

Never miss an update

Stay up to date with the latest news from Market Matters by hitting the 'follow' button below and you'll be notified every time I post a wire.

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

2 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets