May Review: Steady Markets Deliver Small Gains

Equities and credit delivered gains in May, commodities were mixed. Japan, France and Germany posted good GDP numbers, forward looking data for the US is weak. US equities are looking overvalued and a range of prominent investors have come out as selling down or going short. High yield credit is seeing strong issuance, but there are warnings that all is not well.

Most risk assets posted small gains in May. In equities Japan (3.4%) and Australia (2.4%) performed best with more modest results for the US (1.5%), Europe (1.2%) and China (0.4%). Credit also posted small gains, but the near record level of new issuance in May shows sentiment is now much stronger. Commodities were mixed with US oil (7.0%) and natural gas (5.1%) jumping whilst iron ore (-24.2%), copper (-8.2%) and gold (6.0%) fell.

In economic news Japan avoided another recession with GDP growth of 1.7% for the quarter. However, there was an extra day due to the leap year which bumped up the number and it comes after a -1.7% quarter. France and Germany reported solid quarterly numbers of 2.4% and 2.7% respectively. PMI surveys from the US were soft and for China were largely unchanged. The Cass Freight Index, US rail freight movements, US air freight and the CPB World Trade Monitor continue to flash amber. Temporary employment levels and online job ads in the US are weaker.

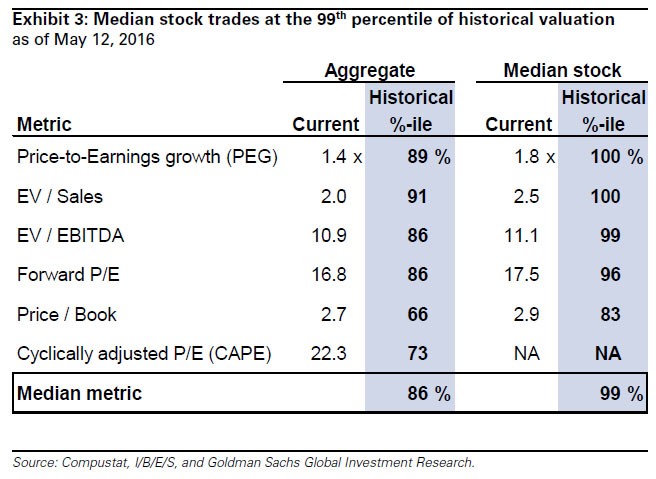

A seminal piece by Goldman Sachs this month found that the median US stock is as overvalued as it has ever been. The table below shows a range of common valuation measures, with all of them saying now is a better time to be selling than buying. The one argument that runs against this is that interest rates are expected to be low for a long time yet, so on a relative basis stocks aren’t that bad. It’s not just a US phenomenon, shares in Europe have also risen much faster than earnings in recent years.

There’s been a series of well-regarded investors publicly saying that they are selling down or have gone short including Stanley Druckenmiller, Jim Chanos, Carl Icahn and Sam Zell. Michael Burry, highlighted in The Big Short, recently sold all of his bank stocks. Uber bear of the month is Milton Berg, who outlined his case for no real returns for the next 30 years. Uber bull of the month is William Lee, who’s buying shares of Chinese banks.

The chase for yield is back again in the US high yield markets. A co-founder of the private equity firm Apollo remarked that the debt markets are “back in all their glory” and that “the good times are rolling again, at least for this month”. Loans that were stuck at the underwriting stage earlier this year are being cleared, though deep discounts were required to get some away. The regulatory limit of six times debt to EBITDA is being somewhat circumvented by banks lending to non-banks that then lend to the ultimate borrowers.

There’s a few party poopers though, Bank of America has 9 reasons why high yield debt is overpriced and Antipodes Partners is concerned about the record high levels of leverage and the poor use of debt. Several articles highlighted the increasing levels of debt and decreasing levels of cash held by US corporates, particularly when the top 1% of companies (which have very large cash balances) are excluded.

An interesting development is dealers using high yield ETFs to access the underlying bonds, which works well when prices are rising but could create problems if they are falling. The gap between yields on energy bonds and other sectors is narrowing, which seems to be a bet that oil prices are heading higher.

In the chase for yield in US municipal debt tobacco bonds have been the big winners up 51% since 2014. These aren’t without risk with Fitch to stop rating tobacco bonds as their repayment is “too unpredictable”. Detroit has barely made it out of bankruptcy but has just found another hole in its pension plans. It’s schools could be bankrupt this year. Prisons in Illinois have stopped paying for food and water due to budget disagreements.

The Oil price continued to rise in May helped by a substantial amount of production being offline in Canada, Libya and Nigeria. There’s also uncertainty around Venezuela being able to maintain production as it’s society is collapsing. The rally isn’t quite as clear cut as might be expected. Contracts for short term deliveries have certainly risen, but the forward prices beyond 2019 are lower. It’s also interesting that China has something of a glut developing. China has lent to several emerging market oil producers and as the oil price has fallen they’ve had to deliver more barrels of oil to make their repayments. From Venezuela alone, China is owed $37 billion.

On the subject of Venezuela, it is continuing to sell down its gold reserves in order to pay some of its bills. Law enforcement has broken down with 74 reports of vigilante killings so far this year. The currency has devalued so much that thieves can’t even be bothered stealing it. Coca-Cola has stopped production as it can’t get hold of sugar and the largest beer producer has also shutdown production.

The big news from China was the comments by the “authoritative person” on the front page of the Communist newspaper. Debt was called the “original sin”, “the recovery will be L shaped” and there was a warning that trees cannot grow to the sky. It wasn’t completely negative, the source believes that the Chinese economy still has enormous potential and resilience. Speculation mostly centres on President Xi being the “authoritative person” but even if it isn’t him, he would have signed-off on comments this controversial in a format this public. Whilst it’s ok for the authoritative person to be bearish, it’s not ok for journalists with another crackdown on economic commentary.

In light of those comments, the devaluation of the Yuan to the lowest in five years is very interesting indeed. The increasing demand for Bitcoin in China might be signalling that another round of outflows is kicking off. The main economics agency warned Chinese companies not to issue offshore debt, at a time when Chinese companies are dominating issuance of US dollar and Euro bonds by Asian borrowers.

Chinese wealth management products (WMPs) continue to create concerns. The latest trend is to use WMPs to invest in other WMPs, creating a risk of cascading defaults and liquidity runs. Comparisons to pre-crisis subprime CDOs are logical, the underlying credit quality is often rubbish and the layering of risk multiplies the potential problems. Then there’s the risk of complete fraud, as was the case with Wealthroll, a $6.1 billion issuer of WMPs. It’s far from alone though, close to 1,000 online lenders have collapsed in the last year.

On one measure of credit risk China is the worst in the world, easily beating Turkey, Canada and Brazil. Another article noted that China, the US and Japan all have debt bubbles, each with their own nuances. The estimates on the size of the non-performing loan (NPL) problem in China range from 2% to 20%, but some small banks are already above 20%. Natixis found that 17% of Chinese companies have an EBITDA to interest ratio of less than 1. Remember that you can’t pay interest with EBITDA, the percentage would be much higher if operating cashflow or EBIT was used.

SocGen thinks there’s $1.2 trillion of loan losses coming, which could wipe out over half of bank capital. Regulators are cracking down on receivable financing, which could force banks to hold ten times more capital against those assets. It’s not just Chinese banks that are thought to be mismarking their assets, insurance companies are suspected of overvaluing assets as well. In case you are getting excited about investing in NPLs in China, remember that enforcement for foreigners is near impossible.

Chinese credit ratings may as well be used for toilet paper, with Bloomberg finding that 57% of Chinese AAA ratings don’t meet the ratios needed for an investment grade rating if state guarantees are ignored. China bulls say “don’t worry the government has your back”. China bears say “look at the defaults by state owned entities this year”. It’s this sort of dichotomy that can cause a massive yield gap between onshore and offshore bonds. Perhaps Chinese investors are catching on though as bond sales have dropped off dramatically in the last two months.

Full marks to the Singaporean banking regulator who revoked the licence for Bank BSI after it was caught aiding money laundering. They are also looking at criminal charges for key individuals. On the scale of white collar punishment both of those items score top marks and will influence the behaviour of others. Cancelling the licence stops a business in its tracks. Jail for individuals means they can’t hide behind the corporate veil. Large fines are the next step down, but they’ve became par for course now in the US and Europe and can be seen as the cost of doing business. The inability of US regulators to get convictions and jail time for individuals is one of the reasons that banks seem to keep reoffending. Plenty of lessons there for Australia’s corporate watchpuppy ASIC.

European banks continue their travails with Italy’s Unicredit looking for a new CEO as well as €6 billion in new equity, which is dwarfed by its €80 billion in NPLs. Things are so bad for other Italian banks that the government has said it will accept shares instead of cash interest on debt given in previous bailouts. Spain’s Banco Popular also sacked its CEO and is looking for €2.5 billion in new share capital. That might not be enough, as it has a higher than average level of NPLs and lower than average level of provisioning against them. These two banks are now competing with Deutsche Bank for the lowest price to book ratio.

Speaking of Deutsche Bank, its CEO wasn’t happy with Moody’s downgrade of its rating to Baa2. His claim that “we have enough capital to repay all of our debt four-times over” doesn’t align with the liabilities being 27 times the size of the book value of equity and 72 times the market capitalisation. Zero Hedge loves to pull out the comparisons with Lehman Brothers, who made similar statements to reassure markets in the year leading up to its demise.

Only eight years after excesses in US home lending kicked off a financial crisis banks are at it again. Dutch banks have average LVRs of 101%, Barclays is offering 100% LVR loans in the UK and Wells Fargo is offering 97% LVR loans in the US. A syndicate of almost 60 banks is lending $7.7 billion to Glencore at Libor + 0.95%.

Lending Club made headlines throughout May. Early in the month it revealed it had bought back $22 million of loans after it misstated their characteristics to the buyer. It then sacked its CEO. Comparisons immediately began with US subprime originators who went bankrupt when they couldn’t buy back loans they misrepresented and sold. The share price tanked so much that at one point the market capitalisation was $1.3 billion for a company with $800 million of cash in the bank. The share price recovered after four Singaporean companies bought shares and it was revealed that Citigroup is considering buying loans.

I wouldn’t be surprised if one of the banks or credit card companies announces a take-over offer soon. Marketplace lending is one of the few growth areas in finance, it has very high returns on equity and those returns would be even higher if the cost of funding was reduced to investment grade levels. That strategy would solve the biggest issue for marketplace lenders, getting the funding to match loan applications.

As a result of capacity limits, Prosper has recently cut its staff by 28% and closed some offices. By solving the funding constraints marketplace lending has the potential for a positive spiral, as lower rates attract better quality borrowers, that default less and can justify lower rates. If you are new to this area, Tracy Alloway gave an excellent wrap-up of the sector’s history and recent issues in a podcast. Competitors aren’t taking the threat lightly, Visa has plans to get millennials to take on more debt.

Hedge funds have copped a hiding recently, including from Warren Buffet, and rightly so. Several big names have suffered outsized losses this year. When you have delivered low returns and charged high fees investors won’t be happy. Some have gone as far as saying that “hedge funds are a compensation scheme masquerading as an asset class”. Private equity funds have also been in the spotlight, with a report accusing managers of dodging taxes and over-charging fees. Investors may be considering switching to Vanguard which is offering institutional investors index funds at 1 basis point per annum. The risk with that swap is that the timing could be wrong. Equities are at elevated levels now so the outperformance by hedge funds in down markets might be needed soon.

There’s clearly been a lack of diversity in ideas, with hedge funds crowding into a grab bag of underperforming shares like Valeant and SunEdison. It has long been argued that there’s a lack of talent, there aren’t 10,000 geniuses available to run the 10,000 available hedge funds. Institutional investors crowding into the biggest managers hasn’t helped, many of these are now so big they’ve lost their ability to be nimble. Research has usually found that managers with less than $1 billion in assets outperform their larger peers, although another study found that younger managers outperform more established managers.

The IMF and the ECB cobbled together yet another bailout package for Greece, but this one might only last until October. The IMF sees the prospect of Greece delivering enough of a surplus to amortise its debts as a “far-fetched fantasy” and is calling for debt compromises. Europeans, particularly Germany, see compromising principal as crossing a red line. The IMF is right on this point, Greece is paying comparatively less in interest than Italy and Portugal as a result of the very low interest rates it was granted in previous deals. Without reducing the principal owing, Greece can’t make headway in reducing its debts. As a result of failing to implement reforms and strike a deal with its creditors Greece has been raiding the health department and public utilities to pay salaries.

The discussions about central banks, quantitative easing and helicopter money jumped the shark in May. The chief central banker for Lithuania said of his fellow European central bankers that “we are magic people” that can “pull rabbits out of the hat” and can deliver “surprises for the market” as required. Some might think central bankers are taking drugs when they say things like that, but Nassim Taleb thinks monetary policy is like drugs and the stimulus effect is wearing off. Fitch thinks that helicopter money relies on faulty assumptions and Mark Carney says it exacerbates Ponzi schemes. The experience of Denmark shows that negative interest rates don’t work. An economist from the BIS argued that low inflation is ok but low interest rates aren’t. In a taste of what happens when money policy goes wrong, ATMs in Zimbabwe are running out of US dollars and the population doesn’t trust the new currency.

For those interested in US politics Nassim Taleb has prepared a cheat sheet comparing Hillary Clinton and Donald Trump. The New York Post wrote how corporate America bought Hillary for $21m. The Creator of Dilbert put forward six reasons why Trump will win. Trump said the unspeakable, that the US government might need to renegotiate its debts. Barack Obama’s legacy: the most hostile and least transparent President ever according to journalists including 31 times more jail time for whistleblowers than every other US president combined.

Written by Jonathan Rochford for Narrow Road Capital on May 31, 2016. Comments and criticisms are welcomed and can be sent to info@narrowroadcapital.com

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

5 topics

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Narrow Road Capital is a credit manager with a track record of higher returns and lower fees on Australian credit investments. Clients include institutions, not for profits and family offices.

Expertise

Comments

Comments

Sign In or Join Free to comment