Mining Cycle: Poised, just like equity markets

It goes without saying that the last few months have produced unprecedented 1 market volatility. Aside of wars, COVID19 is the most monumental disruption to the global economy during the modern industrial era. So far in 2020 we have experienced several new extremes:

- Latest employment figures are the worst for multiple decades, possibly since the Great Depression

- Governments and Central Banks have announced the largest ever stimulus and quantitative easing measures, with interest rates now virtually zero

- Coming off record highs in February, March was the worst month for stock markets since 1987 with global equity markets down 40%, in the fastest fall of that magnitude in history…

- And then April was the best month ever, recovering more than half of these losses.

And on the tail of all that upheaval, perspectives in the market are almost polarised – investors are spying either a further correction, or that we will all be saved by the deployment of stimulus against the horrible spectre of zero returns on cash which makes “wait and see” distinctly unprofitable. The cycle for the mining industry is, for the foreseeable future, linked to equities – if the market were to experience a further leg down, mining equities would be sucked with them in a likely liquidity squeeze.

These thoughts are not to hitch a wagon to either market scenario, rather to consider the consequence for the mining cycle under both.

A little or a lot – extents of market collapse

There have been very few winners from the COVID19 correction, and many losers. The table below compares the main ASX sectors and indices, key mineral commodities and the “big 4” US based technology firms.

.jpg)

Gold – “more interest than product”

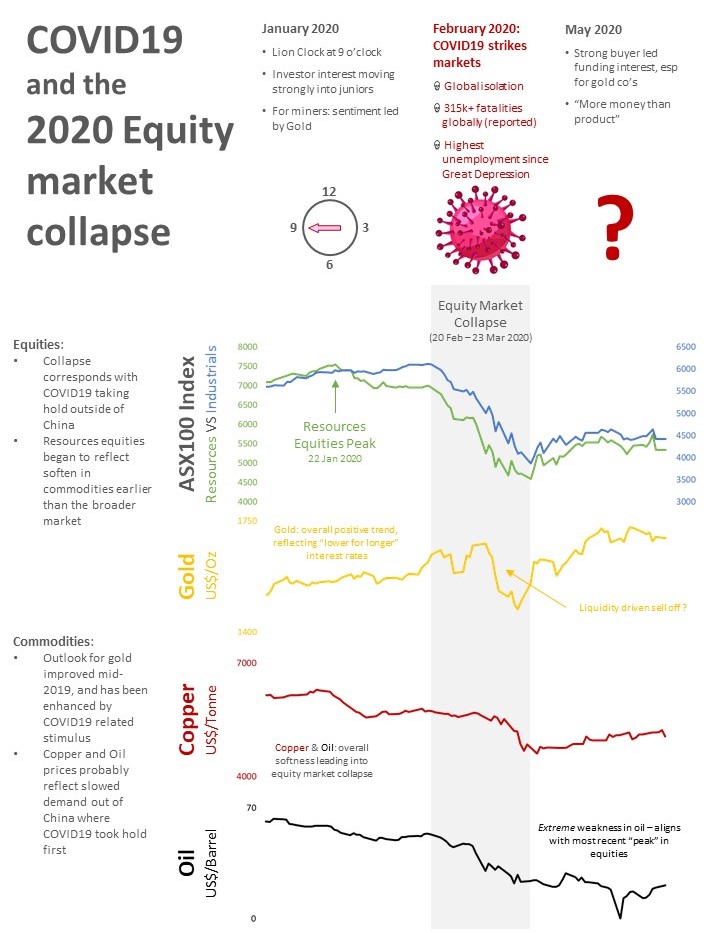

The strongest area of the Australian market by a wide margin has been the gold sector, with similar performance evident on other exchanges. Gold took on a renewed shine in mid-2019 when the global outlook for interest rates weakened. Investor interest in gold has surged since the emergence of COVID19 under the combined effects of massively expanded quantitative easing (which encompasses official interest rates settings being lowered to almost zero) and COVID19 related uncertainty.

This renewed interest is manifest in increasing M&A activity in the sector and fund raisings across the spectrum of gold companies, including pre-development or small producers looking to raise funds for growth. Capital raisings that have taken place have been very well subscribed, and there is an apparent increase in small companies reporting unsolicited offerings of capital from investors or brokers, a phenomenon that was all but absent from the junior mining market since circa 2011. It certainly appears that there is a large pool of money trying to find a home in the relatively small gold space. One Canadian gold exploration CEO recently reported that in the gold sector there is presently “far more interest than product”.

Liquidity: Crash or correction?

Media headlines from late February through mid-March described a crash in equities markets. Substantial falls in percentage terms are the most synonymous aspect of stock market crashes, so “crashing” is entirely consistent with overall falls of circa 40% and trading days like 16 March when the All Ordinaries index fell 9.5%. However, after a 37% fall in the All Ordinaries Index, there has been a 24% rebound leaving that index down only 22%. A very similar pattern is reflected by other major stock markets and the US market has recovered even more ground. Language in commentary has subsequently adjusted to describe a “correction” rather than a crash.

An equally important aspect of equity market crashes is an extreme contraction of liquidity – an overwhelming move to cash which is driven by fear and lasts until fear exhausts itself in capitulation. There has been a brief episode when liquidity dropped during mid-March (when investors were selling out of just about everything except for toilet paper), but that was over almost as soon as it began and liquidity quickly returned to the market. The price recovery may be due to bargain hunting behaviour or the effectiveness of government monetary policy with negative interest rates for cash.

Typical indicators of liquidity for the mining sector are reflecting a surge in liquidity since January 2020:

- Exploration – activity measures and anecdotal indications show a decrease, but mostly related to COVID19 safety measures, and not a lack of funding. A number of notable discovery stories have been able to raise funds with ease, over a range of commodities

- Merger and Acquisition activity was taking on a healthy acceleration in 2019 and 2020. There is nothing to indicate this has abated, with several sizeable deals announced that strongly support the continuance of the trend

- Capital raisings – especially for small producers or explorers, appear to be proceeding with an abundance of investor interest

These indications are contrary to the availability of investor funds during a typical market crash. Fear was fleeting and was quickly replaced by greed. As events unfolded in March it certainly felt appropriate to describe the event as a crash, but the robust rebound raises questions defining the current COVID19 crisis as a “correction”. It is possible that the recent rebound is merely a “dead cat bounce”, super-charged by extraordinary government intervention. Without delving deeply into “what ifs” (of which there are many), ultimately the future market reaction to reports of actual economic impact of COVID19 and company earnings will only be revealed as events unfold.

Historical comparisons

The magnitude of negative performance of mining equities through February / March is on a par with historic mining busts. Previous mining busts have been brought about either by conditions intrinsic to the mining sector or when mining equities have been caught up in a broader equity market crash, and its worth a quick review of mining downturns through the last 40 years as to which is which:

1987: Very rapid equity market collapse

- Liquidity for miners recovered in a short period and the consequent bust was short lived

1997: Mining industry induced collapse

- Mining equities fell by 41% over almost 18 months commencing mid-1997. In the same period the rest of the market trended positively

- Sentiment toward explorers had been mortally wounded by the Bre-X scandal which broke several months before the ultimate peak for mining equities, and whilst ultimately the collapse was linked to the currency crisis in South East Asia, investors were more than happy to go looking for other forms of speculative investment

- Funding of exploration suffered for 3-4 years, while traditional exploration supporters were distracted by dot-com wonders

2008: Very strong equity market collapse resulting from the Global Financial Crisis

- Mining equities fell by 57%, in line with the rest of the market

- The aftermath of the GFC saw the deployment of stimulus and quantitative easing, and the world learned the new expression “too big to fail”

- Consequent return of liquidity was rapid

2011: Mining industry induced collapse

- Longest and deepest mining bust in living memory, where mining equities lost 67% in just under five years, whilst the rest of the market put on 32% in the same time

- Sentiment toward miners tipped in May 2011, in an overflow of investor frustration toward irresponsible investment in growth (both M&A and expansion)

2020: Fastest ever equity market collapse

- Largest ever stimulus

The historical experience gleaned from these episodes tells us:

- Mining downturns induced by broader equity market collapse (1987, 2008) are shorter in duration in comparison to downturns brought about by conditions within the industry (1997, 2011)

- This is because liquidity returns to mining (and exploration especially) very slowly when investors have fallen out of love with the sector, but can reappear quickly (right after the crash concludes) if the event was a broader market crash

- The return of liquidity can be even more aggressive where stimulus is being deployed (2008)

(note: percentage movements of mining equities or the rest of the market are based on movements of the ASX100 Resources and Industrials Indices during the respective timeframes)

Mining bust or back to business?

The 2020 mining equities collapse has been a broader equity market event, and so whatever happens next in the equity market we expect will directly impinge mining equities performance. In the lead up to COVID19, a very healthy level of investor interest was being observed toward the sector manifest in a re-emergence of investor interest in Canada and globally investors taking greater interest in earlier stage companies. M&A activity was indicating companies were interested in growth. Much of the activity was within the gold sector, but the cycle works on liquidity irrespective of whether it is focused or spread out. Risk appetite was increasing, and the Lion clock was at 9 o’clock.

In the midst of the COVID19 equity market collapse, there were clear signs that a crash was taking place, indicative that the Lion clock should be set to 12 o’clock. The enormous economic impact that COVID19 is likely to have, and an expectation that such a significant collapse in equities would lead to a decrease in liquidity – felt most keenly by companies that rely on liquidity to fund their activities. As it has turned out so far, the opposite has been the case – equity markets generally have recovered more than half of their losses, gold indices are above their February peaks and it appears that liquidity has surged, rather than fallen away within the gold space. Further, many aspects of the stimulus are focussed on infrastructure, which is expected to be supportive of increasing demand for metals.

The equity market is sensitive to earnings of companies and liquidity, but in the current environment it is challenging to determine which will have the ascendancy. There is a large proportion of investors who cannot accept a zero return on cash, these investors remain invested in the equity market, waiting to judge earnings and economic reports as they are delivered over the coming months reflecting the possible supportive impact of stimulus measures.

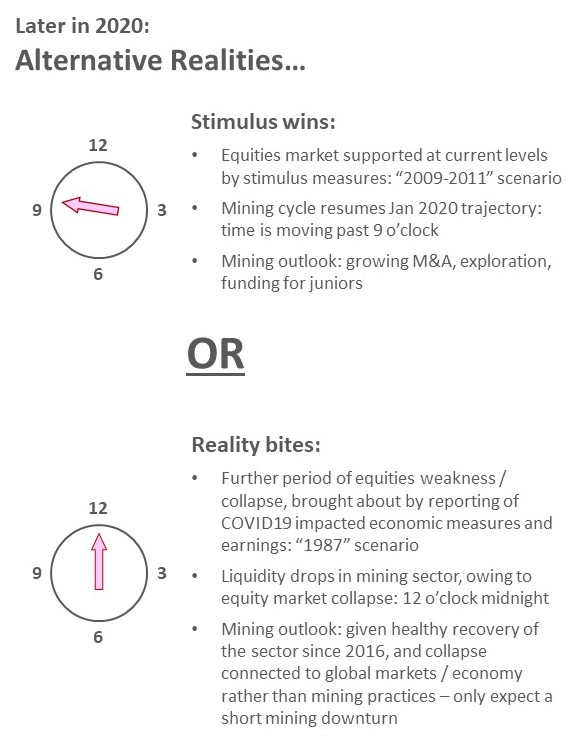

There are two relevant scenarios that could play out:

- “Whatever it takes” stimulus provides enough of a back stop that whilst economic measures and earnings are severely damaged, the equity market looks through those to an expected recovery. This would see the market trade on an historically high price / earnings ratio for the period until we recover “normality”

- Economic news and earnings reports cause further equity market decline, including mining equities

Under either scenario the mining sector moves into the next phase of the market both in reasonable health and with growing investor support (led by gold). If stimulus is victorious and supports the market, then the Lion clock will likely be just past 9 o’clock, reflecting the jump in liquidity we have seen, with conditions most similar to circa 2009 after the GFC. If we experience further equity market weakness, the effect on liquidity is expected to end the mining cycle, so the clock would be at 12 o’clock midnight – a mining bust. The present collective balance sheet of mining companies is in relatively good health having avoided over-leverage, and recovery from this crash could be expected to be far more rapid for the industry as a whole than the last mining bust (2011).

This report is an extract of Lion Selection Group (ASX:LSX) report for the quarter ending 30 April 2020, the full report can be obtained here.

Whilst there are plenty of uncertainties including the potential for further equity market weakness, from a Lion perspective, we feel confident about the outlook for our most significant investments:

- Massive and accelerating monetary expansion by central banks and extremely low interest rates will continue to focus more attention on hard assets like gold

- Growing investor appetite for gold, and gold producer appetite for new projects

- Nusantara’s partnership with Indika positions the company strongly to complete funding required for development

- Pani is emerging as a world class gold project, of which there are very few in the pre-development space

- Following several asset sales during 2019, Lion is well funded for its expected commitments to these positions

Footnotes:

- And chronic overuse of the word “unprecedented”

- Not a typo: West Texas Intermediate fell to a low closing price of 0.9c a barrel on 20 April. The recovery since, whilst still to an anomalously low price, is an enormous percentage gain from almost nothing

Get investment ideas from industry insiders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

2 topics

1 stock mentioned

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Geologist, mining investor, watchful commentator, bicycle collector and father of three.

Expertise

Comments

Comments

Sign In or Join Free to comment