Narrative versus the facts

Value investors, value indexes and value stocks have underperformed over the last three years and in 2020. In fact, value strategies across the globe have underperformed at an increasing rate for most of the post-GFC era. Various reasons for this unusual phenomenon have been widely discussed, but the following wire examines the detrimental effect of poor earnings growth on value stocks and strategies.

Many commentators argue that capital-light, digitally enabled growth stocks have delivered faster earnings growth than more mature, sometimes capital-intensive value stocks. They also argue this trend will persist, given the post-GFC continuation of low interest rates and secular stagnation.

Such a dynamic would certainly explain the divergence of prices on the ASX, where value indexes (such as those maintained by MSCI) have lagged the index and growth indexes vary dramatically. And it has become received wisdom. The only problem with this “fundamentally based” explanation of the recent two-tiered market is that the facts show the opposite.

Value portfolios have delivered superior fundamentals, with more than 100% of the underperformance attributable to sentiment, that is, relative multiple inflation by growth stocks.

To illustrate this, we can dissect the relative performance of portfolios into two categories.

Firstly, earnings growth and dividends paid together represent the fundamental return on the assets owned. And in the absence of multiple changes, they determine the total return for investors – this fundamental factor is determined by the companies held in a portfolio, not by the market.

Secondly, of shorter duration and driven by investor sentiment, we have changes to the multiples applied to earnings of value and growth companies.

The MSCI maintains growth and value indexes for the

ASX, including forward EPS series that allow us to disaggregate observed

returns between fundamentals (earnings/dividends) on the one hand, and

sentiment/multiples on the other. Please note that the fundamental return

measured by MSCI is a combination of the performance of the stocks in each

index at various times and the value and growth portfolio construction process. It is thus applicable to actively constructed value and growth portfolios.

As always, any analysis is sensitive to the starting point. The data below represent the entire low-interest rate/secular stagnation period, but without starting at the GFC lows (on average, value indexes tend to be more cyclical than growth indexes, so commencing in 2008 or 2009 might introduce a positive bias towards value). Given that globally value started to lag growth in price terms in 2007, we chose mid-2007 as our starting point.

The 2007 to 2020 window covers the entire low rate period. By measuring from the pre-GFC economic/market peak to the pre-COVID-19 economic/market peak, we have bracketed the secular stagnation era in an unbiased way. And by measuring over a period of around 12 years, we should arrive at statistically meaningful data and conclusions concerning trends.

To make the conclusions as up-to-date and relevant as possible, we show the numbers to March 2020. To the extent that analysts were already downgrading numbers for COVID-19 and that the value portfolios may be more cyclical, this is a bias against value, so we err on the side of caution here.

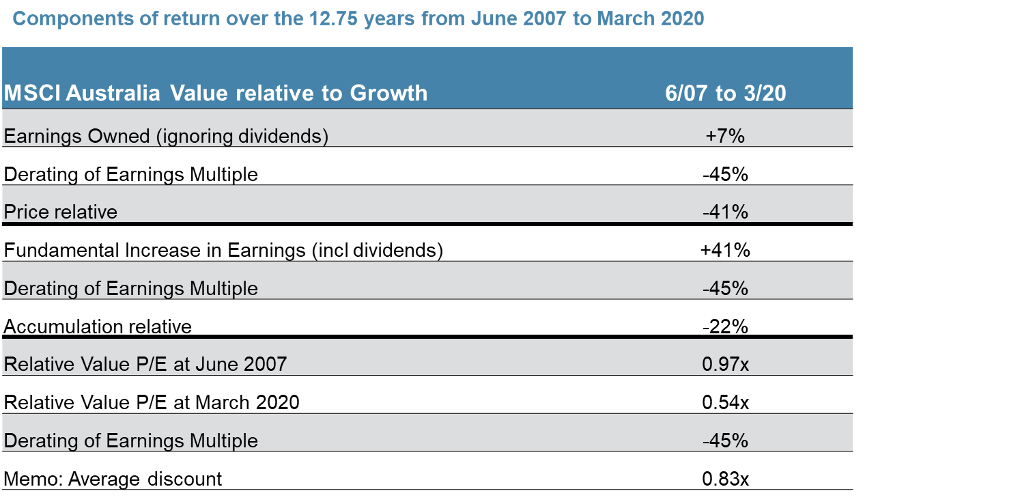

So what happened over this period? The table below answers this question - all data is MSCI Value relative to MSCI Growth.

Table 1: Summary of the components of return over the 12.75 years from June 2007 to March 2020. Percentages have been rounded. Source: FactSet, MSCI, LAMP calculations.

The data shows that over this period, the value portfolio grew its forward earnings by 7% more than the growth portfolio. But due to a 45% relative de-rating, the price return has lagged growth by a dramatic 41%. Once we include the higher dividend yield of the value index, we find that by the end of this secular stagnation era, the value portfolio has entitled the investor to 41% more earnings than the growth portfolio.

This is the reverse of the narrative that is driving markets.

However, due to the 45% relative de-rating of the value portfolio (which was mostly growth stock multiple inflation, rather than an absolute derating of value stocks), the value portfolio ended behind by 22% on an accumulation basis. Much more than 100% of the performance lag for value has been sentiment/multiples. It is worth emphasising this remarkable arithmetic:

(1 + 41%) (1 – 45%) = (1 – 22%)

(41% more fundamentals) (45% lower relative multiple) = (22% relative underperformance)

Imagine that you’d invested with a value manager in mid-2007. That manager promised you that their stock selection could produce more than 2.5% outperformance of fundamentals per annum. In April this year, after 12 years of delivering 2.7% pa on the fundamentals, the manager is 22% behind the overall market. What is your conclusion, given that you see headline returns but do not place a weight on fundamental returns?

The key question remains: what’s a more sustainable way to greater wealth - owning more earnings; or stocks that trade on higher and higher multiples?

As in late 1999, individual investors and funds currently basing their decisions solely on headline numbers are contributing to the rapidly widening gap in stock pricing by deserting value strategies and portfolios.

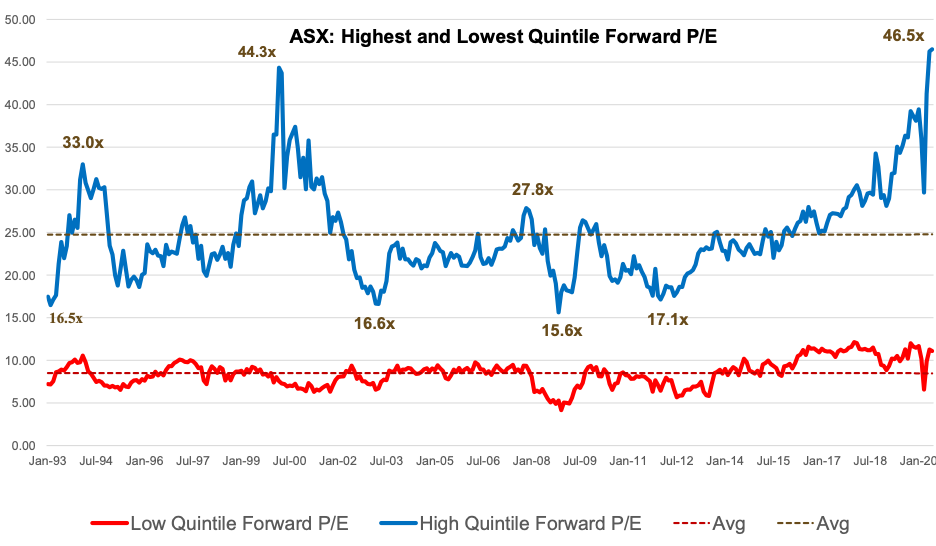

As in the late 1990s, Australia was relatively late to join the current tech boom in the US, then, once we joined we did so with gusto (our InfoTech index trades on more than double the S&P500 equivalent in the US). We have seen this sort of growth stock P/E inflation before, and it didn’t end well in the past.

The chart places the current multiple divergence across the ASX into context.

Source: CSFB to June 2020

Source: CSFB to June 2020At more than 46-times forward earnings, how comfortable are you paying ever-higher P/Es for growth stocks?

Never miss an insight

Stay up to date with all my latest Livewire content by clicking the follow button.

MSCI use a two dimensional definition of growth and value. Value is defined by low P/B, low P/E and high dividend yield, while growth is classified according to five measures of firm growth rate. This means that growth is not simply anti-value defined by high multiples. More information can be found here: https://www.msci.com/eqb/methodology/meth_docs/MSCI_Dec07_GIMIVGMethod.pdf.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Philipp Hofflin is a Portfolio Manager/Analyst on the Australian Equity Team with Lazard Asset Management Pacific Co. He began working in the investment field in 1995. Prior to joining Lazard in 1999, Philipp was the Head of Financial Markets Research with Royal & Sun Alliance in Australia, (previously Tyndall Investment Management) and a tutor/lecturer for the School of Mathematics and Statistics at the University of Sydney. Philipp has a BSc (Hons) from The University of Melbourne, a Graduate Diploma in Economics and a PhD from the University of Sydney. Philipp specializes in interest rate sensitive companies and is fluent in German.

1 topic

Philipp Hofflin is a Portfolio Manager/Analyst on the Australian Equity Team with Lazard Asset Management Pacific Co. He began working in the investment field in 1995. Prior to joining Lazard in 1999, Philipp was the Head of Financial Markets...

Expertise

Philipp Hofflin is a Portfolio Manager/Analyst on the Australian Equity Team with Lazard Asset Management Pacific Co. He began working in the investment field in 1995. Prior to joining Lazard in 1999, Philipp was the Head of Financial Markets...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Investment Theme

When dumb money beats smart money, it’s time to worry

Livewire Markets