New year, new strategy?

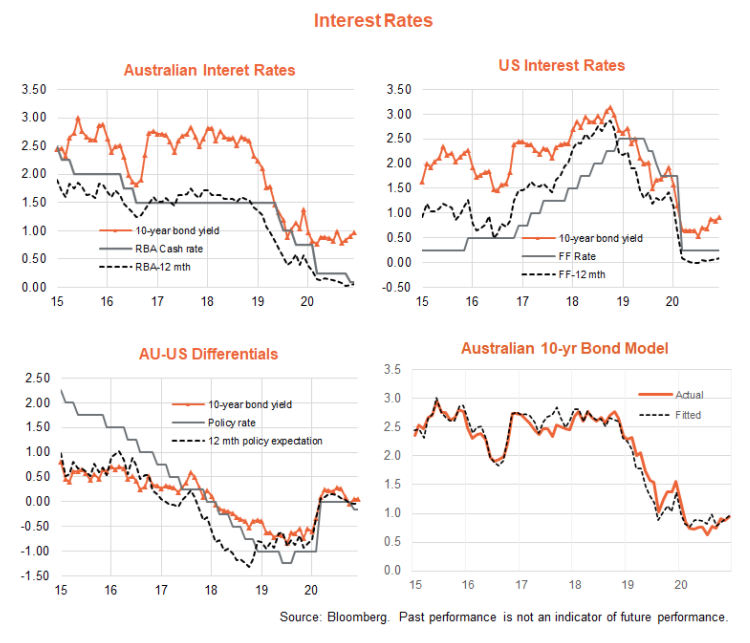

Long-term bond yields continued to creep gradually higher in December as the prospect of further significant near-term monetary stimulus eased in line with an improving global economic outlook. US 10-year government bond yields ended the month at 0.92%, and Australian 10-year rates at 0.97% – implying a small positive spread for local rates of 0.05%. This compared with a daily low for US 10-year yields of 0.5% on August 4, and 0.62% for local yields on 9 March. US rates have lifted modestly more than local rates in recent months, with the bond spread contracting from a month-end peak of 0.29% at end-July.

Based on current cash rates and 12-month forward policy expectations in Australia and the U.S. (essentially no expected change in rates), my Australian 10-year model suggests fair-value around the current rate of 1%, i.e. bonds are fairly priced given current market expectations. Accordingly, if we end 2021 with no policy change and the market essentially expecting no policy change over 2022 either, bonds yields need not rise much further from where they currently are.

My base case expectation remains for a fairly benign interest rate outlook this year, with continued broad policy alignment between Australia and the US. Specifically, I expect no policy change in either Australia or the US this year, though by year-end I expect the market will be pricing one 0.25% tightening in both countries for 2022 – such that local and US 10-year bonds end the year around 1.25%. Of course, there are both upside and downside risks to this outlook – but the main message is that modelling suggests bond yields are at present not that unusually low given current monetary settings, and so should stay fairly low if monetary setting don’t change all that much.

Australian dollar – firm for now but should ease

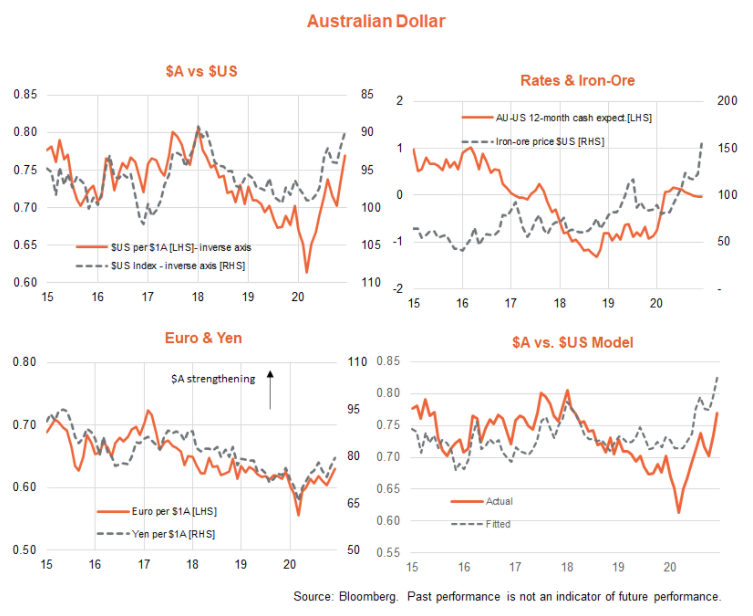

The Australian dollar continued to power higher over December, ending the year at US76.9c, compared with a recent end-month low of US61.3c at end-March. Although the RBA has tried valiantly to hold down the $A through further local monetary easing, the reduction in Australian-US short-term interest rate differentials has only been modest whilst important drivers – such as broad based weakness in the $US and surging iron-ore prices have provided offsets.

Indeed, based on historic relationships since 2005 between the $A, interest rate differentials, the $US and iron-ore prices, my valuation model suggested the $A could have gone as high as US83c! This alone suggests the $A could push even higher in the short-run, even if underlying fundamentals don’t change all that much (although I note iron-price prices in the early days of the new year have dropped back to US$133/tonne, placing fair-value at US81c).

Where to for the $A? Interest rates are likely to remain a neutral influence, given broad monetary alignment between Australia and the U.S. Iron-ore prices, however, should ease over the coming year as China eases back on stimulus and Brazilian supply continues to gradually recover. Indeed, last month’s mid-year Federal Government budget update projected a fall in iron-ore prices to US$55/tonne by September (compared with the year-end level of US$155!) – which would be consistent with a fair value for the $A (assuming all else constant) of around US75c.

That leaves the outlook for the $US. Weakness over the past year at first reflected an unwinding of the initial COVID-related flight to $US safety, but the $US has fallen to well below pre-COVID levels in more recent months. This added weakness appears to reflect a view that non-U.S. ‘value’ parts of the global equity market may continue to outperform with global recovery, and also risks related to the U.S. economy due to both election uncertainty and its ongoing COVID problem.

My expectation, however, is that the $US should stabilise in coming months and regain some strength as America recovers from the COVID shock and U.S. dominant technology/growth stocks reassert their relative strength.

On the view that the $US strengthens by 5% by end-2021 and iron-ore prices fall to US$75/tonne, my year-end $A fair-value estimate would be around US74c.

Equity prices – earnings-driven recovery

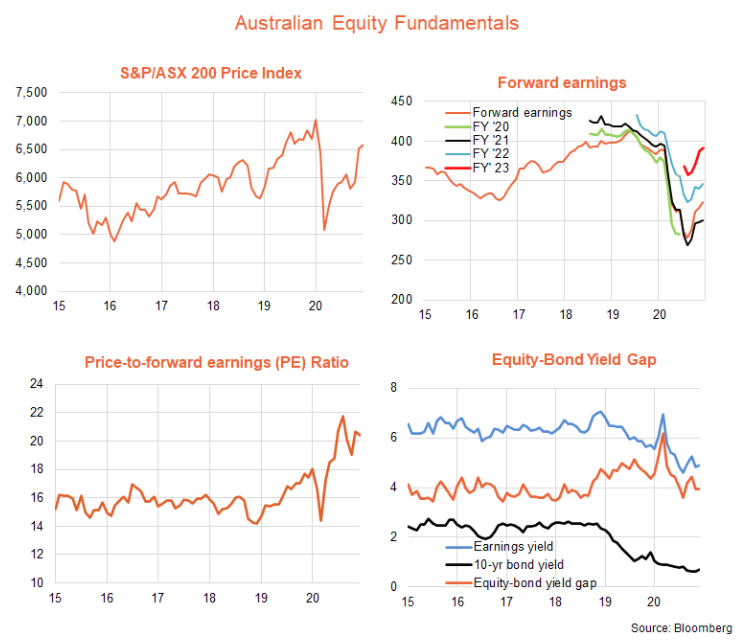

After a mid-year pause, the recovery in Australian equities from the February/March slump resumed over the final months of 2020. The S&P/ASX 200 Index returned a further 1.2% in December after a strong 10.2% return in November. All up, the market returned 1.4% last year, with a 31.9% rebound from the monthly end-March low just offsetting the 23.1% slump over the first three months. The S&P/ASX 200 price index, however, did drop 1.5% over the year, with a 3% dividend return (which itself was down on historic returns of around 4 to 5%) keeping the total return in positive territory.

As seen in the chart below, one heartening aspect of recent share market performance is that it has reflected a rebound in earnings (or more specifically earnings expectations) rather than further escalation in already lofty price-to-earnings valuations. One a month-end basis, the price-to-forward earnings ratio peaked at 21.8 at end-August, though ended the year at 20.4. With the 10-year government bond yield around 1%, that implies an equity earnings-yield (inverse of the PE ratio) to bond-yield gap of around 4%, which remains broadly in line with average levels over the past decade or so.

Where to for equities? Assuming a modest lift in bond yields, PE valuations could be a modest drag on returns – indeed, if 10-year bond yields hit 1.25% by year-end and the equity-bond yield gap holds at around 4%, the PE ratio would decline to around 19 – implying a 5% decline. Meanwhile, current earnings expectations imply 14% growth in forward earnings over the coming year, which if realised could still produce a net price return of around 5 to 10%, or total return of 9 to 14% including a modestly improved dividend return of around 4%.

All this is consistent with a base case year-end S&P/ASX 200 target of around 7,000.

Equity trends – US/growth vs non-US/value?

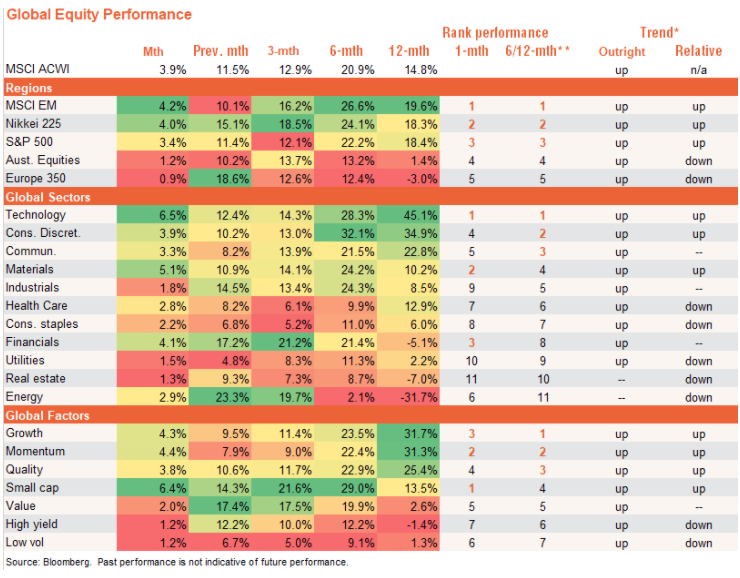

As evident in the table below, along with the maturing of the global equity rebound from the March lows of last year, long-unloved value and non-US regions have attempted to outmuscle U.S./growth/technology themes in recent months. Over the last three months of 2020, Japan and emerging markets performed best among regions, financials and energy shone among global sectors, with small caps and value faring best among factors. Japan and EM continued to do well in December, though technology performed strongly among sectors while value slipped back among factors. On a currency-hedged basis, relative Australian performance has been mixed, though much stronger than unhedged global equities due to strength in the $A.

Tables ordered by 6/12 month return performance for each region, sector and factor respectively – on a local currency basis. Past performance is not indicative of future performance. You cannot invest directly in an index.

Whether this attempted rotation away from the winning US/tech/growth themes of recent years persists remains to be seen. A lift in oil prices and bond yields as the global economy recovers should favour value sectors such as energy and financials respectively. But technology also retains strong structural tailwinds and still-reasonable overall valuations given promised solid earnings growth.

Overall, I remain dubious whether we’re really seeing a sustained rotation, or merely an unwind of the premium growth sectors attracted in the early dark days of the COVID sell-off.

Never miss an insight

Hit the follow button below to stay up to date with my insights on the macro events shaping the ETF landscape.

To learn more about BetaShares Funds, please visit our website.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

10 stocks mentioned

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment