No guidebook for this crisis

With over 40 years of experience in financial markets, Paul Xiradis from Ausbil Investment Management has seen more than his fair share of market collapses, from the '87 Crash through to the GFC. But none of them looked quite like this one. Prior collapses have been driven by either fundamental or systemic issues, but this one has been driven by an entirely different menace; a deadly disease.

In this wire, Paul addresses our questions about his outlook for economies and markets from here, how stimulus and rescue packages could affect this outlook, and how he's positioned now.

Why is this correction different to the others you've faced in your career?

Significant market corrections are typically brought on by fundamental factors such as a slowing economic cycle or interest rates rising to a point where they start to choke off corporate earnings. Sometimes there are systemic issues which create hidden risks and, once the risks become more apparent, valuations suffer. We saw this with the Long Term Capital Management Hedge Fund crisis in 1998, and again with the Global Financial Crisis in 2008.

The long history of fundamental corrections means that, although they’re unfortunate, and there are both winners and losers, they offer us a guide as to how to manage and mitigate the risks.

This event is different (there’s no ‘guide book’), in that it wasn’t instigated by fundamentals. Rather, it was brought on by a contagious and virulent disease that has rapidly spread around the world. We have seen epidemics and pandemics previously but this one has proved extremely difficult to contain. The resultant shutdown has upset consumer behaviour and spending patterns. It has also disrupted the working environment and work practices. We haven’t seen this before at this universal scale.

Equity market valuations have adjusted rapidly to the new environment and they’re down around 30%. The risk now is the extent to which this feeds through into the broader economy, and into future company earnings.

What's your outlook for global economies? Is a recession imminent?

Well there is no doubt that it will be a difficult period.

Lockdowns have been implemented across a whole range of jurisdictions and industrial production has moved back to levels not seen since the GFC in 2008 and 2009.

The virus originated in China and they will experience a poor first quarter. More recently, they have had some success in controlling the spread of the disease, with reports that major industrial enterprises have resumed work.

The G20 will experience a very weak second quarter. Certain service sectors such as travel, hospitality and retail have either ground to a halt or have been severely disrupted, so this must have a cost. Many workers have already been laid off or stood down. For example, here in Australia, Qantas stood down 20,000 staff. It’s important to note that a majority of people who have been laid off are expected to return to the workforce, at this stage, when the virus has been suppressed.

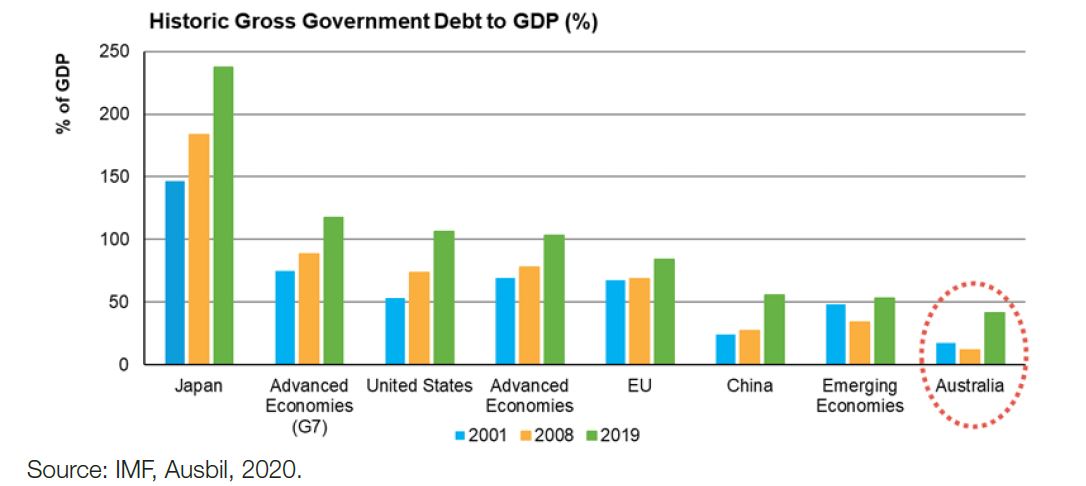

Will the globe experience a technical recession? The answer may vary across jurisdictions depending on the level of stimulus. Countries like the USA and Australia have so far responded with policy measures that amount to some 22% and 17% of GDP, respectively. These levels are unprecedented. But activity will gap down sharply during the next months, unemployment will rise and growth rates will stall. It will feel like a recession.

What effect will the government's stimulus and rescue packages have on the local economy?

A$320bn in monetary and fiscal measures have been announced, designed to support individuals, households and businesses, and ensure the flow of credit. This is huge and without recent precedent.

The Job Keeper wage subsidy is particularly interesting and amounts to $130bn of the stimulus package. The unemployment rate will temporarily surge higher on shutdowns but it will be tempered by this initiative. It means that employers can preserve their workforce during an extremely difficult period and quickly resume activity as the recovery takes hold.

On the monetary side, the Reserve Bank is deploying ‘yield curve control’, and we’d expect the official interest rate to remain at 0.25%, or less, for the next 3 years. So, interest rates and inflationary expectations will remain low. This should support activity and extend the equity cycle as it recovers.

It’s also worth noting that China stimulus will boost their infrastructure and construction activity. Steel inventories have been depleted and demand for bulk commodities has been resilient. You can see this in bulk prices with iron ore at around $82 per tonne and metallurgical coal at around $145 per tonne. This is a supportive for our terms of trade and national income.

The AUD/USD is set to benefit from both this effect and the global stimulus.

Overall, we expect a very, very tough period during the next few months. Our base case is that we expect recovery later in 2020 and into 2021.

Figure 1: Australia better positioned than most to fund its stimulus package

From a portfolio construction perspective, how are you managing this crisis?

While earnings are always important, immediate balance sheet strength has become a priority across the market, so we have been doing a lot of stress testing.

Any signs of balance sheet weakness, or an industry structure that is challenged, may provide a reason to decrease exposure or sell. We have seen this in parts of the building and mining services sectors.

We have a quality bias including a solid position in biotechnology and healthcare. At the same time, we are ensuring some defensive characteristics via supermarkets, telecommunications and selected real estate investment trusts.

We are a little overweight the banks because they went into this crisis with real financial strength and they are working with the government to support business and consumer activity. Unlike in 2008, they are part of the solution, not part of the problem.

We own bulk commodities too, given that there is improvement in China and more stimulus on its way.

Contrary to the negative sentiment in the market, some companies offer both resilience and clear growth prospects in and beyond this crisis. We are seeing such opportunities in the online and technology space, and we are exploring these in depth.

So, as you’d expect, it’s a balanced, diversified approach that acknowledges the challenges ahead of us over the coming months, but also maintains exposure to the best companies so that we can participate in the full recovery cycle when it starts.

We think it’s important not to become too defensive right now.

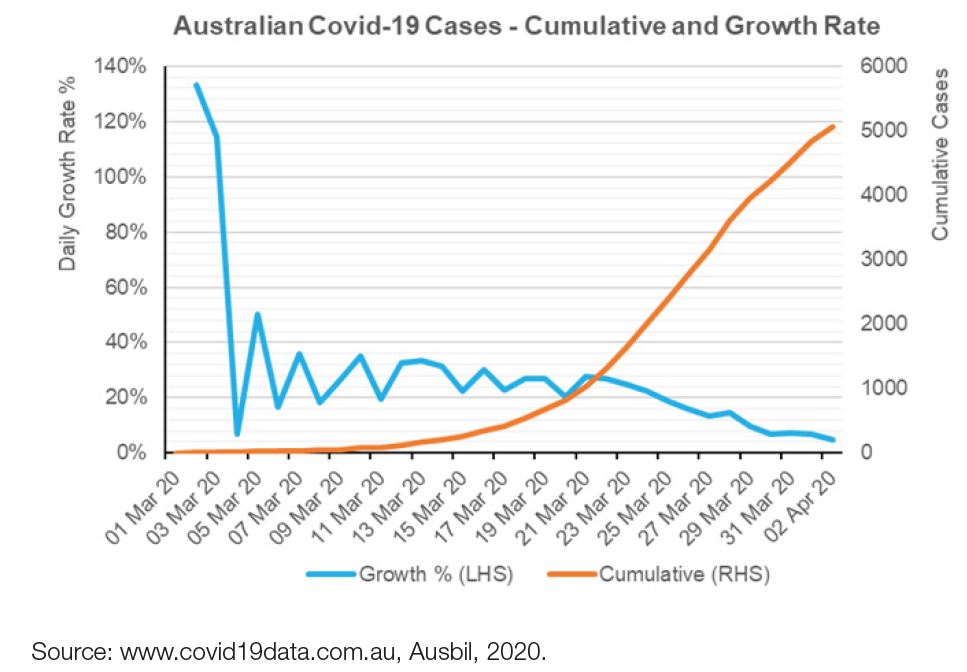

Australian governments and the health authorities are, on balance, managing the crisis effectively and there is some slowing in the rate of the spread of the disease (see chart below). There is potential for the shutdown to ease more quickly than in other parts of the world.

Figure 2: The spread of Covid-19 in Australia is showing signs of slowing

Invest with Experience

Ausbil's investment approach allows them to exploit the inefficiencies across the entire market, at all stages of the cycle and across all market conditions. Find out more here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

2 contributors mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets