Our single largest Chinese investment

Charlie Aitken

Aitken Investment Management

Our structurally bullish view on Chinese consumer-facing companies continues and today we thought we’d update you on our single largest investment in China, Ping An Insurance (2318HK). Ping An has been in the fund since our inception 2.5 years ago. As our conviction has grown so too has the scale of our investment in Ping An, which now represents just under 10% of the fund. Ping An is a Chinese insurance company listed in Hong Kong leveraged to numerous structural growth themes and is a significant regulatory reform beneficiary. Ping An announced a very solid FY17 result last week and we continue to see a strong path of growth ahead for the company.

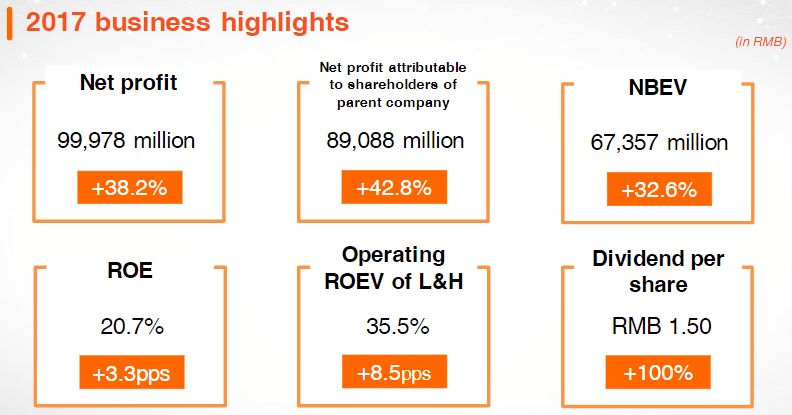

The results again highlighted Ping An’s best in class insurance status. NPAT was 5-10% ahead of market expectations with traditional insurance (life and P&C) and internet segments (or Ping An’s fintech investments) all beating consensus comfortably. The RMB 89bn reported earnings were up 43% on FY16 (RMB 76.2bn was consensus), and life NBV (net book value) growth of 33% was very strong. Investment income also climbed 12%, new business value increased 33%, and the net premium earned increased 34%.

A key positive surprise was the increase in dividend. The company quoted that the “Board of Directors suggested raising the cash dividend ratio to 30.8%, which drives the dividend per share for 2017 up by 100.0% year on year to RMB 1.50”. This is an increase from 21% to 30.8% in the payout ratio and highlights the confidence in the company’s prospects and performance. The positive 10.9bn RMB surprise from the ‘Ping An Doctor’ restructuring should also be noted. Ping An Doctor has been accepted by the Hong Kong stock exchange for an IPO (expected to come to market late April).

The result also showed Ping An’s commitment to their technology offering. Lufax (Ping An’s online lending platform) became profitable for the first time this year following 97% growth in loans under management. Ping An now has 436 million internet users, around 10% of the total internet users globally, with 100% growth in the last 2 years, and 200% in the last 3 years. The technology offering currently includes online banking platforms and facial recognition systems that include the ability to detect if borrowers are lying (might be useful for mortgage brokers in Australia!!). The benefits of such investments are starting to show through in the results, with the RoE of their Fintech and HealthTech business (41%) already achieving 2X the ROE of the group as a whole.

We continue to believe there are numerous structural tailwinds for Ping An including:

- Transition to a consumption-driven economy

- An aging population – increased demand for healthcare and pension resources

- Continued reform of a relatively poor healthcare system

- Extremely high savings rate – greater than 50% of GDP

- Population underinsured – life insurance penetration 1.8% versus 3.8% globally

- Financial reform

- Rising middle class – greater awareness and focus on healthcare, retirement benefits, estate planning and ability to afford wider range of insurance.

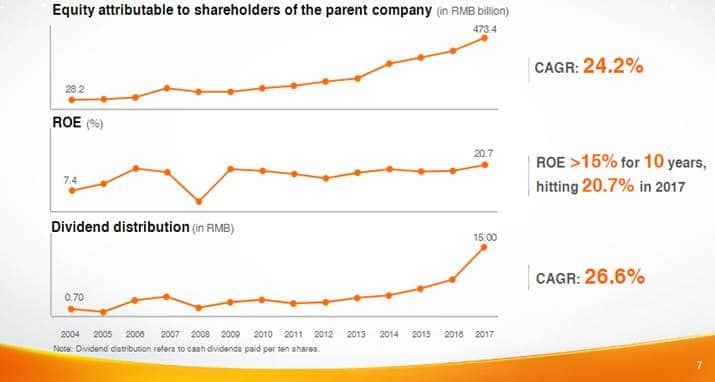

The following slides released with the results highlight the impressive track record of Ping An over the last 14 years.

We continue to believe we can find strong growth prospects in Asia, with structural tailwinds and at reasonable valuations.

Aitken Investment Management is a Global High Conviction Fund. For more information please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire