Outlook 2021: Searching for some sort of normal

As 2020 draws to a close, transition in the White House is underway and vaccine discoveries are lowering the likelihood of another damaging lockdown. Policymakers also look intent on sustaining historic stimulus, with interest rates pegged at zero for several years. While growth could fade and market volatility rise into the end of the year, we are choosing to edge more overweight equities for 2021. Our moderate economic recovery outlook supports equity overweights to Australia, Europe and emerging markets.

2020—saying goodbye…but etched on our memories

2020 has been a challenging year for investors. Markets have had to absorb a one-in-a-hundred-year pandemic, a global recession, a turbulent US election and quickening climate events. February and March witnessed one of the sharpest equity market corrections (and bond market rallies) in history. Since then, risk appetite and equity indexes have broadly recovered over the remainder of the year (and balanced portfolios have preserved capital, despite a 35% equity collapse in March). This has been aided by similarly historic monetary and fiscal stimulus, efforts to contain the virus that proved successful initially, as well as recent late-year progress on a vaccine.

Without doubt, this has been a year that has heralded the benefits of investing across an appropriately diversified core of quality assets, including traditional equities, bond and credit markets—as well as alternative assets, such as private equity, hedge funds, real assets and private credit. Moreover, in a year where crises have embodied a confronting human element, it has also highlighted the need to remain disciplined in the asset allocation process and avoid emotional decisions, which might include shifting portfolios to cash. As discussed here, this brings its own challenges.

2021—still on track for a moderate U-shaped recovery

Even as 2020 draws to a close, short-term uncertainty remains over the likely path of future activity. The coming months will be dominated by key risks. Firstly, the rapid resurgence of the COVID-19 pandemic across the US and Europe; and secondly, uncertainty over a complicated transition of US leadership. There are already some signs of a loss of Q4 growth momentum across the US and Europe, raising concern that 2020’s historic level of monetary and fiscal stimulus may not be sufficient to sustain growth through 2021. Then, there is the uncertainty of what decisions on trade and defence may flow from the White House before the January 2021 inauguration. But beyond the next few of months, several drivers suggest our long-held moderate (albeit stop/start) global and domestic recovery remains on track:

- Historic near-zero interest rates and elevated liquidity. The US Federal Reserve (Fed) and Reserve Bank of Australia (RBA) are flagging zero rates until 2023. Further stimulus is widely anticipated from the European Central Bank (ECB) and Fed before the end of the year.

- Sustained government support, with stimulus via employment support and tax cuts worth more than 5% of global output in 2020 (several times larger than during the 2008-09 GFC). While the stimulus impulse is fading, the US is expected to deliver a further package in Q1 2021.

- Elevated household saving rates, reflecting the combination of government payments and reduced consumption. Combined with rising consumer confidence and easing virus fears, this should be a powerful force underpinning a pick-up in consumer spending through 2021

“From a huge river of uncertainty, we see the other side now… …but I don’t want to be exuberant about this vaccination because there is still uncertainty.” - Christine Lagarde, President of the European Central Bank - November 2020

These combine with news of a number of vaccine discoveries, which should

reinforce governments’ reluctance to return entire economies to damaging

lockdowns. The recent stabilisation in the US, European and Australian company

earnings trends also flags stronger underlying activity in 2021. The potential for

President-elect Biden to outwork the US’ bipartisan anti-China sentiment in a

more diplomatic way should also foster a calmer geopolitical environment.

As such, we add some risk to our portfolios as we enter 2021, with two key decisions. Firstly, we move a little more underweight fixed income by closing our overweight to international corporate credit, where spreads have now tightened to pre-COVID-19 levels. Secondly, for equities, we move modestly more overweight. While we leave our underweight to the US in place, we move overweight Europe, joining our Australia and emerging market overweights, all regions likely to benefit from a recovery in 2021 growth.

“Globally, households have considerable levels of excess savings from the pandemic…those numbers are around 7.5% to 10% of global output, which amounts to considerable levels of potential spending/economic stimulus” - Longview Economics November 2020

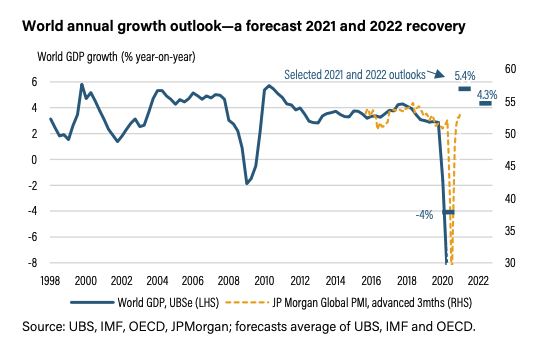

What do the key global forecasts look like?

Forecasts for global growth have been edging higher. In October, forecasts from the International Monetary Fund (IMF) were less dire than its mid-year figures, with growth seen rebounding by 5.2% in 2021 (after -4.4%). UBS, in November, significantly lifted its 2021 outlook, shifting to its ‘optimistic vaccine scenario’, which assumes a visible decline in virus cases by mid-2021, faster than its prior H2 2021 assumption. It now forecasts global growth of 6.1% in 2021 and 5.0% in 2022 (compared with 5.3% and 4.1% previously).

As shown in the chart above, 2021 growth of around 5% would be the fastest

pace since the post-GFC rebound. Still, activity is likely to remain below preCOVID levels until late 2021. Even so, a synchronised recovery should underpin a

weaker US dollar, some drift higher in inflation (though to levels that are still

below central bank targets), as well as a modest rise in bond yields (on the back

of improving growth and inflation trends).

What are the risks to an improving growth outlook?

After 2020, there should be no doubt that forecasts are (and always were) subject to significant ambiguity. Balancing that, with monetary and fiscal policy on ‘full tilt’, a deep recession in the immediate rear-view mirror, the shift in US leadership, and several vaccines reporting over 90% success rates, it’s not surprising that the list of risks to the macro outlook is worryingly short. Indeed, risks to the macro backdrop appear less substantive than those confronting arguably expensive asset prices:

- Delayed vaccine approval until late 2021 would raise the risk of renewed lockdowns, declining consumer confidence, combined with the stretched ability of policymakers to materially add additional stimulus. A much higher level of bankruptcy and unemployment would dominate.

- A surprise burst of inflation likely due to short-term supply pressures. This may not be sustained given the extent to which global demand is depressed and jobs markets are weak. However, if bond yields were to rise, it could undermine the current highly liquid environment.

- Consumers prove highly cautious despite a vaccine, leading to a much slower pick-up in activity and repair of jobs markets. Here, the risk is that policy stimulus may not be sufficient to bridge the gap to a fuller recovery, threatening a double-dip recession.

Outlook for fixed income

For much of 2021, we expect central banks to remain hostage to virus risks, with the Fed, ECB and Bank of England (BoE) all flagging extensions of their stimulus packages. But with a vaccine in sight and better economic indicators pointing to recovery, uber-accommodative quantitative easing (QE) and other liquidity measures may come under pressure as we move through H2 2021.

We expect global monetary policies to remain accommodative with overnight cash rates close to zero for all of 2021. The RBA is expected to remain at 0.10%, keeping the front end of the bond curve well-anchored. However, despite the RBA’s historic $100 billion bond buy-back program to control the yield curve, the Government’s implementation of larger fiscal measures and increasing supply of both state and government bonds, we will likely see yield curves steepen with longer-dated rates rising modestly through the year.

Investment-grade and high-yield credit have recovered strongly in 2020 and will enter 2021 at pre-COVID spreads, where we expect them to stay while stimulus is in place. Signs of any reduced QE will inevitably see bond yields lift and credit spreads widen. We, therefore, favour keeping duration low by investing in floating rate products (targeting robust Australian banks), private debt managed by best-in-class managers, and investment-grade credit, while taking profit on high-yield fixed-rate bonds. Bank capital levels remain robust, suggesting investors will do well to own additional Tier 1 hybrids for yield.

Outlook for the Australian dollar

The US dollar is typically a defensive currency, attracting capital when rising global uncertainty drives demand for US treasuries. Consistent with that, synchronised global recoveries typically see the US dollar engage a flat-to-weaker trend, an outlook that also aligns with a Biden-relative-to-Trump presidency. Reflecting that, most outlooks now centre on stronger non-US exchange rates through 2021. The Australian dollar, along with the euro and emerging market currencies, are seen as key beneficiaries.

As we discussed last month in our Core Offerings Australia 2021—positioned for outperformance, our relatively more upbeat macro outlook for Australia should support a trend rise in the Aussie dollar, despite its vulnerability to risk-off events. For end-2021, UBS forecasts a rise in the currency to USD 0.77, while CBA predicts USD 0.78, gains of 6-7% from current levels. Gains against non-US dollar currencies are seen as less significant.

Outlook for alternative investments

Overall, the medium-term opportunity set for alternatives has improved in the wake of the global pandemic. However, we continue to stress the importance of diversification and investing through leading specialists in their respective fields. There remains much uncertainty, which warrants close attention given more nuanced sector-specific impacts of the pandemic. We see three key themes to watch in 2021:

1. Dislocation and distress—While extensive actions by central banks have minimised some of the opportunities since Q1 2020, we believe that further dislocations remain across both equity and credit markets, providing a favourable environment for nimble hedge fund strategies and providers of structured liquidity. In addition, we anticipate that the distressed debt cycle could still rival the scale of that seen in the aftermath of 2008.

2. Alternative credit and stable yield assets—With the likelihood of near-zero rates for multiple years, institutional investors from pension funds to major insurance companies are looking to both alternative credit (such as unlisted private debt) and global real assets (like property and infrastructure) for defensive yield. We believe this heightened demand will drive strong performance in this space. Data and renewable assets with long-term contract terms look particularly attractive.

3. Future of growth—Notwithstanding that COVID-19 has accelerated many underlying technological trends, all companies will need to become tech-enabled and innovate. As such, venture and growth capital are poised to take advantage of this, and we expect this will drive value creation for years to come. There is also a structural shift toward companies staying private for longer (the average is now approximately 11 years), making it harder to access this value creation without investing in private markets.

Outlook for equities

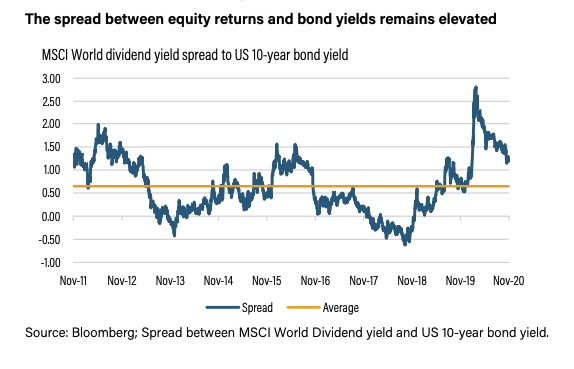

Globally, equity strategists are forecasting a double-digit return for equities by end-2021, with Credit Suisse targeting a 15% rise. While the recent rally now sees tactical indicators arguing for a pause, the fundamental supports for further equity gains in 2021 are stimulatory policy, the risk-adjusted return pick-up of equities over bonds, and the beginning of a bond-for-equity switch, with bonds now arguably offering less diversification.

The biggest decision for investors for 2021 may well be the style inherent in their portfolios. The prospect of a widely available vaccine would suggest a more synchronous global recovery, which lends itself to more economically-sensitive exposures, rather than the bulwarks of current portfolios, which are structural growth and defensive allocations to IT and healthcare. Regionally, this would suggest incremental allocations to Europe and the emerging markets at the expense of the US. The UK remains beholden to Brexit uncertainty, but if that is resolved, it would also offer upside.

Domestically, the backdrop for equities remains positive. Significant and co-ordinated fiscal and monetary stimulus stands in contrast to recent events in both the US and Europe. We would also argue the RBA’s additional $100 billion in QE has not received the attention it deserves, notwithstanding it looks small compared to the USD 3 trillion added by the Fed. If the entire term funding facility was drawn, the RBA’s balance sheet will rise to around 25% of national output, quickly catching up to the same level as the Fed’s (34%).

This sets a positive backdrop for domestic equity returns from an already relatively cheaper valuation position vis-à-vis the rest of the world. With banks receiving cost of funds assistance, with bad debts manageable and significant capital buffers, the sector looks well supported. With the prospects of a global recovery underpinning the materials sector, and a healthcare sector that has been less defensive than usual (due to COVID-19), 60% of the domestic market now looks leveraged to stronger post-COVID conditions.

Where are the risks? Although the outlook for 2021 looks constructive, it’s important for investors to have an eye on potential risks. Fiscal gridlock in the US against a backdrop of more widespread COVID-related lockdowns and mobility restrictions make for a more difficult short-term trajectory. Any delays to the widespread rollout of a vaccine could heighten vulnerability to a pull-back, though we suggest the market will be tempted to look beyond this.

Equity investors would also be well advised to watch the direction of credit spreads—credit spreads and equity returns can, at times, be closely correlated. Additionally, the 40 basis points (bps) rise in bond yields in the lead up to the US presidential election was enough to check momentum in global equities, with significant rotation away from IT and healthcare. Although central banks will be reluctant to let bond yields rise too much or too quickly, we are mindful that US 10-year yields began 2020 closer to 2% than 1%, and significant moves higher would prove a headwind for equity performance.

Learn what Crestone can do for your portfolio

With access to an unrivalled network of strategic partners and specialist investment managers, Crestone Wealth Management offer one of the most comprehensive and global product and service offerings in Australian wealth management. Click 'contact' below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment