Overweight banks in October, the winning trade

Since 2000, the Bank Index has been up 12 out of the last 16 years or 75% of the time. In the 12 years that the Bank Average has closed up, the average rise in those 12 years has been MASSIVE - 5.95%, so this is significant. I believe the reason is that investors chase the banks for their dividends – since hardly any other stocks are going ex-dividend in early November – they tend to see huge buying interest.

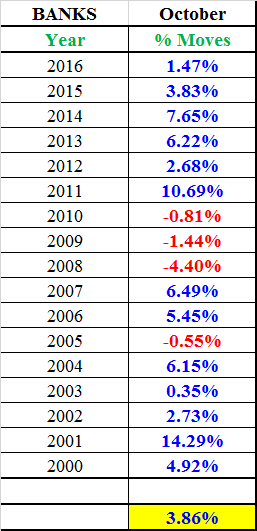

Performance of ASX 200 Bank Index over the last 17 years

Source: Coppo report

The average rise has been +3.86%

Source: Coppo report

Why are the Banks so strong in October?

One reason I think has to do with the fact that the 3 big Banks (not CBA) all report in late October or early November, as a result, investors buy them ahead of reporting. Over the last 20 odd years I have seen it happen again and again – most years it happens. The only exceptions come when there is a big “global macro” event that is causing markets to be hit across the globe.

With the September reporting season now over and all stocks from then have already gone ex-dividend and most are in the process right now of “paying” the dividend into investors accounts.

Many investors, in their desperate “hunt for income” look to where they can next “harvest” income. There are some funds that follow the dividends around and provide big distributions and these funds I know will be buying the banks for their income.

What we see is a ‘rotation” out of the stocks that have already paid dividends into the next ones that do. Now the Bank dividends are some of the biggest in the market. For instance, we saw in September $16.4 billion in dividends was paid and another $7.3 billion in October. In total, over those 2 months, we have $23.7 billion being paid.

With the 3 big banks have dividends coming up and based on dividend estimates we see each bank paying:

- NAB $2.66 billion (based of dividend of 99c fully franked)

- ANZ $2.37 billion (based of dividend of 81c fully franked)

- Westpac $3.2 billion (based of dividend of 94c fully franked)

Just 3 stocks will pay $8.2 billion, versus 378 stocks paying $23.7 billion right now.

With the “45 Day rule” this means that retail investors must continuously hold shares 'at risk' for at least 45 days to be eligible for the franking tax offset. Given the 3 big banks report in late October / early November, this time frame is relevant:

- Thursday 12th October - BOQ

- Thursday 26th October - ANZ

- Thursday 2nd November - NAB

- Monday 6th November - WBC

Their approximate ex-dividend dates, based on when they went ex-dividend last year, are roughly around these dates

- 6th November - ANZ

- 6th November - NAB

- 14th November - WBC

So, there will be investors who will, from now, buying the banks to secure another major income stream

I have seen quant studies done over the years that prove this, whereby the banks “outperform” in the 4 weeks prior and 2 weeks post – going ex-dividend (I have been quoting this number for 15 years and it seems to occur most times)

it will happen again this year – the only thing that would kill a banks rally is a global selloff (which many have been calling for since November last year after Trump was elected).

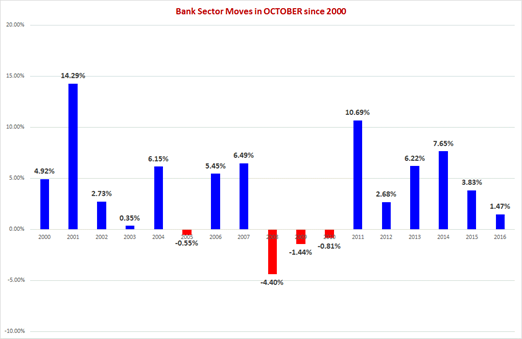

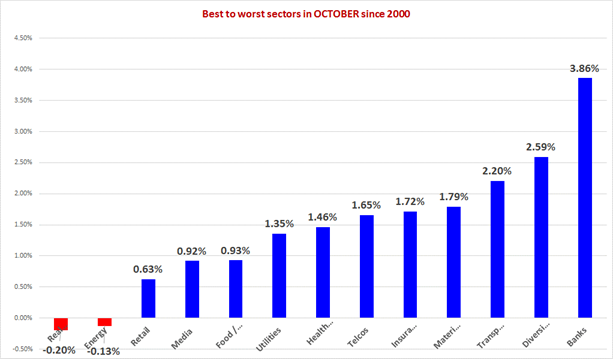

Banks have been the best sector in October over the last 17 years; up +3.86%

Source: Coppo report

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Richard authors “The Coppo Report”, a highly regarded market newsletter. He has over 30 years’ experience in financial markets, beginning his career at Ord Minnett where he worked for 15 years, before moving to Goldman Sachs.

1 topic

4 stocks mentioned

Richard authors “The Coppo Report”, a highly regarded market newsletter. He has over 30 years’ experience in financial markets, beginning his career at Ord Minnett where he worked for 15 years, before moving to Goldman Sachs.

Expertise

Richard authors “The Coppo Report”, a highly regarded market newsletter. He has over 30 years’ experience in financial markets, beginning his career at Ord Minnett where he worked for 15 years, before moving to Goldman Sachs.

Expertise

Comments

Comments

Sign In or Join Free to comment