Quality vs value in Australian small caps

UBS Asset Management

UBS Asset Management

Our small cap investment process involves building our own cash flow based valuation models and ranking stocks on a balance of growth, operating margin and capital required. We are very careful to account for the amount of cash required for fixed assets, working capital and intangibles. This process often keeps us away from stocks that often appear to be growing very rapidly but require, in our opinion, far too much in the way of capital (or capital hidden as acquisitions). We are very wary of the amount of working capital required as businesses deploy new investments that more often than not have teething problems. This is the difference between a cash flow based process and an accounting earnings process. We are very comfortable investing in low growth companies provided they have a good combination of margin and capital efficiency. We then overlay this valuation with our 'Eight Commandments' that attempt to keep us away from situations where we think, for example, management are just plain dodgy.

Our investing style, as such, does not fit cleanly into a traditional value or growth bucket. However in a recent note Morgan Stanley put stocks into two buckets according to factors such as profitability, fundamental stability, pay-out and safety. They then classified the stocks into quality or, perhaps harshly, junk. We found the analysis made some observations that fit with some of our long experience with running our portfolio.

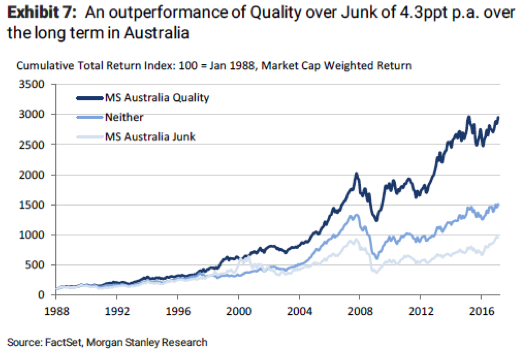

Morgan Stanley found that over the long run quality out performed junk by 4.3% pa.

While this is interesting and possibly not surprising what we found to be more significant was the commentary around the Australian equity market volatility since the start of 2016 when arguably global interest rates, after being pushed down by one mechanism or another for perhaps 30 years, decided to increase.

The periods over the last 18 months when our quality biased portfolio has found most challenging have been February-March 2016 and late 2016-Jan 2017. This coincides with the most pronounced rebounds in what Morgan Stanley describes as junk.

The key question is where are we now.

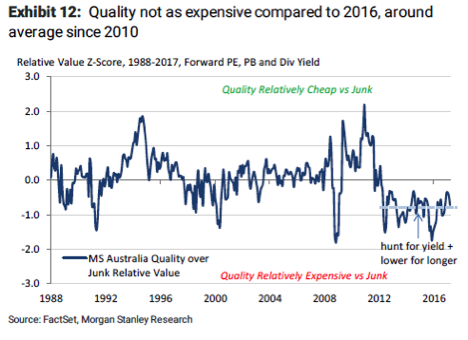

According to Morgan Stanley the premium that investors were prepared to pay for quality when interest rates were going to stay at near zero levels for ever has now been re-priced. They believe, as detailed above that valuation spread is back to more normal levels. Our investment philosophy is just to focus on the companies that we believe will deliver high returns over the long run. We do not adjust our investment process, which has worked very well over the 13 years we have be investing in small caps in Australia.

Perhaps closer to home a good empirical example of the macro themes that Morgan Stanley has discussed in the proposed oOH media (OML) and APN Outdoor (APO) merger. Last week the ACCC raised serious concerns about the merger and the prospect that it will reduce competition. It is by no means clear that the merger will not proceed after undertakings are given and assets are sold. However the announcement was a major impediment for what would be a merger that would yield significant synergies. Despite this the share price of OML is almost 5% higher than the day before the merger was blocked. APO has not fared quite as well and is 5% below the pre ACCC announcement price. However we believe that had this announcement occurred while the market had "premium to junk" valuations on these stocks both would have dropped significantly more than the 5% decline in APO. We focus on individual stocks rather than macro trends. However we believe that this micro example reinforces what Morgan Stanley strategists are saying. After a period of volatility we believe, as always, quality companies with a strong cash flow generating ability are the best option.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity investment capabilities that can also be combined into multi-asset strategies.

1 stock mentioned

UBS Asset Management

UBS Asset Management

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity...

Expertise

No areas of expertise

UBS Asset Management

UBS Asset Management

UBS Asset Management offers investment capabilities and investment styles across all major traditional and alternative asset classes. These include equity, fixed income, currency, hedge fund, real estate, infrastructure and private equity...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment