Reasons for caution on housing exposure

Avoca Investment Management

Avoca Investment Management

The Australian housing sector is critical for both the economy and stock market. New dwelling construction and renovations create jobs and rising house prices creates wealth, which then flows into retail and other consumer-facing sectors. Importantly, new housing activity has tended to run counter-cyclical to the resource CapEx cycle, dropping away as resource CapEx runs hot (interest rates tend to be high leading to lower demand for houses) and then ramping up when resource construction is in the doldrums (as interest rates decline). This symbiotic relationship has helped sustain the longest post-war period of economic growth of any G20 nation.

But these good times are now facing risks. The key question is: has the abnormally extended period of ultra-low rates over the past five years driven house prices and household debt to unsustainable levels as new home buyers pursue the great Australian dream of home ownership?

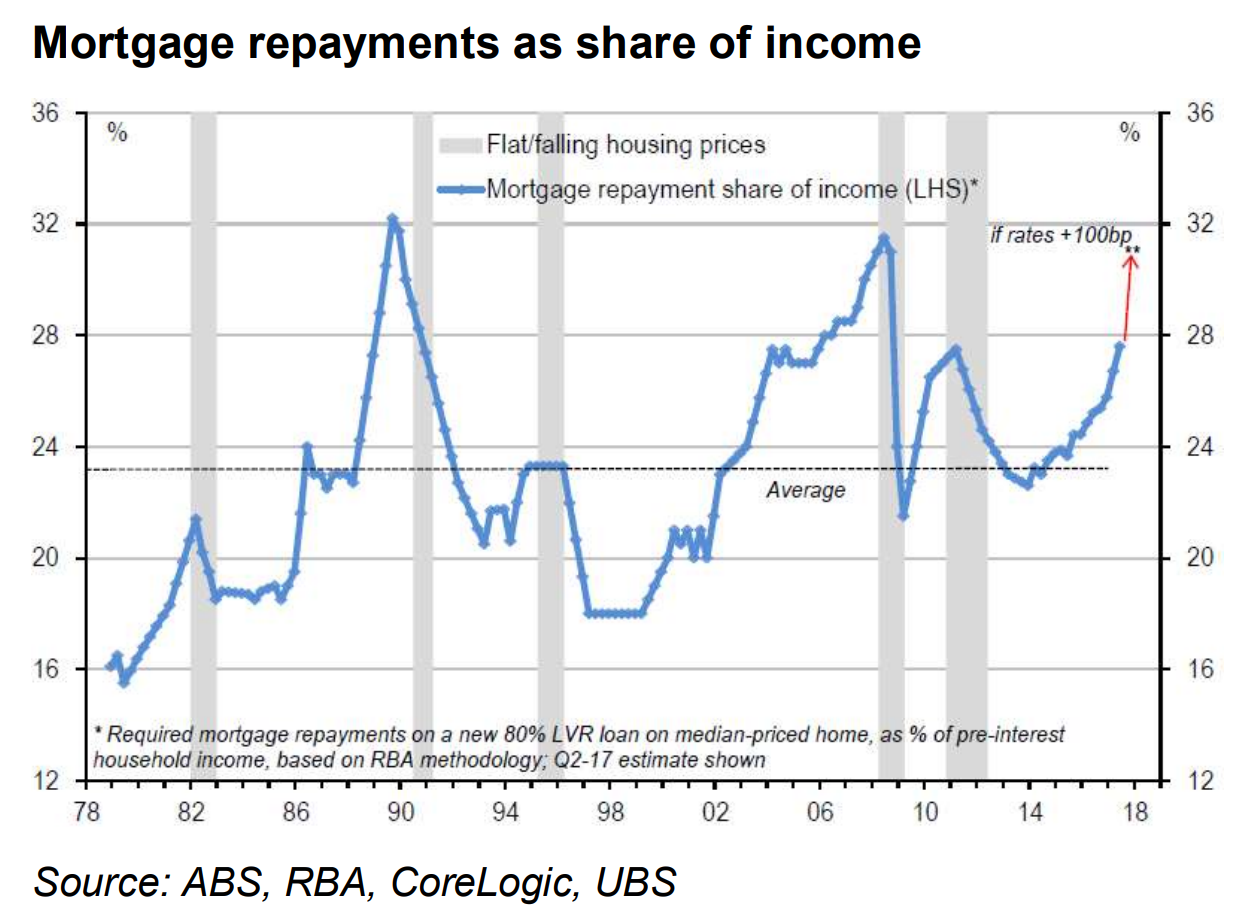

This question is a hard one to answer definitively, due to a lack of comparable data. Ideally, we would like to see household debt versus household investment assets (i.e. a gearing measure), but this data is not available. As a proxy, the RBA and others use mortgage repayments as a share of household income. On that measure and notwithstanding generational low mortgage rates, average mortgage repayments as a share of income are well above the 40-year average. As the following chart details, as little as 100bp of rate increases would take this ratio to levels last seen pre-GFC and before the 1987 stock market crash.

Compounding concerns of elevated household debt is the Australian housing market’s heightened dependence on foreign capital, namely Chinese. While the data is again difficult to come by, anecdotal evidence suggests anywhere between 15% and 30% of all apartment and house sales (new and existing) over the past year have been acquired by foreign buyers. In the long run, there is no reason to think foreign buyers are any less price-sensitive than domestic buyers. In addition, the risk of Chinese capital controls remains ever present and unpredictable. Accordingly, there is a clear risk that foreign buyers withdraw over time—potentially sharply—exacerbating any weakness.

So, this is a heady mix, just as quantitative tightening kicks off in the USA and Europe and global rates start to push up. We see reason to be cautious about domestic exposures in such an environment.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

2 topics

Avoca Investment Management

Avoca Investment Management

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

Expertise

Avoca Investment Management

Avoca Investment Management

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

Expertise

Comments

Comments

Sign In or Join Free to comment