Reporting season not so rosy close up

Profit reporting season looked great from a distance but down in the trenches investors may not have felt that was quite the case. The data shows, on a stock-by-stock or even-weighted basis, that there has been a tempering of expectations across most sectors.

More EPS forecasts were downgraded than upgraded

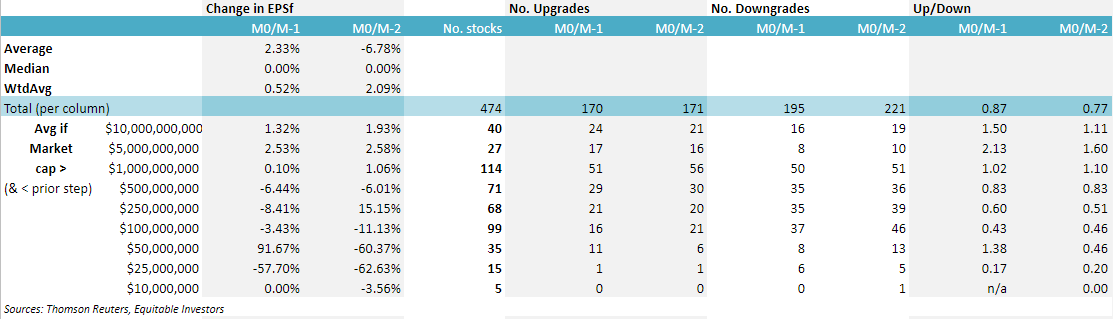

Changes in analysts' forecast EPS made over the course of January and February are a great way of measuring the buoyancy of the profit reporting season as they capture both the impact of the actual financial figures companies reported and the sentiment flowing from companies' outlook statements and guidance.

Quantitative analysts and top-down strategists who have talked up the season that just passed as a 'very strong one' are right - from a market-cap-weighted perspective at least. That's because larger stocks fared better. The weighted average change in EPS expectations over January and February was +2.1%.

However, the unweighted average change in analysts' earnings per share (EPS) expectations across 474 stocks was a -6.8% decline over the course of January and February (based on data from Thomson Reuters). We counted 221 downgrades against 171 upgrades.

Large stocks fared better than smaller stocks

Stocks with market caps greater than $5 billion experienced healthy uplifts in analysts' EPS expectations - both in terms of the simple average and by the number of companies experiencing upgrades as a ratio of those that were downgraded.

Stocks capitalised between $100m and $1 billion faced the opposite scenario - their simple average EPS revision was negative and more of them had expectations reduced than raised.

Figure 1: Changes in consensus EPS forecasts for ASX listings over Jan & Feb 2018 (M0 = March 2; M-1 = 1 month earlier; M-2 = 2 months earlier)

A part-explanation for the divergence between large and small stocks this reporting season is simply the relative level of growth priced in ahead of reporting season. Hopes for smaller companies may have simply been, in aggregage, excessively optimistic.

The EPS growth expectation for the S&P/ASX Small Industrials Index is now 5% for FY18. The heavyweight S&P/ASX 100 Index is now expected to grow EPS 6% this financial year.

That's the reverse of expectations back in December 2017, when analysts were looking for the Small Industrials to grow 6% and the 100 to grow 5%.

When EPS forecasts zig but shares prices zag

Of most interest to Equitable Investors are those stocks that impressed analysts (as indicated by EPS upgrades) but went backwards in terms of share price.

Online "life admin store" iSelect (disclosure: Equitable Investors Dragonfly Fund owns shares in iSelect) is one we believe is not widely understood in the marketplace.

In what is always a seasonally weak half, iSelect delivered earnings that appeared in-line with expectations, demonstrated a strong balance sheet, and resulted in a mild uplift in EPS expectations but also a share price decline of more than 15%.

Radiology stocks Capitol Health and Integral Diagnostics were also stocks that failed to curry favour with the market despite strong EPS upgrades, although their uncertain merger dance probably overshadows the specific financial data points.

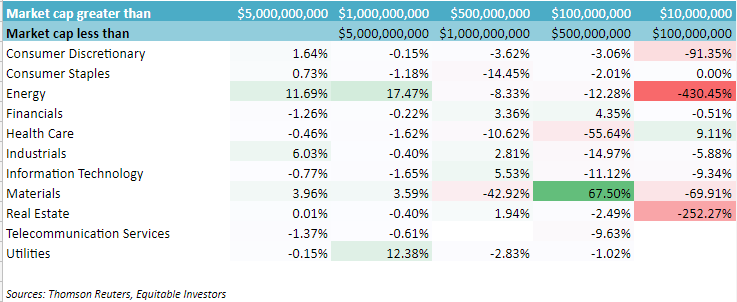

Utilities, Materials & Financials stood out as eight of 11 sectors were marked down

The market's aggregate figures are impacted by the resources sector where wild fluctuations are always on the cards.The Materials sector emerged with a strong average uplift to forecasts but with more downgrades than upgrades.

Financials received a healthy average EPS increase on the back of the majority of changes to expectations being positive - 1.4 up for every 1 down. This was certainly not driven by the banks but rather the emerging players like:

- administration and platform operator, OneVue Holdings,

- finance broking aggregator, Consolidated Operations Group,

- funds management player, Pinnacle Investment Group and

- property funds group, Centuria Capital.

Figure 2: Changes in consensus EPS forecasts over Jan & Feb 2018 - by industry and market cap

Consensus trimmed on leading tech stocks, while consultancies disappointed

Perhaps the outcome of reporting season that may not have been expected was that Information Technology stocks large and small had EPS projections trimmed.

Leading online classified plays REA Group and Carsales.com were among IT stocks to take a hit. So were some of the higher profile tech names of recent time like Afterpay Touch and WiseTech Global.

A number of IT consulting businesses found the going tough for differing reasons - analysts now have lower earnings targets for DWS, RXP Services and Empired.

RXP lost some clients, DWS noted pressure on the rates it charges and Empired's New Zealand government-facing business experienced a lull in activity amid that nation's federal election (disclosure: Equitable Investors Dragonfly Fund owns shares in Empired).

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Martin established Equitable Investors and the Dragonfly Fund in 2017 after serving as an investment manager with Thorney Investment Group. Equitable seeks out unique opportunities with intensive research and constructive corporate engagement

3 stocks mentioned

Martin established Equitable Investors and the Dragonfly Fund in 2017 after serving as an investment manager with Thorney Investment Group. Equitable seeks out unique opportunities with intensive research and constructive corporate engagement

Expertise

Martin established Equitable Investors and the Dragonfly Fund in 2017 after serving as an investment manager with Thorney Investment Group. Equitable seeks out unique opportunities with intensive research and constructive corporate engagement

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX playmakers making things happen

Livewire Markets