Royal Commission final report released

The market was soft on open this morning giving back all the gains and them some implied by the SPI Futures on Friday (+20pts), however buyers stepped up to the plate largely focussing on the banking stocks ahead of the Hayne RC report which is just out – my initial thoughts after a quick scan below. Obviously most focus on the RC today, however eco data out this morning was also soft…Building Approvals -8.4% versus 2% expected which took the wind out of the sales of the AUD.

Overall today, the market was strong – surprisingly in the face of the weaker data + of course the RC final report…

The ASX 200 closed up +28points or 0.48% to 5891. Dow Futures are currently trading up +8pts.

ASX 200 Chart

CATCHING OUR EYE

Royal Commission (RC); All in all, I actually think the outcomes here will be good for banks stocks – while I haven’t had a lot of time to review some high notes below;

In 76 recommendations, Hayne recommends tougher regulation, more scrutiny of pay and culture and pushes the securities regulator to consider court action as a first option. But stops short of calling for them to be forcibly broken up to stop them offering financial advice and wealth management. Basically, vertical integration stays which is a win for AMP and IOOF plus Westpac as the bank that has kept their wealth business (all else have sold).

"Enforced separation of product and advice would be a very large step to take,’’ Hayne wrote. ``It would be both costly and disruptive. I am not persuaded that it is necessary to mandate structural separation between products and advice.’’

The root cause of much of the industry’s wrongdoing is pay and bonus structures, Hayne said. The prudential regulator APRA will be tasked with stepping up supervision of remuneration, and banks should review their pay systems for frontline staff at least once a year.

Mortgage brokers to be paid by the borrowers, not the banks. That’s tough for the brokers but good for the banks with big domestic footprints – best for WBC and CBA + also good for comparison sites I would think.

No criminal charges recommended…

More to come in the MM AM report tomorrow

Commonwealth Banks (ASX:CBA) Chart

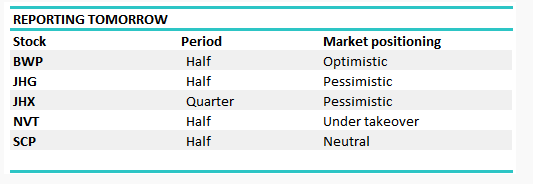

Reporting; No stocks out with reports today – BLD downgraded we start to get a few out tomorrow. CBA on Wednesday a big one.

Western Areas (ASX:WSA) +5.7%; One of the resource stocks that recently plumbed new 52 week lows and is now starting to see some strong buying. Looking at resources more generally, the Australian miners (XJR) have added a whopping ~17% (USD terms) since 20 December when the index plumbed a 15 month low. This was at the tail-end of a tumultuous year (XJR down ~11%) whipped around by Trump-Trade –Tariffs with most of the downdraft in the final quarter. We like WSA, targeting higher prices but remember, resources are very cyclical.

Western Areas (ASX:WSA) Chart

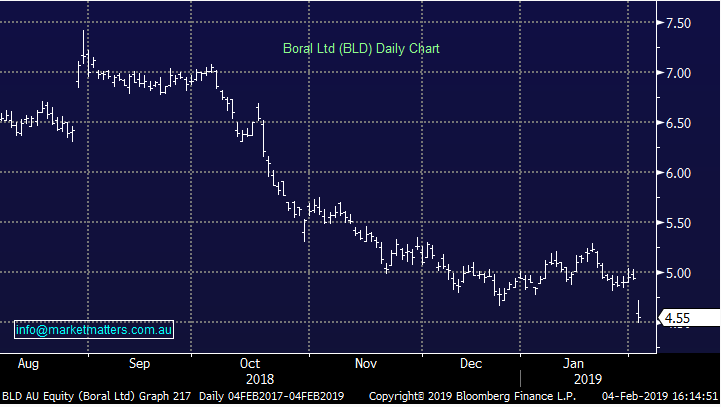

Boral (ASX: BLD) -7.89%; Despite record levels of infrastructure spend locally and in the US, Boral today lowered guidance heading into the first half result. The building materials company is now expecting little to no growth in EBITDA in the first half of FY19, while guiding to NPAT of around $200m.

Commentary for the full year result also turned a little sour with Australian operations seen flat for the year down from previous guidance of low single digit growth, North American operations to see 15% growth at the EBITDA line which is down from 20% growth at previous guidance, and profits from the USG Boral joint venture now expected to be slightly lower in FY19, down from profit growth of around 10%.

Also concerning investors is further warnings around a strong second half skew to the result, with Boral pointing to volume lags, project delays and extreme weather in the first half holding back earnings despite strong underlying market conditions.

Boral will report their first half result on February 25.

Boral (ASX: BLD) Chart

Broker Moves;

- Flight Centre Upgraded to Hold at Morningstar

- GUD Holdings Upgraded to Overweight at JPMorgan; PT A$12.70

- Asaleo Care Upgraded to Outperform at Credit Suisse; PT A$1.25

- Vocus Reinstated at Credit Suisse With Neutral; PT A$3.25

- TPG Telecom Reinstated Underperform at Credit Suisse; PT A$5.60

- Telstra Reinstated at Credit Suisse With Neutral; PT A$3.10

- Sydney Airport Cut to Underperform at Credit Suisse; PT A$6.40

- IOOF Holdings Downgraded to Sell at Bell Potter; PT A$4.35

- Insurance Australia Upgraded to Overweight at JPMorgan; PT A$8

- Sandfire Downgraded to Accumulate at Hartleys Ltd; PT A$8.36

- Resolute Mining Upgraded to Buy at Hartleys Ltd; PT A$1.52

- Rio Tinto Upgraded to Add at AlphaValue

Never miss an update

Stay up to date with the latest news from Market Matters by hitting the 'follow' button below and you'll be notified every time I post a wire.

Want to learn more about Market Matters? Hit the 'contact' button to get in touch with us.

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

2 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 2 standout ASX names for FY26

Livewire Markets

Commodities

Central banks are doubling down on gold - should you?

Livewire Markets