SARS is not a model for Coronavirus

Drawing parallels between the two outbreaks is tempting but risky.

Key Insights

-

The potential impact of the COVID‐19 virus on the Chinese economy has been compared with that of the SARS virus in 2003.

-

However, there were external factors weighing on the Chinese economy in 2003 that do not exist today.

-

We believe our approach, based on calculating the impact of lost working days on production, provides a more accurate assessment of the economic impact of COVID‐19.

Commentators seeking to understand the long‐term implications of COVID‐19 (a coronavirus) are frequently comparing it with the 2002–2003 severe acute respiratory syndrome (SARS) outbreak, which had a severe impact on both the Chinese and the global economies. But the 2003 SARS outbreak coincided with slowing global gross domestic product (GDP) growth, the Iraq War, and higher oil prices. So is SARS really a good case study for understanding the likely economic effects of COVID‐19? And if it is not, what other evidence can we turn to?

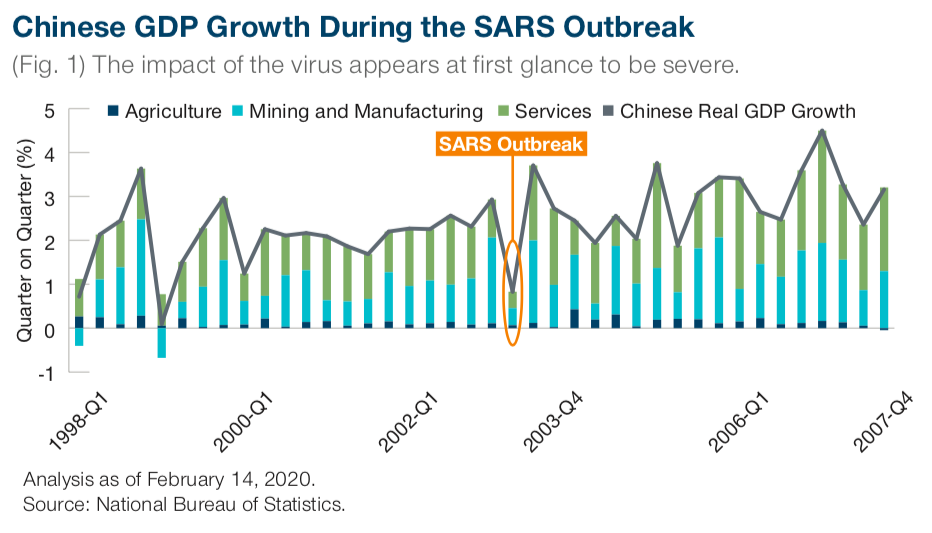

The SARS outbreak caused 8,098 cases and 774 deaths in 17 countries. Although the first cases appeared as early as November 2002, it was not until April 2003 that the World Health Organization issued a global health alert. Shortly afterwards, the Chinese authorities announced that all primary and secondary schools would be closed for two weeks and closed down other public venues, such as theatres and discos.

It was also in April 2003 that the first quarantine measures were introduced. As Figure 1 shows, this coincided with a significant reduction in Chinese Q2 2003 GDP growth in which the quarter‐on‐quarter growth rate fell by 2.1% (from 2.9% in Q1 2003 to 0.8% in Q2 2003). This decline was driven by a reduction in services and manufacturing growth, which was likely partly caused by containment measures taken by the Chinese government. Many observers, therefore, argue that the SARS episode is a good case study from which to extrapolate the effects of COVID‐19.

However, there are significant differences between the situation today and that of China in 2003. Then, China composed only 5% of the world economy and was just in the process of becoming central to global supply chains on the back of its World Trade Organization accession in 2001. Rather than being a driver of the world economy, China was more a recipient of fluctuations and shocks from elsewhere.

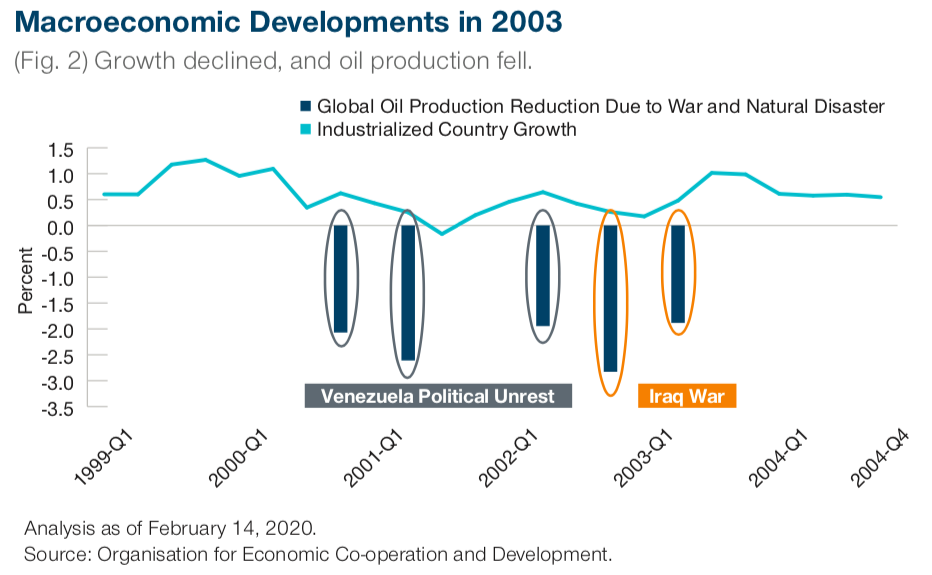

Moreover, there were two important global economic developments occurring at the same time (Figure 2): First, in early 2003, growth in G7 economies (75% of global GDP at

the time) was slowing; and second, in anticipation of the U.S. invasion of Iraq, which reduced global oil production by around 2%. The Q2 2003 Chinese slowdown is often wholly attributable to SARS, but is it possible that these two macro factors may also have played a part?

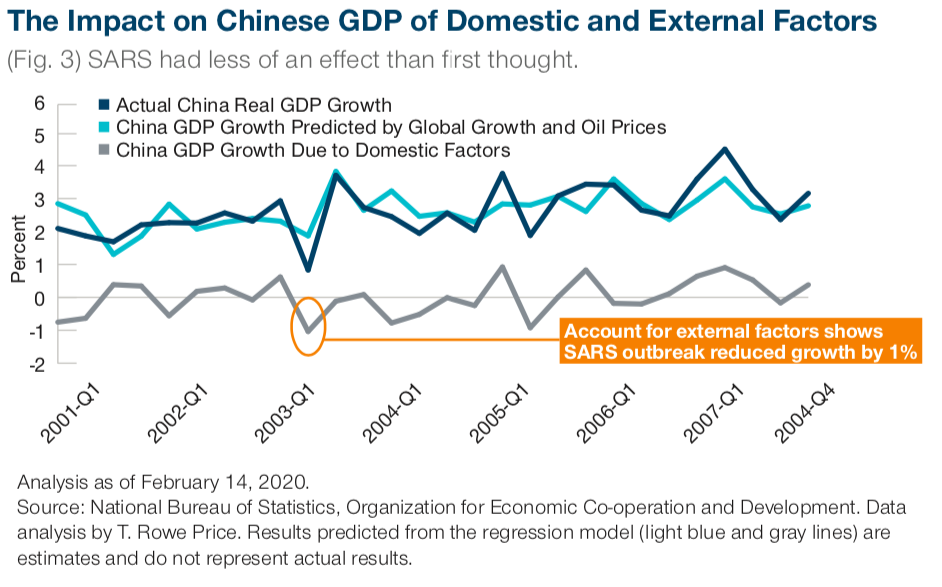

We used a simple linear regression analysis to determine the extent to which industrialized country growth and real oil price growth rates impacted Chinese GDP growth from Q1 2001 to Q4 2007. The residual from this regression shows the impact on growth from idiosyncratic factors over the period. Figure 3 shows the results from this exercise. The grey line shows Chinese growth predicted by the global factors in the regression model and indicates that these would have led to a moderation of growth in China without the outbreak of SARS. The residual weakness in growth, which can be attributed to China‐specific factors in that quarter, is 1%—much lower than the 2.1% effect that can be calculated by looking at quarterly growth rates alone.

Overall, the coincidental global slowdown and rise in real oil prices mean that the effect of SARS was likely greatly exaggerated in Chinese GDP data. In our view, SARS is, therefore, not a good case study for understanding the potential economic consequences of COVID‐19 on Chinese real GDP growth.

If SARS is not a good case study to assess the economic impact of COVID‐19, what should investors look at instead? We believe that the most useful approach is to quantify the effect of lost working days on overall production. We estimate that the current measures imposed by the Chinese government through early February have led to eight lost working days for the country as whole. A reduction in one working day in Q1 leads to roughly a 0.4% loss in output, meaning that the eight lost working days so far translate into a quarterly growth reduction of 3.2%. This number is 50% larger than 2.1% growth impact measured during the SARS outbreak, and three times as large as the estimated 1% impact adjusted for external factors. Although this number could rise further, it is significantly smaller than extrapolating the economic impact based on virus cases in China, which, with 78,000 cases to date, is 15 times larger than the 5,237 cases that China experienced during SARS.

We believe that by looking at the sensitivity of growth to each working day lost (0.4% of GDP), we can get a much better sense of the economic impact of COVID‐19 than can be obtained from arbitrarily scaling up the consequences of SARS. The same method can be applied to the impact of COVID‐19 on growth in other countries that have been badly hit by the virus, including Italy.

We will continue to track high‐frequency indicators around travel patterns, pollution, and coal consumption at power plants. This will help us to more accurately gauge how many effective working days have been lost in real time and, therefore, what the economic impact is likely to be—and to do so significantly ahead of the publication of longer‐term hard data.

Invest with confidence

T. Rowe Price focuses on delivering investment management excellence that investors can rely on—now and over the long term. Hit the 'follow' button below for more of our investment insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

T. Rowe Price is an investment management firm focused on helping clients meet their objectives and achieve their long-term financial goals. We manage assets across a broad range of active equity, fixed income and multi-asset investment strategies.

1 topic

T. Rowe Price

T. Rowe Price is an investment management firm focused on helping clients meet their objectives and achieve their long-term financial goals. We manage assets across a broad range of active equity, fixed income and multi-asset investment strategies.

T. Rowe Price

T. Rowe Price is an investment management firm focused on helping clients meet their objectives and achieve their long-term financial goals. We manage assets across a broad range of active equity, fixed income and multi-asset investment strategies.

Comments

Comments

Sign In or Join Free to comment