Signs of recovery... but are equities too expensive?

The global community continued to battle the COVID-19 pandemic through April, with an increasing number of economies entering or extending near-entire lockdowns of activity. Cumulative cases topped 3 million and deaths exceeded 220,000. Yet despite this, bond yields resisted the temptation to plumb new lows and equity markets moved steadily higher, adding to their late-March rebound. This unfolded as many of the signals we outlined for a sustained equity market trough were ‘checked off’ our list in April. But key items remain unchecked.

Moreover, equity markets are now just 20% below their pre-pandemic highs and valuations little different. Arguably, the uncertainty of, and the damage to, the outlook warrants a larger discount. Thus, we remain both comfortable with our modest overweight equities position (since mid-March) and cautious for now about moving more overweight, despite rising odds of a H2 2020 recovery. This month, we discuss five active portfolio decisions investors should be considering. We also move tactically overweight domestic relative to European equities.

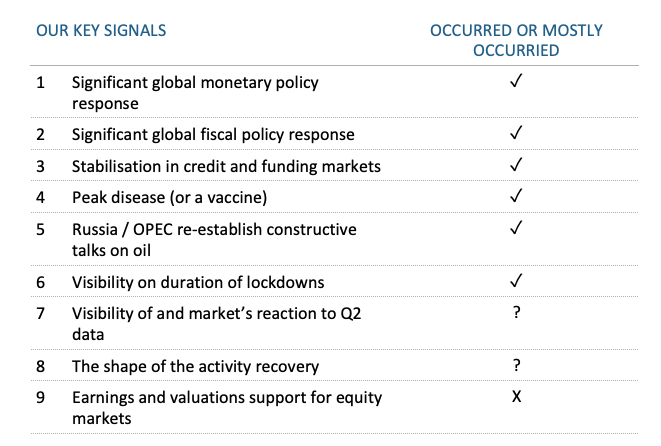

Many of our risk signals were checked off through April

In March, as the global crisis was unfolding, we introduced a list of key signals we would be monitoring to help us assess when equity markets specifically, but risk appetite more broadly, may establish a sustained trough. While a number of these were already checked off our list at the start of March, the number has now grown to six out of nine (see the table below), and some of the remaining items may be achievable over the coming month or so. As we highlighted last month, a number of our key signals had been triggered, though additional progress has unfolded in April.

1 and 2—Justifiable panic by policy makers over the sharply weaker outlook for growth had already led to significant monetary and fiscal policy support during March. By the of end April, more central banks had cut interest rates than during the GFC, and emerging markets central banks were particularly active. Latest estimates by UBS put the global fiscal stimulus at just over 3.7% of world output, more than twice that during the GFC (and up from around 1% in the middle of March).

3—Central banks have continued to support short-term funding markets in April. The US Federal Reserve (Fed) announced expanded lending facilities and limited purchases to non-investment grade debt. The European Central Bank (ECB) made similar decisions in late April, supporting corporate debt that has been downgraded from investment grade. In late April, the Bank of Japan (BoJ) scrapped a limitation on it buying government bonds.

Source: Crestone

During April more of our key signals were triggered:

4—COVID-19 cases globally have continued to rise, surpassing 3.2 million by end-April and with over 220,000 deaths. But for those regions at the centre of the outbreak in early March (Europe and the US), the pace of new infections has slowed in April. While the risk of new outbreaks is material—and the recent pick-up in less developed economies (such as Africa and India) bear watching—markets have assessed that ‘peak disease’ has been reached.

5—In early April, the Organization of the Petroleum Exporting Countries (OPEC) and Russia agreed to historic production cuts, though delayed their start until 1 May. Late April saw instability return to the oil market, as diminishing storage facilities saw near-term contracts slump to negative pricing. However, cuts to production in May are expected to stabilise prices, albeit prices are likely to stay at low levels for some time.

6—Reflecting a slowing pace in new cases—and the rising economic and social cost of lockdowns—governments across the world have been announcing phased returns to work. In the US, a number of states are allowing restaurants and cafés to serve customers. Since late March, governments in Europe (including Spain and Italy) have been announcing the modest unwinding of restrictions.

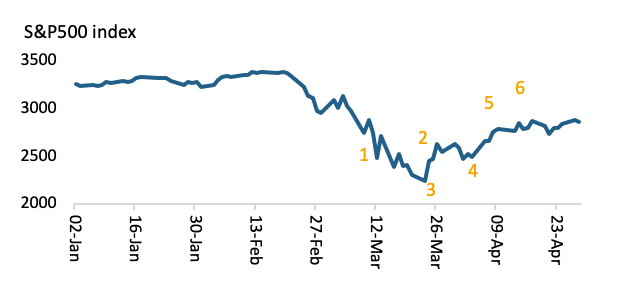

Equity markets have rallied as signals have been met

SOURCE: BLOOMBERG, CRESTONE.

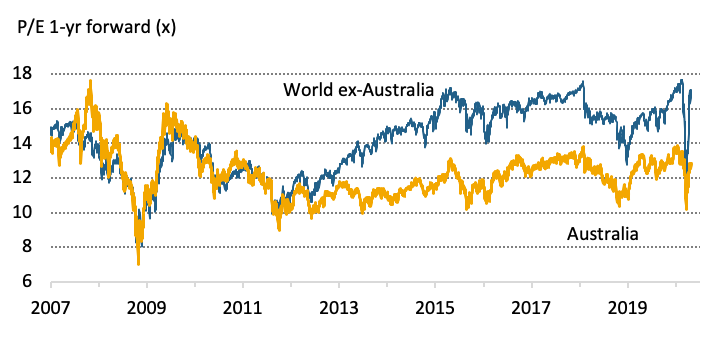

Valuations have returned to near pre-virus highs

Source: UBS, Crestone.

While the strength and resilience of the rebound in equity markets has been somewhat surprising, as the chart above shows, it has broadly done so as the key signals we have been monitoring have been achieved. However, a number of our key signals remain ‘un-checked’:

7—While recent data has begun to shed some light on the extent activity has been sharply curtailed through Q2—such as the recent April collapse in global leading indicators—markets are yet to be confronted by sharp rises in unemployment, which is broadly expected to jump from 40-year lows to more than 10% of workforces in the coming couple of months.

8—As detailed in last month’s Core Offerings, uncertainty remains over whether there will be a V-, U- or L-shaped recovery. This will likely have a material impact on risk appetite and earnings. We continue to view a U-shaped recovery as the most likely (embodying a global ‘return to work’ through late Q2 and Q3). With risk signals 1-6 having now been checked off, the risk of an L-shaped recovery has also fallen through April.

9—As the second chart above shows, having approached prior points of valuation support at the market’s trough on 23 March, the recent rebound has elevated valuations back to near their pre-COVID-19 levels. We remain cautious ahead of a fuller reflection of the macro outlook in company earnings and look to re-assess our positioning after the current US and European Q1 earnings seasons.

Adjusting our regional equity tilts

Based on our signals, we remain both comfortable with our modest tactical overweight to equities (from mid-March) and cautious for now about moving more overweight, despite rising odds of a H2 2020 economic recovery. While not convinced markets will retest their prior lows (and are inclined to buy into any weakness), the recent rally has cautioned us about moving more overweight equities given relatively full valuations. This is particularly relevant ahead of better understanding the extent of Q2’s economic weakness, and the inherently messy process of restarting economies.

This month, however, we are

adjusting our preferences for regional equity markets, initiating an overweight

to Australia relative to Europe. Several factors favouring Australia underpin this decision:

Faster trading partner recovery—Australia’s closer ties than Europe to Asia, and particularly China’s faster domestic economic pick-up, are likely to support Australia’s recovery through H2 2020 and 2021.

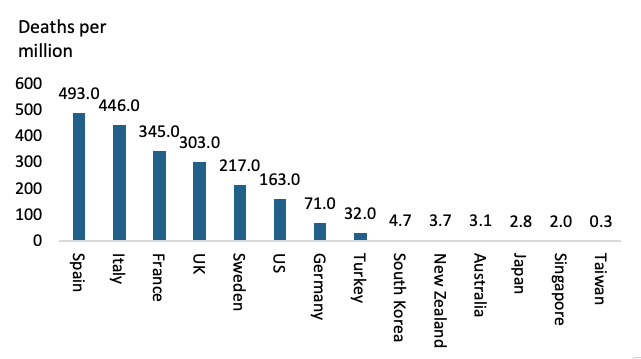

Faster recovery from COVID-19—Europe has struggled to deal with the pandemic. The chart (below) highlights data on COVID-19 deaths per million population and the greater negative impact of the virus in Europe compared with Asia, including Australia. The easing of lockdown restrictions will potentially see a faster return to normal in Australia’s consumer patterns.

Better capitalised banking system—Australia’s ample banking system liquidity which, unlike Europe, is now at historically low rates, should aid a faster recovery in activity. In contrast, with banks such a large component of European indices (and dominant in their transmission of credit), flat yield curves and rising bad debts are likely to weigh on European indices.

Faster earnings revisions and capital raisings—Domestic equities have underperformed the MSCI World index in April, likely reflecting in part the significant level of capital raisings taking place. MST Equity Strategy also believes that “the lows of the bear market are now behind us and stock indices will now trend higher although profits continue to fall.”

Greater relative discount to the US market– Domestic equities have corrected to a 15% discount to the US, its largest since early 2018. European equities, in contrast, have ventured to their current (larger) 25% discount to the US numerous times in the past few years. According to Société Générale, “half of the European sectors are already pricing in a V-shaped recovery”, not a view they hold when considering the US equity market.

Europe may suffer longer impacts from the COVID-19 outbreak

Source: MST Marque.

Five active investment decisions

Many investors may view current equity market valuations as lacking near-term attractiveness. However, this doesn’t mean there is nothing to be done in terms of portfolio management. As Sir John Templeton writes, “the first rule of investment is ‘buy low and sell high’, but many people fear to buy low because of the fear of the stock dropping even lower. Then you may ask: ‘When is the time to buy low?’ The answer is: When there is maximum pessimism.” There are active decisions investors can be considering today:

Firstly, be invested. Periods of extreme market moves tend to encourage investor efforts to time markets. Human nature and emotion almost demand it. However, outperforming a ‘buy-and-hold’ investor requires two near-precise decisions—when to exit and when to re-enter the market. Academic analysis suggests this is at the absolute limits of human ability and almost invariably a recipe to long-term portfolio underperformance.

Secondly, actively rebalance portfolios in line with your risk appetite. After a 30% correction in equity prices, most portfolios have drifted 8-9% below their target exposure. Taking the opportunity to selectively rebalance back toward target is a worthy endeavour. During the GFC, an investor who held a 40% equity weight before the crisis unfolded had only a 20% weight at the trough, leaving them only half-exposed to the 68% rally in the first year of recovery.

Thirdly, just because the index

looks expensive doesn’t mean that all the sectors or companies in that index

are also expensive or without investment merit. Recessions bring opportunity to

make great long-term investments. However, investors need to focus on assets

that have near-term downside resilience (those with strong balance sheets and low gearing) if the outlook proves weaker than expected.

Fourthly, drawdowns typically nurture a focus on quality. Even if there is a desire to leave a portfolio’s equity exposure unchanged, investors can actively rotate out of underperforming companies (or sectors) into those with more potential to rebound as a recovery unfolds. This quality focus should extend to fund managers and ensuring the right mix of manager styles (and risk) within each asset class.

Finally, keep an eye on the long-term themes that are emerging. This crisis, particularly given its unique human element, is likely to have accelerated structural themes than can be profitable to expose a portfolio to, even during the crisis. Some sectors will clearly have their strong thematics accelerated, such as online purchasing, home delivery, health care and home-based technology and entertainment. Others could find their structural headwinds intensified, such us cruise-liner travel, bricks and mortar retailing and central business district office space. Still, others could be facing new unanticipated demand headwinds, such as short-haul business travel and accommodation.

Learn what Crestone can do for your portfolio

With access to an unrivalled network of strategic partners and specialist investment managers, Crestone Wealth Management has one of the most comprehensive global product and service offerings in Australian wealth management. Click 'contact' below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment