SimCorp: a niche supplier to the finance industry

Copenhagen headquartered SimCorp is the global leader in integrated software solutions for large asset managers, insurance companies and sovereign wealth funds. Its main product, SimCorp Dimension, builds on the company’s state of the art investment book of records (IBOR) technology to provide front-to-back office multi-asset class functionality to its clients. More than half of the top 50 global investment managers are Dimension users and US$20 trillion was managed through the system in 2018.

Unusually for a company that is a supplier to the finance industry, SimCorp isn’t a particularly cyclical business as revenue is earnt from license fees which are independent to the amount of funds clients have under management. SimCorp’s products are embedded within their client’s daily operations, including compliance with government regulation, and as a result are not considered a discretionary expense. It also helps that customers are large institutions such as the Abu Dhabi Investment Authority, the Healthcare of Ontario Pension Plan and UBS Asset Management, that can easily withstand periods of market volatility. In addition to high revenue visibility, SimCorp displays many of the traits we like to see in a business.

Early mover

SimCorp’s 50-year long presence in the industry and early

focus on integrated solutions lie at the core of the company’s

competitive advantage.

SimCorp software allows clients to run incredibly complex operations smoothly and accurately, and once adopted it is risky and disruptive for them to migrate to an alternative provider. Over the years, the recurring revenues from this sticky client base has enabled SimCorp to fund the development of one the best solutions available in the market today. It is now extremely difficult for smaller peers to keep up with, let alone to challenge, SimCorp’s leadership.

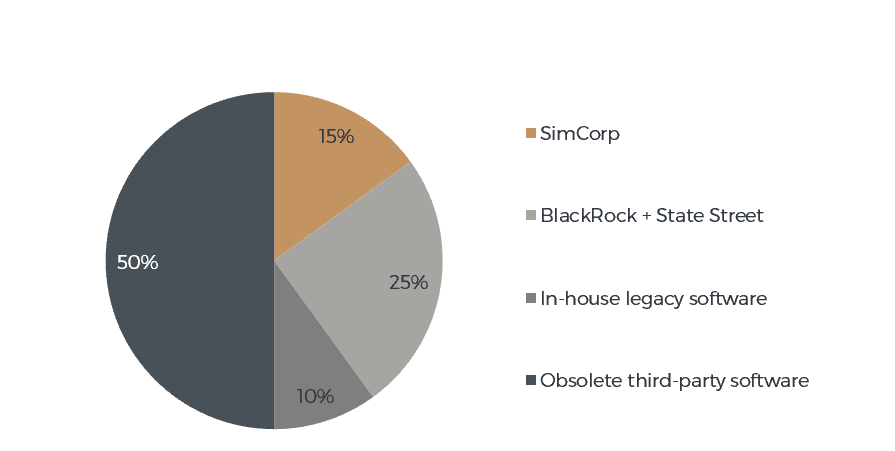

Figure 1: Global Market Shares

Sources: FactSet, Company Filings, Fairlight Estimates

Sources: FactSet, Company Filings, Fairlight EstimatesWhilst Dimension can be purchased as one solution, clients

tend to purchase its individual modules over time in order to

minimise implementation risk. SimCorp has developed its

modules organically rather than through M&A, which allows

for seamless integration, placing SimCorp at an advantage when clients seek to adopt additional software solutions

when compared to standalone solutions. Aggregating

independently-developed pieces of software is not a

straightforward process and carries multiple risks. So, trying

to replicate SimCorp’s level of integration through M&A is

problematic, even for well capitalised new entrants.

Great prospects for growth

SimCorp currently has a leading 15% global market share. But,

importantly, to grow it doesn’t need to displace BlackRock

and State Street, the other two leading industry players,

which would not be easy given the above-mentioned high

switching costs that users experience.

Rather, SimCorp’s main growth opportunity is to win over

financial institutions that are currently using outdated

software and are looking to upgrade. Such institutions form

the majority of the addressable market (Figure 1). In addition,

another 10% of the addressable market is comprised of inhouse systems which are quickly becoming obsolete due to

the increasing demand from clients for accurate performance

reporting and regulatory compliance. Error prone excel

spreadsheets and clunky products that have been coded

internally are likely to be replaced over time by the third party

software designed by Simcorp, BlackRock and State Street.

SimCorp should be able to expand its business for many years

to come.

Attractive and well managed business

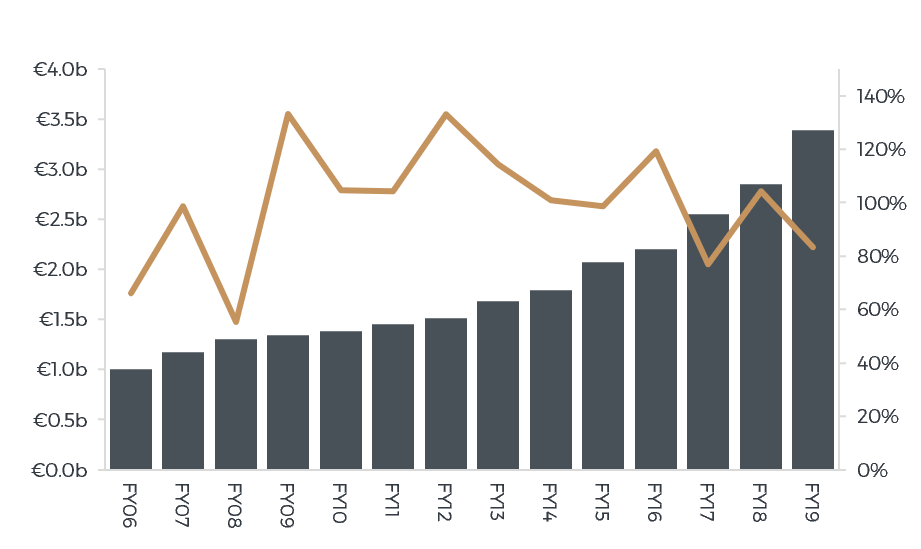

Given the nature of software businesses where development

expenses are mostly incurred upfront, SimCorp doesn’t

require much capital to grow. Since 2006, the company has

grown sales by almost four times while achieving an average free

cash flow conversion of 99% (Figure 2).

SimCorp has a long serving management team and an

engaged workforce which collectively own about 5% of the

company’s shares. Management is quite conservative –

research and development are fully expensed every year and

the company has a negligible amount of debt. Management

has been paying most of the annual free cashflows to

shareholders in the form of dividends and buybacks and we

expect this to continue, even during this difficult year.

Figure 2: Sales (LHS) and Cash Conversion (RHS)

Sources: FactSet, Company Filings, Fairlight Estimates

Sources: FactSet, Company Filings, Fairlight EstimatesThe Fairlight View

Due to the COVID-19 induced sharp and indiscriminate sell off across global stock markets, the Fairlight Global Small & Mid Cap Fund was recently able to establish a position in SimCorp at an attractive multiple of free cash flow.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alvise is a partner and portfolio manager for the Fairlight Asset Management Global Small and Mid Cap Fund. Alvise previously worked at Forager Funds for more than six years where he focused mainly on global companies.

4 topics

Alvise is a partner and portfolio manager for the Fairlight Asset Management Global Small and Mid Cap Fund. Alvise previously worked at Forager Funds for more than six years where he focused mainly on global companies.

Expertise

Alvise is a partner and portfolio manager for the Fairlight Asset Management Global Small and Mid Cap Fund. Alvise previously worked at Forager Funds for more than six years where he focused mainly on global companies.

Expertise

Comments

Comments

Sign In or Join Free to comment