SolarEdge: fair value, exceptional growth

Solar power is now the cheapest form of energy production, second only to wind. Those economics have seen rapid grid defection leading to an increase in grid power costs as well as huge latent demand for battery storage. SolarEdge (SEDG) has ridden that rise in demand, and with its unique capabilities in innovation, has become one of the world’s leading inverter manufacturers. They now look to leverage those capabilities into battery storage and virtual grid solutions. The company has revenue growth of 44.7% CAGR over the last four years, produced $259m USD in cash flows from operations in FY19, and funds all its growth from internal cash flows.

Subsidisation Unlocked a Wave of Economic Surplus

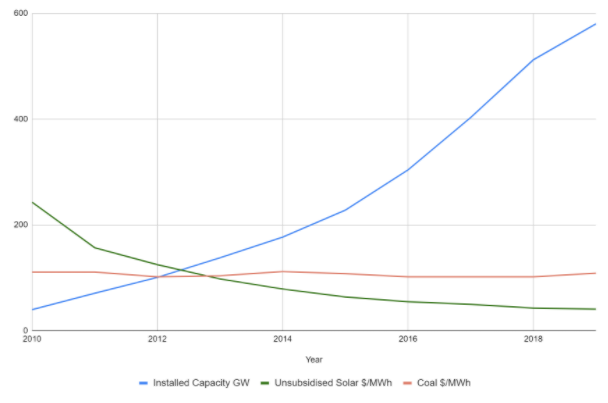

Years of PV subsidisation led to a rapid uptake of solar, increasing sales volumes and in turn, greater competition amongst solar manufacturers and installers. That competition lowered the price of rooftop PV to a point where it became a cheaper source of power than grid supply. At that time the velocity of solar uptake really took off, as did its viability, with the price of unsubsidised solar now significantly lower than coal, gas, or nuclear power. Chart One below shows the rise in installed capacity of solar energy and its decrease in cost in $/MWh as compared to power produced by coal.

Installed Solar Capacity (GW), Unsubsidised Solar ($/MWh) and Coal ($/MWh).

Chart 1. Cost of unsubsidised solar and coal at utility scale vs growth of installed solar capacity 2010 to 2019 (Source: Lazard Levelised cost of energy analysis, 2019 & PV Magazine, 2020).

Chart 1 above illustrates the influence of the reduction in the cost of solar once it became less than coal. Installed capacity begins to spike upwards from around 2014 which is shortly after the cost of solar falling below coal. The continual downward pressure on pricing means that solar subsidisation is no longer a part of its economic viability.

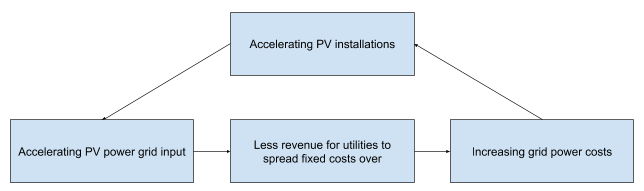

Less Revenue to Spread Enormous Fixed Costs for Grid Suppliers

Rapid uptake of PV, by default, results in less usage of grid supply. That means less revenues to absorb the massive fixed costs of utilities, which in turn forces them to increase prices, especially at night when solar can’t compete. “Every minute on average, 6.5 solar panels are installed on Australian rooftops” (ABC News. Oct, 2018).

PV Demand Excellerating

Figure One. Drivers of PV demand acceleration.

Figure One above shows the relationship between solar installations, increased COGS as a portion of revenue for utilities and subsequent rises in grid power costs further accelerating demand for PV installations. This situation has led to huge latent demand for batteries.

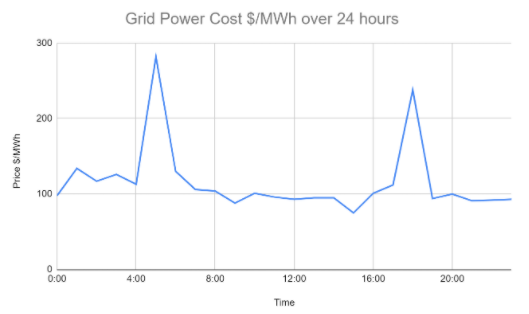

Chart 2. Peak pricing relationship with demand and daylight (Source: Australian Energy Market Operator).

Chart 2 above highlights the power price spikes outside of daylight hours when usage peaks. The situation led to a huge latent demand for batteries, waiting to be realised the moment they become economically feasible in residential applications. SolarEdge is currently building a $95m USD 2GW factory in South Korea that is expected to bring the costs of residential batteries down as it has done in its inverter business.

Exceptional Growth

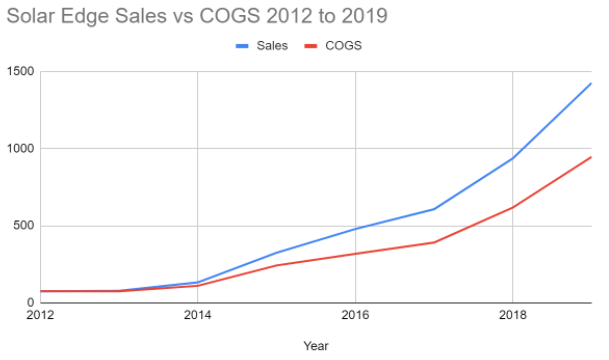

The effects above led to remarkable growth for SolarEdge with revenues growing by 44.7% CAGR over the last 4 years. It is now the largest inverter manufacturer in the world. SolarEdge has maintained a focus on maintaining margins as it has lowered the price of its products.

Chart 3. SEDGE sales and cost of goods sold (COGS) from 2012 to 2019 (Source: Factset).

Chart 3 above shows growth in sales and COGS from 2012 (when COGS were higher than sales) to 2019. A focus on maintaining margins while creating a larger market by lowering prices has given SolarEdge scaling effects.

Revenues over the last three years have grown by 43.75% CAGR while funds from operations has grown at 81.15% CAGR. Lowering prices has been necessary to increase the addressable market of solar, making it more viable in more areas. Europe was not traditionally a native solar application due to its low number of daylight hours per year. However solar is now growing very quickly and Europe made up over 26% and 30% of the company’s total revenues in FY18 and FY19 respectively, sustainable stocks outperform.

Diverse Revenue Geographies and Products

59.8% of revenues in Q2 FY20 were generated outside of the US. Revenues were made up of:

US - 40.2%

Europe - 46.5%

Rest of World (Mostly Australia) - 13.3%

SEDGE is diversifying its revenue streams outside of the residential market with 56% of revenues now coming from commercial installations and SEDGE now winning utility scale tenders. SEDGE currently offers:

Energy Hub Inverter with Prism Technology

Single Phase Inverters with HD-Wave technology for residential applications ranging from 1 to 11.4 kW

Three Phase Inverters ranging from 4 to 100 kW

120 kW Three Phase Inverters with Synergy Technology

EV Charging Inverter

Smart EV Charger

Commercial battery storage by Kokam

Uninterruptible power systems (UPS)

Power Optimisers

Solar panels

PV Monitoring

Software

Significant Replacement Market Coming

The lifespan of an inverter is approximately 10 -15 years. A significant replacement market is emerging as the first wave of installed inverters approach replacement age.

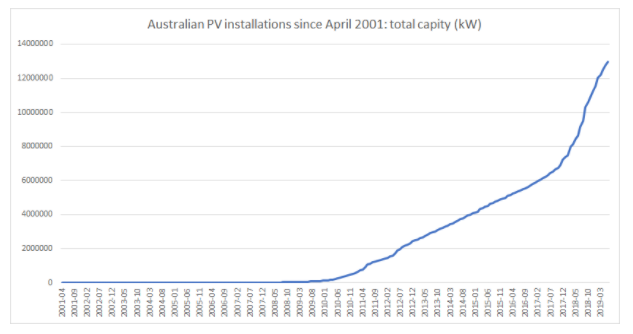

Chart 4. Total installed PV capacity (kW) since April 2001. (Australian PV Institute, 2019)

Chart 4 above shows the significant increase in PV installations from 2010. Using Australia as an example we can see how the first wave of inverters installed are approaching replacement age from 2020 . The number of inverters requiring replacement will dramatically increase every year proportional to the installed capacity of 10 - 15 years prior. This time, people will be looking for an option that can handle both PV and battery.

Strategy

SolarEdge is diversifying away from pure solar into battery storage (residential, commercial, & UPS), e-mobility and virtual grid solutions.

Residential and Commercial Battery Storage Solutions

Battery production is set to begin H1 2022 with the operation of the autonomous Kokam factory in South Korea. McKinsey research (2015) stated that “the market for distributed battery installations in the United States is set to expand by as much as 50% per year.” In 2018, SolarEdge took a bold move into the energy storage market with the purchase of Kokam Batteries in South Korea. Around the same time, they purchased SMRE, a producer of electric mobility, automated production machines, and telematics software. They are using the capabilities of SMRE to build their own robots for autonomous battery production lines at Kokam and to enter the e-mobility market.

E Mobility

With extensive R&D, solar, and battery capability, SolarEdge sees itself as being well positioned to be competitive in the e-mobility market. E-mobility is expected to grow at over 30% CAGR to 2030, with the fundamentals transport systems being battery capability (storage, cost, and power output) and powertrains (efficiency and cost). To win in batteries, a manufacturer will need vast scale with technical supremacy. SolarEdge is already the largest inverter manufacturer in the world. They are at the point of sale for more opportunities for battery commercial and residential installations than anyone else.

They have already built extensive R&D capabilities that have seen them become the market leaders in PV and inverter innovation. It makes a lot of sense to apply these capabilities to batteries and furthermore to e-mobility batteries. It is the cost of batteries that prevents mass adoption of electric vehicles (EVs). Today, EVs often cost $12,000 USD more to produce than comparable internal combustion engine vehicles with the biggest contributor to this difference being battery cost (Baik, et al, 2019). SolarEdge appears to be tackling this problem by beginning battery production in a market where it’s already viable, commercial on-site storage, and then rolling out to residential and EV applications. In applying the same R&D capability that allowed them to maintain margins whilst lowering the cost of PV panels and inverters, they have the potential to unlock massive latent demand for battery applications in homes and EVs.

Right Time - Commercial & Residential Battery Storage

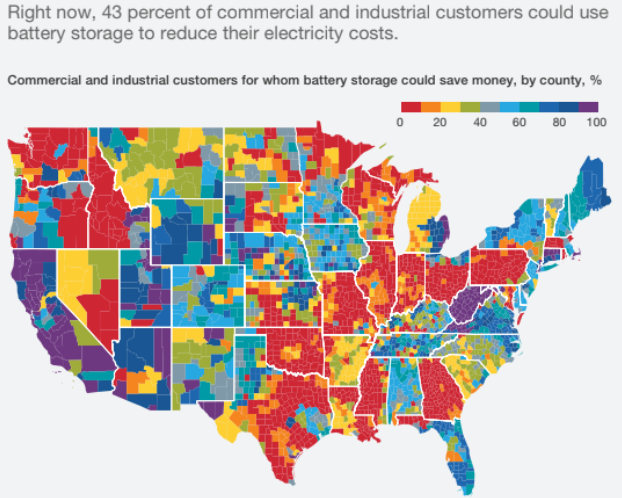

Economics for battery installation has become viable in some applications. McKinsey estimate that as of June 2017, 43% of commercial and industrial usage applications in the US were economically viable, as shown in Figure Two below.

Figure Two. Viability of battery storage in commercial and industrial usage application USA (McKinsey Research, June 2017).

Virtual Grid

There’s a lot of sense in SolarEdge creating a virtual grid solution. As the world’s largest inverter manufacturer, no one else has the ability to connect more inverters together than they do. With the move into storage solutions a SolarEdge virtual grid becomes even more compelling.

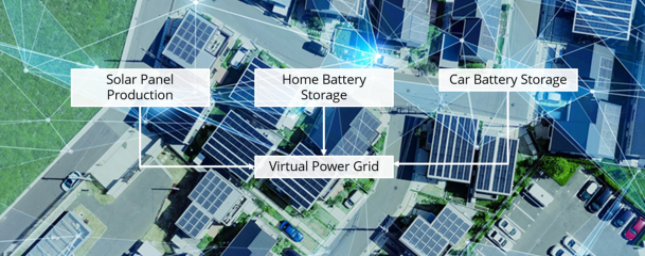

Figure 3. SEDGE connection of PV panels, battery storage and EV storage into a virtual grid.

As shown in figure 3, SolarEdge is moving towards connecting various supplies of production and storage into a virtual grid solution. In Q2 FY19 over 1 million solar systems were monitored on their portal with Q2 FY19 seeing 115,000 systems added. The first virtual trial grid solution is expected to be in place sometime around the end of 2020 and to be offered to the market in 2021.

Self Funding

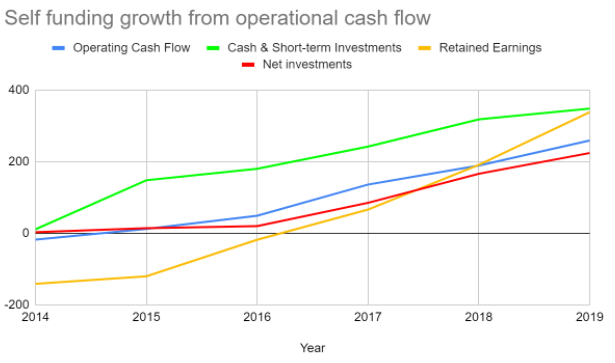

SolarEdge has no debt and funds its growth through its own cash flows. Net investing cash flows including the purchase of Kokam and building the new battery factory was only $224m in FY19, while operating cash flows were $259m.

Chart 5 . Net investing cash flow relative to operating cash flow, cash & short-term investments and retained earnings.

Chart 5 shows the conservative nature of capitalisation at SolarEdge. Net investments is less than cash flow from operations while the company has significant cash reserves and is building retained earnings.

Valuation

At Blue Oceans Capital our valuation of SolarEdge as of the recent July quarter update comes in at a conservative $220, right on fair value at current market prices.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

References

Australian PV Institute, June 2019. Australian" rel="nofollow noopener" target="_blank" data-event-type="click" data-event="link_click">(VIEW LINK) PV market since April 2001.

Australian Energy Market Operator, 2019. Data Dashboard.

Baik, Y., Hensley, R., Hertzke, P., Knupfer, S., March 2019. Making electric vehicles profitable. McKinsey Research.

Lazard Levelised Cost of Energy Analysis, November 2018.

PV Magazine, April 6 2020. “World now has 583.5 GW of operational PV.”

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

As investors, we have tremendous power to create change. Business enables evolution but investors enable business. Blue Oceans Capital exists to drive investment into sustainable companies and to make a difference.

........

All statements made in this article are made in good faith and we believe they are accurate and reliable. Blue Oceans does not give any warranty as to the accuracy, reliability or completeness of information that is contained in this article, except in so far as any liability under statute cannot be excluded. Blue Oceans, its directors, employees and their representatives do not accept any liability for any error or omission in this article or for any resulting loss or damage suffered by the recipient or any other person. Unless otherwise specified, copyright of information providedin this article is owned by Blue Oceans. You may not alter or modify this information in any way, including the removal of this copyright notice.

As investors, we have tremendous power to create change. Business enables evolution but investors enable business. Blue Oceans Capital exists to drive investment into sustainable companies and to make a difference.

Expertise

As investors, we have tremendous power to create change. Business enables evolution but investors enable business. Blue Oceans Capital exists to drive investment into sustainable companies and to make a difference.

Expertise

Comments

Comments

Sign In or Join Free to comment