Strategic Retreat?

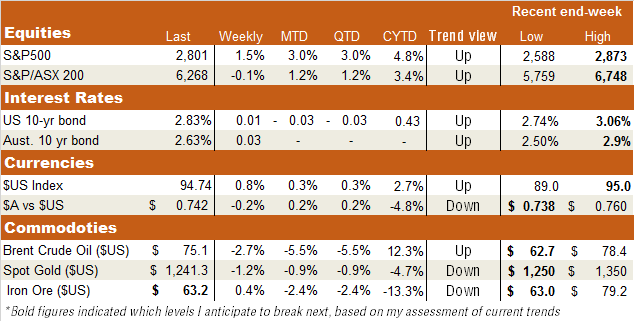

The key highlight across global markets last week was the fact that Wall Street simply shrugged in the face of an escalation of the trade wars. As noted last week, Wall Street rallied on the day America’s first instalment of tariffs on $US50 billion of Chinese imports came into effect, which China retaliated against with tariffs of its own. But Wall Street then shrugged last week when Trump announced he may impose tariffs on a further $US200 billion of Chinese imports due to China’s retaliation.

Why? Interestingly, so far at least, China has not threatened to retaliate as strenuously this time around. What’s more, US Treasury Secretary Mnuchin suggests the Administration was still ready to talk if China were open to it. One scenario is that China might simply have decided to take the current round of tariffs on the chin and not escalate matters further – after all, even a 10% tax on half its imports into the US would likely be manageable. China might then simply refuse to negotiate on trade-opening talks and see if Trump alone ups the ante (even in the face of an increasing backlash against China’s new restrictions on key US exports such as soybeans). By not retaliating, China could be aiming to take the oxygen out of Trump’s attacks. As wars go, it’s a bit like the Russians retreating in the face of Napoleon’s advance, leaving the French no-one to fight – and ultimately cold, hungry and far from home.

Either way, another major reason Wall Street has remained upbeat is its increasing focus on the Q2 earnings reporting season, which again promises to be good given America’s strong economy and recent tax cuts. All up, the S&P 500 is now only 2.5% off its highs earlier this year. The risk-on environment saw the $US also firm which in turn saw gold test below important support around $US1,250 per ounce.

Having been something of a safe-haven Asian equity trade in recent weeks, the S&P/ASX 200 was steadier last week as global markets recovered. Local economic data remained encouraging, with key business and consumer sentiment reports (perhaps surprisingly) holding up rather well.

Week Ahead

Barring another iteration in the US-China trade war, market focus will be the gradual roll out of US earnings results. Another focus will be Congressional testimony by Fed chairman Powell, who is likely to affirm his optimistic view on the economy and intent to continue gradually lifting US rates. At face value, the news flow should remain supportive of stocks and the $US.

Closer to home, China releases its monthly “data dump” today, which should show a further moderate slowdown in growth on the back of recent tightening in credit growth. Is the economy slowing too far too fast? Maybe, but unlikely. Either way, we’ll likely never know as China will only reveal through its statistics what it wants us to see.

In Australia, the June labour market report on Thursday should show underlying employment growth remains firm, albeit somewhat slower than the super charged pace of last year. Critical to the direction in local official rates remains the unemployment rate, which edged down to 5.4% last month. If it can keep grinding lower, the RBA could lift rates by early next year -whereas a move back up toward 6% would have the RBA under pressure to cut interest rates again. My base case view remains that the unemployment rate will likely hover around the mid-5% level for some time, leaving rates on hold until at least H2’19.

Have a Great Week!

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets