Tax Time: What You Need to Know About Capital Gains Tax and Shares

Michael Gable

Fairmont Equities

With the end of financial year around the corner, it is worthwhile reviewing how your gains or losses are treated if you decide to sell your shares before 30 June.

Most investors are aware of what to do with gains on shares that were held for only a brief period of time, but investors who have held shares for many years should be aware of how the gains are taxed.

Any profits which you receive from the sale of your shares will be taxed as a CGT (capital gains tax) event. This means that if you have sold the shares for more than you bought them, they will be subjected to tax as the tax office will consider this as Capital Gains Tax event.

Company dividends will also be taxed as income but you will receive a credit on the tax the company has already paid. We have previously written up an article on the imputation credits in our blog.

The biggest difference of how tax is treated with shares is how long you have held them and when you purchased them.

Please be advised that you should treat this information as a guide only and we recommend that you speak to a tax specialist as well.

Below are the different scenarios to be aware of:

- Owned Shares pre- 20 September 1985: You don’t need to pay tax

- Held shares for less than 12 months: No discount is allowed to reduce tax paid. Sale proceeds are subtracted from the purchase price.

- Held Shares for more than 12 months:

You can use two methods. The discount method and the indexation method. Choose the method which produces the least capital gain to minimise the tax you need to pay.

The discount method

You can reduce your capital gains by:

- 50% for individuals, partners in partnerships and trust

- 33 1/3% for Super Funds

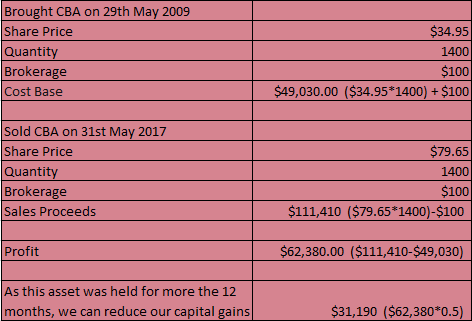

Please see below the calculation of the discount method of a sale of CBA shares which were held for more than 12 months. This tax payer will only need to declare $31,190 as her capital gain as opposed to her entire profit of $62,380 as she receives the 50% discount.

Example:

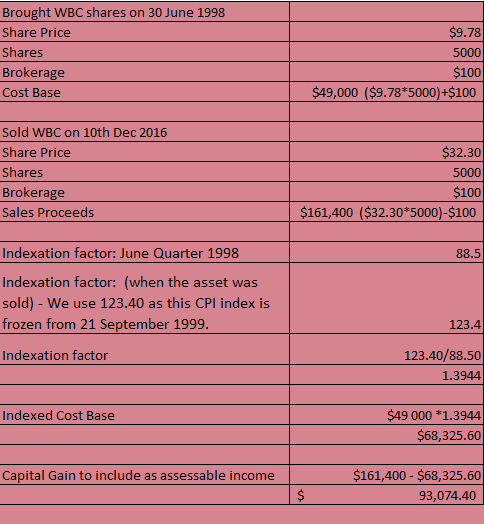

The Indexation Method:

You can use this method if you have acquired assets on or after 20 September 1985 and before 21 September 1999 and you held the asset for more than 12 months. Use this method if it gives you a better outcome than the discount method. This method allows you to increase your cost base by applying the indexation factor which minimises your capital gain by reducing the tax payable.

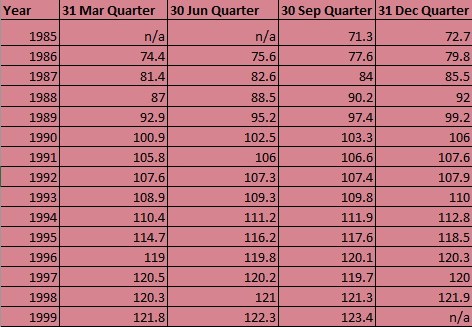

CPI Table from 30 September 1985 – 30 September 1999

Indexation Example:

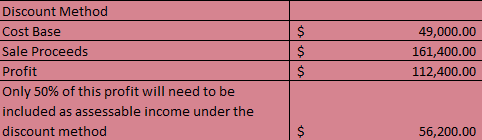

If we use the discount method the outcome would be better for the tax payer as the amount to be included as assessable income is lower.

Capital Losses:

Taxpayers can use capital losses on shares to offset capital gains in the same financial year. For example, if you made $100,000 from Company Yellow shares but then lost $40,000 from Company Red, you made a total profit of $60,000. If you held these shares for less than 12 months, then the entire $60,000 amount will be included as assessable income. If you held these shares for more than 12 months, then the 50% discount will apply and you will only need to pay capital gains tax on $30,000.

If there are no capital losses in the relevant financial year these losses can be carried forward in later years to offset capital gains.

You cannot use capital losses on shares to offset your current taxable income.

Any advice is general only. Fairmont Equities uniquely combines both fundamental and technical analysis. Visit our website for a free trial to our research, request a free portfolio review, and to access our free blog and educational videos.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael Gable is managing director of Fairmont Equities. We are a small boutique advisory that uniquely combines both fundamental and technical analysis. As a result, our analysis is featured regularly in the finance media such as the Australian Financial Review, and Sky News Business.

Fairmont Equities provides portfolio management services and also produces weekly investment and trading ideas.

Sign up to our weekly newsletter containing stock tips and educational articles. Head to www.fairmontequities.com and leave your email to sign up now.

2 topics

Michael Gable

Managing Director

Fairmont Equities

Michael Gable is managing director of Fairmont Equities. We are a small boutique advisory that uniquely combines both fundamental and technical analysis. As a result, our analysis is featured regularly in the finance media such as the Australian...

Expertise

No areas of expertise

Michael Gable

Managing Director

Fairmont Equities

Michael Gable is managing director of Fairmont Equities. We are a small boutique advisory that uniquely combines both fundamental and technical analysis. As a result, our analysis is featured regularly in the finance media such as the Australian...

Expertise

No areas of expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

How to invest $100k for growth

Livewire Markets