Telstra struggles on earnings result – market drifts lower

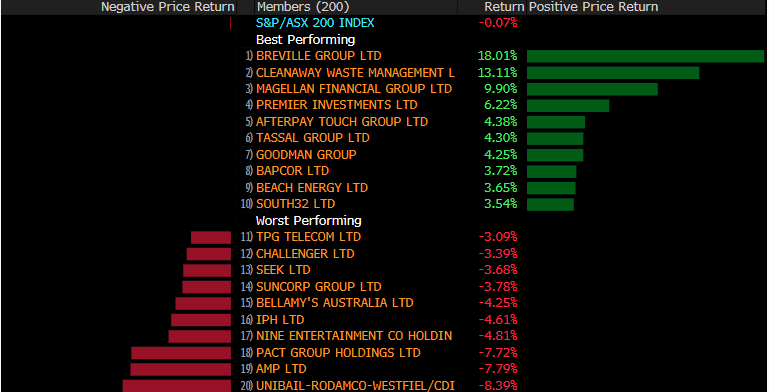

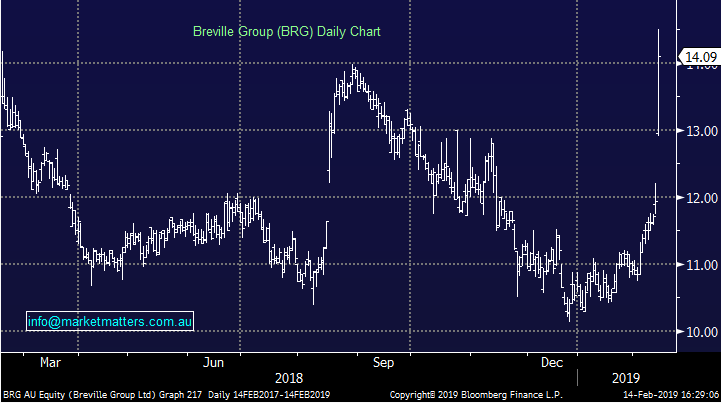

Volatility at the stock level was alive and well today with some big swings in companies that reported results….Breville (ASX:BRG) a cracking set of numbers and the stock reacted accordingly while the woes at AMP continue. Nothing to like about the stock here and a classic example of the old saying - you know what you get trying to pick bottoms! The stock down ~8% tells the story.

Babcor (ASX:BAP) rebounded after yesterday’s selloff while AfterPay (ASX:APT) added another +4.38% to close at $18.36 – up $2 since I suggested it was a sell on Livewire!

Big moves under the hood today

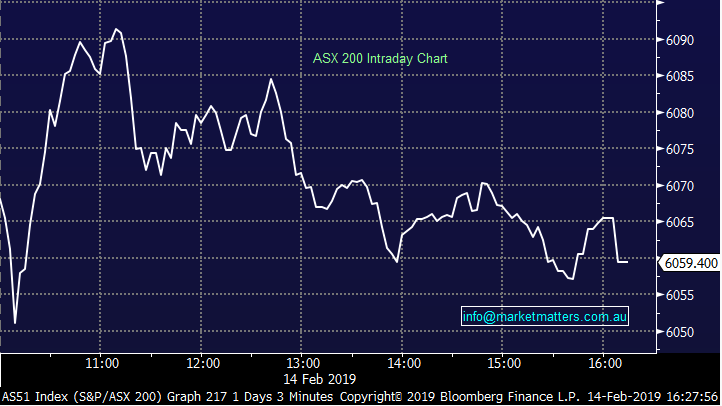

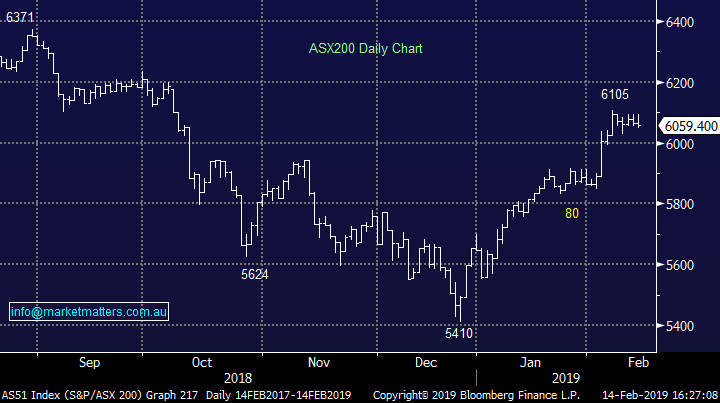

There was a broad cross section of results out today and we’ve attempted to provide a quick snapshot on most. From a broader markets perspective, the index continues to look tired trading to an intra-session high today of 6093 before succumbing to selling, closing near to lows at 6059.

Overall, the ASX 200 closed down -4points or -0.07% to 6059. Dow Futures are currently trading up +36pts or +0.14%

ASX 200 Chart

ASX 200 Chart

CATCHING OUR EYE

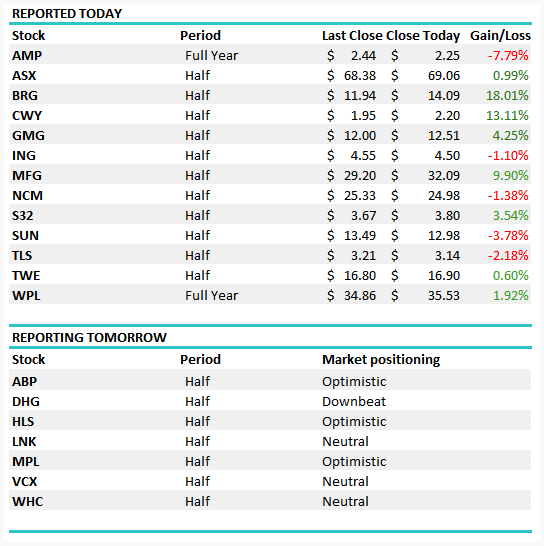

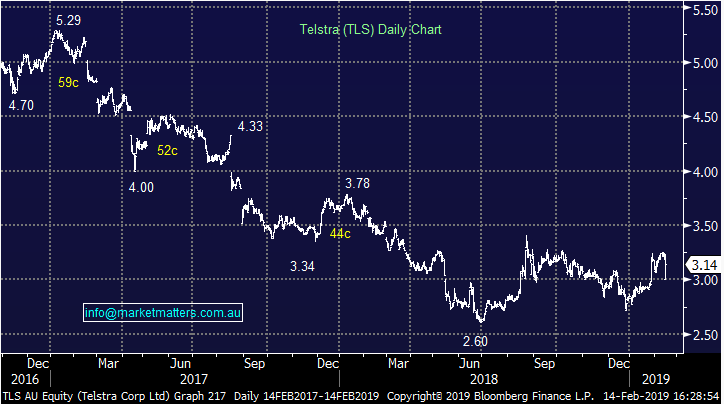

Reporting; A huge day on the reporting front with Telstra (ASX:TLS) headlining the card although there was a good cross section of companies out with numbers. Telstra had a volatile day, prices will show a low of $3.00 however that was a tiny order through Chi-X that shouldn’t have traded by the look – the true daily range was $3.075 to $3.23 with the SP ticking around with Andy Penn commentary. Harry covers the result in more detail below (along with Breville) however I thought it looked okay, slightly light on in terms of free cash flow given they’re spending more for future growth but nothing that concerned me in the numbers.

South32 (ASX:S32) +3.54% traded higher following their 1H results – underlying net profit after tax of $642m which compares well to consensus of $604.5m. Revenue was pretty much inline however they announced a large capital management program which the market liked . That included an interim dividend of $0.051/share + special dividend of $0.017/share making for US22c at the HY mark, plus the buy-back has been ticking over in the background. Total outlay of US$344m with a further US$167m in the share buyback during the period. They confirmed guidance with the groups production volumes expected to rise by +5% in FY19, or +7% on a per share basis given the share buy backs underway. A good result all round from S32

Suncorp (ASX:SUN) -3.78% came out with cash earnings of $413m which was above market expectations of $406m, however they guided to higher regulatory costs going forward (offset partially by cost cuts). While the General Insurance business was hurt from weather events, the actual underlying result was good. The bank component of the result was weak with little loan growth and a declining net interest margin. The sale of the life business is expected to settle at the end of the month with $600m in capital to be returned to shareholders. Some of this could be in the form of a special dividend which may result in the total FY19 dividend being as large as FY18 at 85 cps. In short, insurance division on the up while the bank is treading water at best.

Woodside (ASX:WPL) +1.92% popped today on a bigger dividend which the market liked, however it’s probably not sustainable at that level. From an earnings perspective, underlying core NPAT came in at US$1,416m which was a tad below consensus of US$1,459m. A few smaller bits and bobs led to the miss however it was the final dividend of US$1.44 fully franked that was the standout. WPL guide to an 80% payout ratio and that dividend was equivalent to a 95% payout ratio, so why the deviation? They say it’s a result of strong cash earnings during a period of Oil Price strength plus operationally they had a good period. I doubt this will be sustained however its nice when it comes. We’ve been looking to add WPL to the Income Portfolio recently, but alas, the stock has run!

The exchange operator ASX added nearly 1% today after coming printing results broadly inline with expectations – while I’m light on details here, cash NPAT was $246.1m slightly below consensus but there was an accounting change that seemed to be the reason. Hard to get excited on 26.45x and 3.5% yield however it’s certainly a consistent business.

Today’s result in Healthscope (ASX:HSO) had been pre-released, with group EBITDA up +7.7% YoY while underlying NPAT was up 3% at $74.6m. The takeover remains in play for HSO and that’s the driver for now. HSO closed flat

Goodman (ASX:GMG) +4.25% keeps on performing – no wonder he’s got every sort of vehicle in the parking lot downstairs…todays result was a beat with1H19 Operating profit up 10.4% on pcp to $465m vs. expectations of $430m while the divi had been pre-announced at 15cps. They upgraded guidance and now expect EPS of 51.1¢, or growth of +9.5% - no change to FY19 DPS guidance of 30.0¢. A great result and stock ran another +4.25%

Telstra (ASX: TLS) -2.18%; It’s not a shocking result for Telstra, particularly after many periods of profit downgrades but many of the current holders are here for the div and that disappointed. For the 6 months, net profit was $1.2b, down over 25% from the first half of 2018, while revenue saw a more muted fall of ~2% to $12.6b in the half. Despite the sizable fall on the previous year’s first half, the results are broadly in line with guidance, and with what the market was expecting. For the first time in a while, dividend guidance was not given to the market. Telstra announced an 8c div, comprising of 5c interim and a 3c special, that was down from the 11c first half div from last year and missed some market expectations.

The implied 16c full year DPS had TLS on a sub 5% yield as at yesterday’s close price – not enough for the income investors and the reason for much of the stocks fall today. At $3.14, TLS moves to a 5.1% FF yield, more palatable but clearly down on prior periods.

Telstra (ASX: TLS) Chart

Breville Group (ASX: BRG) +18.01%; Breville has burst out of the gates today to rally to new all-time highs following an impressive first half report. The homeware distributor saw strong growth in the first half on the previous comparable period, with adjusted net profit after tax (NPAT) up 14.8% beating the streets expectations driven by some impressive revenue growth.

Successful expansion into Germany and Austria helped boost the result, with European sales up over 30%. Coffee was also big driver of growth as global consumption soars. The company continues to perform where other retailers can’t in the tough macro environment. A quality retailer that is executing well in the things they can control. Guidance for the full year is for EBIT growth “to be slightly higher than the market’s current consensus of ~11%,” hard to interpret that as anything but a beat. Technically the close above $14 look a break out as the stock charters new territory at all-time highs.

Breville (ASX: BRG) Chart

Broker Moves

- BHP Downgraded to Hold at Morgans Financial; PT A$40.38

- Newcrest Downgraded to Reduce at Morgans Financial; PT A$22.21

- Origin Energy Rated New Hold at Deutsche Bank; PT A$7.70

- Woodside Rated New Hold at Deutsche Bank; PT A$33.80

- Santos Rated New Buy at Deutsche Bank; PT A$7.60

- Oil Search Rated New Buy at Deutsche Bank; PT A$9

- Macquarie Group Downgraded to Hold at Morningstar

- Iluka Downgraded to Hold at Morningstar

- Breville Downgraded to Sell at Morningstar

- OceanaGold Upgraded to Buy at PI Financial; PT C$5.40

- Yancoal Australia Rated New Buy at BOC Intl

- Virgin Australia Cut to Underperform at Credit Suisse; PT A$0.18

- Bapcor Upgraded to Add at Morgans Financial; PT A$6.54

Never miss an update

Stay up to date with the latest news from Market Matters by hitting the 'follow' button below and you'll be notified every time I post a wire.

Market Matters publishes daily market reports and sends SMS alerts when we transact on our portfolio. To get our latest market views and hear when we take new positions, trial Market Matters for 14 days at no cost by clicking here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

5 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management