The 10 best and worst performers of August

The recent whipsaw of capital back towards higher growth / higher valuation businesses has been most evident across the more growth-heavy small and mid-cap equities space, particularly following significant contributions from companies within the emerging technology and IT sectors.

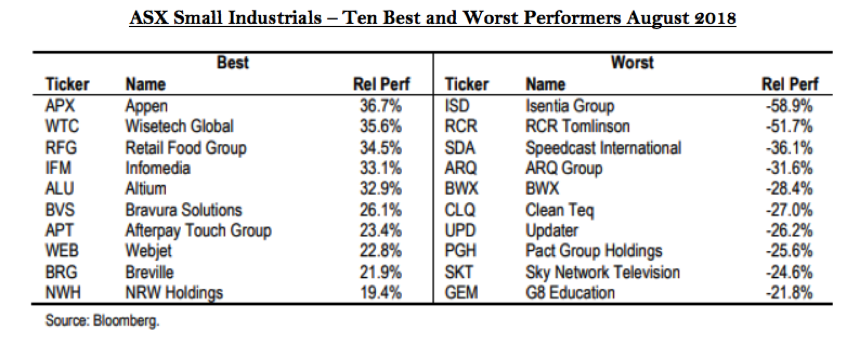

While the ASX Small Ordinaries delivered a total index return of +2.49% for August, a large proportion of this return came as a result of a +17% contribution from the information technology sector alone. Indeed, just four companies were ultimately responsible for 60% of the total monthly return of the entire ASX Small Ordinaries Index in August: Altium (ALU), Afterpay (APT), Appen (APX) and Wisetech (WTC).

Historically, these kinds of aggressive moves tend to reflect shorter-term market positioning rather any significant underlying change in the fundamental outlook, and we would caution against expecting future valuation uplifts in response to similar earnings outcomes.

While growth businesses have delivered some outstanding returns over the past 18 months, there had been an obvious internal market rotation away from the sector in recent months as capital was recycled into lower-quality businesses that screened as relatively cheap versus the underlying market

Similarly, broader cash holdings across domestic fund managers had appeared to grow elevated versus their historical averages (a combination of broader macro concerns e.g. escalating global trade tensions and weakness across emerging markets alongside the anticipation of pending share price volatility through results season), whilst short positions across higher-growth company names had also begun to materially increase.

As a result, while the market had been positioned for some retracement in fortunes across the growth sector (and for a re-rate in lower-quality, value-type businesses) various corners of the investment community were instead forced back into the market to aggressively purchase shares in a number of companies that had already taken on a rapid ascent.

Of the above factors, it’s most likely the race to cover outstanding short positions provided the most meaningful amount of fuel to the fire. In the final week of reporting season, for example, stocks with an outstanding short interest of more than 5% of the company (and a days-to-cover ratio in excess of 30 days) outperformed the underlying ASX 200 index return by some +6.8%.

Significant share price falls

Of course, not all share price moves this month were weighted to the upside, with a number of equally spectacular share price falls experienced by those companies unable to meet overly optimistic consensus forecasts.

Momentum essentially works both ways and while the market rushed this month to support those businesses that displayed an ability to generate meaningful earnings growth, it has been equally prepared to flee those companies that were unable to meet expectations.

Interestingly (or, perhaps, frustratingly for those positioned for the broader recovery in value names), a large number of the more stellar share price declines this month came from businesses that one would most likely attribute to the value-end of the market.

Ultimately, one purchases shares in lower-quality businesses in the belief that the price paid doesn’t adequately reflect the ability of that business to generate a certain amount of future cash flows over time. Of course, in the event that these businesses don’t see an improvement in their outlook, then the valuation discount will remain in place (or, as was the case this month, de-rate to previous levels).

A number of notable moves in this camp included:

- Isentia Group (ISD, -58.9%),

- Speedcast International (SDA, -36.1%),

- ARQ Group (ARQ, -31.6%) and

- Pact Group (PGH, -25.6%).

Indeed, of the top ten worst industrial performers this month across the ASX Small Ordinaries, seven were businesses that one would classify as value stocks.

In terms of broader trends, overall earnings ‘beats’ outnumbered the total ‘misses’ over the period (albeit marginally), although forward-looking guidance, in aggregate, was surprisingly softer than initial market expectations.

As a result, net consensus earnings estimates for FY19 across the ASX 200 ended the month lower than where they started (and by quite some margin: almost three companies saw consensus forward estimates downgraded for every one that experienced a positive revision).

Average earnings per share growth across the Australian market for FY18 will likely settle in the ~8% range, with FY19 estimates now indicating a growth rate slightly below that.

The road ahead

Looking forward, despite an incredible deluge of company data, management meetings and follow-up analysis, our overall view on broader market direction and the opportunities from here remain much the same as when we entered the results period.

With low global interest rates and domestic economic growth rates that continue to remain relatively subdued, businesses that are showing an ability to deliver strong earnings growth rates - regardless of the cycle - will continue to command strong valuation premiums.

While we expect defensive growth businesses to continue to find long-term market support, we are cautious of the level of momentum ingrained in a number of these businesses, particularly where valuations are already reflecting significant upside (and faultless management execution) for many future years ahead

Our general expectation for the remainder of the year is for continued equity market volatility (in addition to a further round of corporate activity / capital raisings) and it will be important to ensure we have sufficient capital available to take advantage of any opportunities as they present.

This is an excerpt from the August 2018 Ophir letter to Investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

10 stocks mentioned

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment