The 2019 Berkshire Hathaway Letter to Investors

Clime Investment Management

Clime Investment Management

In prior years, when we have reviewed Warren Buffett’s annual letter to shareholders, we have noted the unique structure of Berkshire Hathaway (“Berkshire”) and stressed its importance in facilitating the self-funding of its growth.

Berkshire is akin to a “mutual” investment company that has passive minority investments and a few fully owned operating subsidiaries. Whilst Berkshire has hundreds of thousands of shareholders, the company does not declare dividends. All profits made by its insurance subsidiaries are retained in insurance reserves and accessible for investment across the Group. Further, all dividends and income received by Berkshire on its investment portfolio are retained for reinvestment. The structure is unique and it allows the company to benefit from the powerful investment force of compounding. To quote Buffett –

“Our level of equity capital is a different story: Berkshire’s $349 billion is unmatched in corporate America. By retaining all earnings for a very long time, and allowing compound interest to work its magic, we have amassed funds that have enabled us to purchase and develop the valuable groves earlier described. Had we instead followed a 100% payout policy, we would still be working with the $22 million with which we began fiscal 1965.”

The operating subsidiaries, particularly the insurance operations, are the main generators of liquid investment capital. The “free float” that Buffett often refers to are the prepaid or unearned premiums received by these insurance companies. These premiums are received before the insurance liability is extinguished. Therefore, Berkshire has abundant short term liquidity and it generates abundant long term capital that need not be serviced by payment of dividends or returned as capital to shareholders. Berkshire does maintain a buyback authority but it is seldom utilised as the shares trade above the declared line in the sand for the buyback to occur.

The ability to access liquidity at times of economic distress or market dislocation is the “unfair” advantage that Berkshire has created for its shareholders. However, it is the enduring capacity of its management to be patient and logical in their investment approach that converts this unfair advantage into an extraordinary investment mechanism unrivalled in the world today.

“Before we look more closely at the first four groves, let me remind you of our prime goal in the deployment of your capital: to buy ably-managed businesses, in whole or part, that possess favorable and durable economic characteristics. We also need to make these purchases at sensible prices.”

Berkshire letter 2019

Charlie Munger and Warren Buffett

Looking forward, it is hoped that both the business and the investment approach endures past the lives of both Warren Buffett and Charlie Munger. That must be a fundamental belief of their shareholders in their investment in Berkshire Hathaway. Having noted that, we have a growing suspicion that the policy of not paying dividends will soon come to an end.

Why do we suggest this? There are hints that Berkshire is becoming too large and that value-based business acquisitions are becoming more difficult for Buffett and Munger to find in a world inflated by ultra-loose monetary conditions.

“In the years ahead, we hope to move much of our excess liquidity into businesses that Berkshire will permanently own. The immediate prospects for that, however, are not good: Prices are sky-high for businesses possessing decent long-term prospects. That disappointing reality means that 2019 will likely see us again expanding our holdings of marketable equities. We continue, nevertheless, to hope for an elephant-sized acquisition. Even at our ages of 88 and 95 – I’m the young one – that prospect is what causes my heart and Charlie’s to beat faster. (Just writing about the possibility of a huge purchase has caused my pulse rate to soar.)”

Berkshire letter 2019

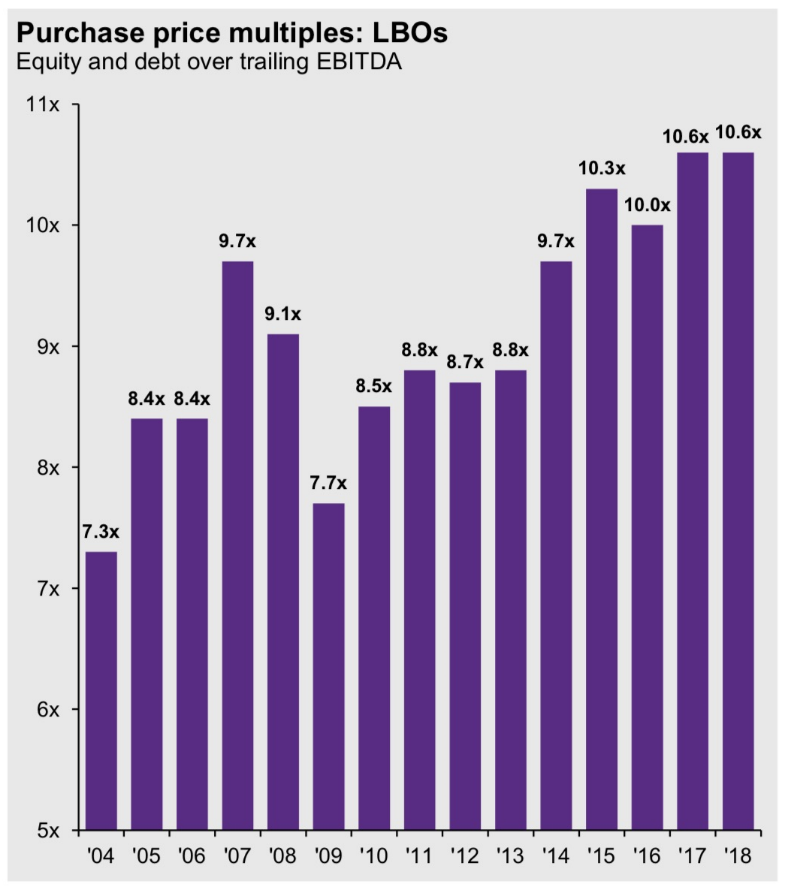

Figure 3. Large acquisitions in US: prices steadily rising

Source: JP Morgan Asset Management

The four-legged dog

“Abraham Lincoln once posed the question: “If you call a dog’s tail a leg, how many legs does it have?” and then answered his own query: “Four, because calling a tail a leg doesn’t make it one.” Abe would have felt lonely on Wall Street.”

… Berkshires 2019 letter

Compared to recent letters, this year’s was quite scant on insights but the reference to Abraham Lincoln’s famous anecdote was both timely and pointed in this era of fake news and bloated promises made by political and business leaders alike. The facades often on show in Wall Street are a constant “bone of contention” for Buffett.

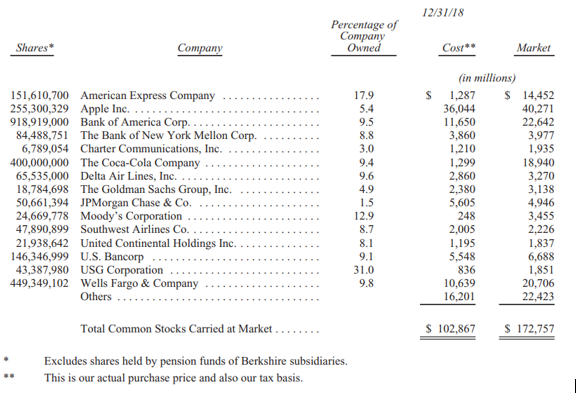

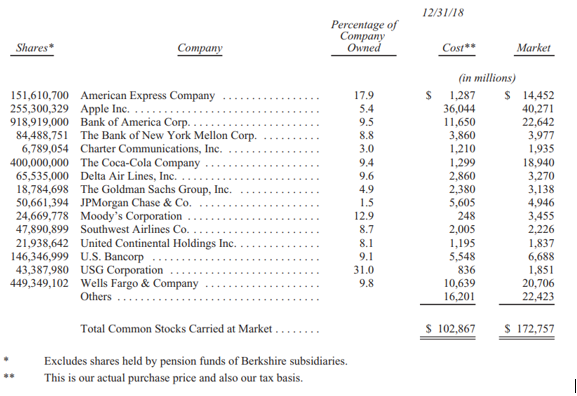

The letter contained the usual factual tables updating the investment portfolio and the rolling year investment returns. However this year Buffett had little to describe with regard to significant portfolio changes or the reasons supporting major acquisitions.

While the Berkshire portfolio has always been remarkably stable with limited changes in major holdings, it is clear that 2018 was not a fertile year for value investing.

Indeed 2018 was marked by an investment “hiccup” that the above table does not capture. Berkshire’s large investment in Kraft Heinz is part of a control group (a consortium), so it must carry this investment on its balance sheet at a GAAP figure. This amount (or value) was reduced in 2018 by their share of the large write-off of intangible assets taken by Kraft Heinz. At year-end, the Kraft Heinz holding had a market value reduced by over $4 billion to $14 billion on a cost basis of $9.8 billion. Most of this fall happened in a mere 24 hours following the Kraft Heinz disclosure.

Kraft Heinz – underinvested in the brands?

Buffett noted that wild swings in the daily market value of Berkshire’s investments was now quite common and he, therefore, warned his shareholders that they should not take much notice of quarterly reporting.

“Wide swings in our quarterly GAAP earnings will inevitably continue. That’s because our huge equity portfolio – valued at nearly $173 billion at the end of 2018 – will often experience one-day price fluctuations of $2 billion or more, all of which the new rule says must be dropped immediately to our bottom line. Indeed, in the fourth quarter, a period of high volatility in stock prices, we experienced several days with a “profit” or “loss” of more than $4 billion. Our advice? Focus on operating earnings, paying little attention to gains or losses of any variety. My saying that in no way diminishes the importance of our investments to Berkshire. Over time, Charlie and I expect them to deliver substantial gains, albeit with highly irregular timing”

Two important comments from Buffett

As Australia enters an election campaign, which may well be dominated by a ferocious tax debate, the Buffett letter contained an interesting take on taxation. The Trump tax cuts were put into an interesting perspective.

Buffett wrote –

“Begin with an economic reality: Like it or not, the U.S. Government “owns” an interest in Berkshire’s earnings of a size determined by Congress. In effect, our country’s Treasury Department holds a special class of our stock – call this holding the AA shares – that receives large “dividends” (that is, tax payments) from Berkshire. In 2017, as in many years before, the corporate tax rate was 35%, which meant that the Treasury was doing very well with its AA shares. Indeed, the Treasury’s “stock,” which was paying nothing when we took over in 1965, had evolved into a holding that delivered billions of dollars annually to the federal government. Last year, however, 40% of the government’s “ownership” (14/35ths) was returned to Berkshire – free of charge – when the corporate tax rate was reduced to 21%. Consequently, our “A” and “B” shareholders received a major boost in the earnings attributable to their shares.”

We wonder what Buffett would make of the franking debate in Australia and whether he would agree that the Australian franking system was a good idea when it was conceived? It seems to us that Buffett believes that corporate America should contribute to the financing of essential services provided by Government to society. Thus, he has no qualms about Berkshire paying tax rather than paying dividends to shareholders.

That is not to say the Buffett is keen to pay tax before it is due. He regards the deferment of tax as a “free loan” from the government. In other words, an investor should refrain from crystallising investments that are performing if tax will be paid when the investor’s capital comes back as cash.

To quote from the letter –

“As I indicated earlier, about $14.7 billion of our $50.5 billion of deferred taxes arises from the unrealized gains in our equity holdings. These liabilities are accrued in our financial statements at the current 21% corporate tax rate but will be paid at the rates prevailing when our investments are sold. Between now and then, we in effect have an interest-free “loan” that allows us to have more money working for us in equities than would otherwise be the case.”

Finally, and most contentiously given our concerns with US government debt that is ballooning under the Trump administration, Buffett notes that US debt has not slowed economic progress and prosperity. Investing in US stocks, maintaining the focus on them and not being diverted into panic during periodic financial crises, has produced an extraordinary outcome.

“Those who regularly preach doom because of government budget deficits (as I regularly did myself for many years) might note that our country’s national debt has increased roughly 400-fold during the last of my 77-year periods. That’s 40,000%! Suppose you had foreseen this increase and panicked at the prospect of runaway deficits and a worthless currency. To “protect” yourself, you might have eschewed stocks and opted instead to buy 31⁄4 ounces of gold with your $114.75. And what would that supposed protection have delivered? You would now have an asset worth about $4,200, less than 1% of what would have been realized from a simple unmanaged investment in American business. The magical metal was no match for the American mettle. Our country’s almost unbelievable prosperity has been gained in a bipartisan manner. Since 1942, we have had seven Republican presidents and seven Democrats. In the years they served, the country contended at various times with a long period of viral inflation, a 21% prime rate, several controversial and costly wars, the resignation of a president, a pervasive collapse in home values, a paralyzing financial panic and a host of other problems. All engendered scary headlines; all are now history”

However, it is our view that the blow out in US government debt is quite distinct from the growth in total debt across the US economy. Last night it was revealed by the US Treasury that the US budget deficit widened to $310 billion in the first four months of Fiscal 2019. This is 77% greater than the same period last year. This year receipts have fallen by 2% (the tax cuts) while spending has lifted by 9 per cent.

So, whilst growing debt supports growth in an economy, we would not agree that rampant debt growth that greatly exceeds GDP growth is sustainable. Indeed, we doubt whether Buffett would support Trumps tax cuts and the driving up of US Government debt.

Time will tell whether the US Federal Reserve will have to return with a QE4 program to prop up the US budget and support the inflated asset prices that Buffett laments are making value investing difficult to undertake.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

2 topics

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Comments

Comments

Sign In or Join Free to comment