TOL - 3rd Feb, 2021

The 3 most important interest rate indicators

Chris Rands

Yarra Capital Management

Typically when creating our fixed income outlook for the year we focus on the most likely scenarios to determine how interest rates could move. This year, however, the range of possible outcomes is far too wide, making it difficult to accurately forecast. While the assumption - the vaccine will work and the economy should be ready to recover - maybe be true, can we rely on it?

“What if?” scenarios

This year we adopted an alternative strategy to determine where interest rates could land in 2021. Rather than our traditional methods, we have used a decision tree to help formulate what we believe are the potential paths that the economy could take. We use this approach to break the potential paths into analysable chunks and then subsequently assign bond market outcomes. This allows us to not only create a feel for the most likely outcome, but also the range of outcomes in the event we miss the mark.

Note the analysis below only presents the results of our forecasting process. For reference to the full rationale of how we landed at these outcomes and probabilities, refer to our comprehensive outlook paper.

The decision tree

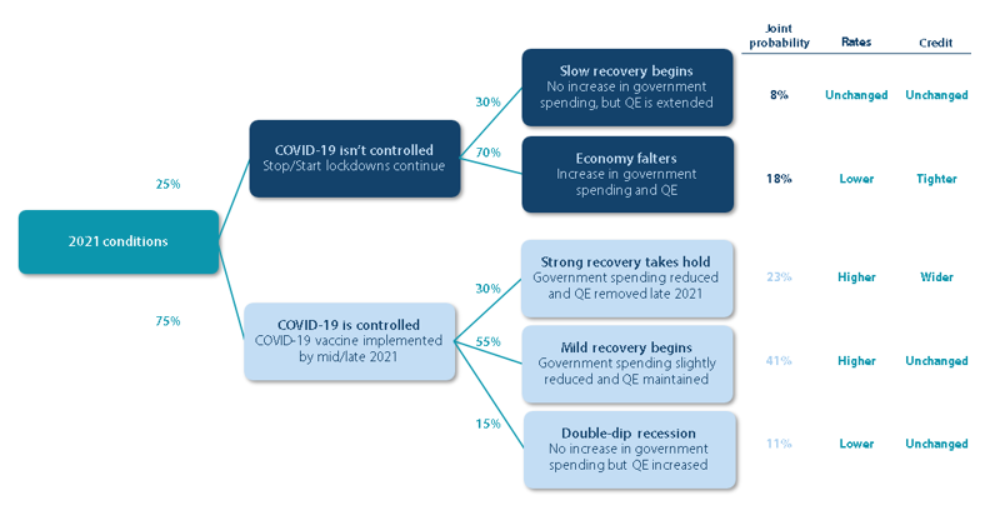

The decision tree that we created has two steps. The first step is to determine the chance that COVID-19 is controlled in Australia in 2021. The second is to determine what economic conditions could come from each environment.

With respect to ‘controlled’ in step one, we apply a loose definition that suggests COVID-19 is not eradicated completely but, rather, if a ‘December 2020 Northern Beaches’ style outbreak occurred in the second half of 2021, it would not lead to widespread quarantines and border closures.

The results of our decision tree are shown below, with the percentages shown on each line representing the subjective probability that we think that event occurs.

Figure 1 - The full decision tree

Source: Nikko AM

The most important question: Will COVID-19 be controlled?

Our decision tree starts with the COVID-19 outcome as it will be the most important for how the economy performs. It is obvious why this is so important. If the vaccine is rolled out fast enough and works effectively in Australia, then the back end of 2021 could see strong economic conditions as businesses start operating at closer to full capacity, and easy fiscal provides an incentive for businesses to invest.

Alternatively, if COVID-19 is not controlled in 2021, then small businesses will have endured almost two years of weaker operating conditions, exposing the economy to the risk of business defaults.

When determining the chance of COVID-19 being controlled in 2021, we see a flow of positive news, cautioned by questions that have yet to be answered. The arguments supporting COVID-19 being controlled in 2021 include:

- the vaccines have proven 90% effective in trials

- there have been quick approval and turnaround times globally

- one of the vaccines is being produced in Australia, and

- the Government expects to have four million doses administered by the end of March.

The downside is that a number of questions remain about whether the virus can be contained. These include:

- How long does the vaccine offering protection?

- Will the vaccine be effective against new strains of the virus?

- Will enough people voluntarily receive the vaccine to achieve herd immunity?

Our take on this information is that the early indications of COVID-19 being controlled in Australia in 2021 is positive. Under the Government’s timeline of vaccine rollout, and assuming the vaccines are 90% effective, by the end of the year a large percentage of the Australian population could have some form of protection. As such we have assigned a 75% chance to the positive outcome that COVID-19 is controlled in Australia (only) in 2021.

What does the economy look like in each scenario?

The second branch of our decision tree then focuses on how the economy would perform under each scenario. For the negative outcome—that COVID-19 is not controlled—our expectation is that we enter either a weak recovery or the economy falters and registers negligible growth.

We have not assumed a double-dip recession in this environment as we believe that in the event that COVID-19 is not contained, the RBA will continue to run extremely loose monetary policy and the Federal Government would continue to run large budget deficits.

Our view on the two outcomes listed above is that it would be more likely that businesses begin to feel the effects of a prolonged slowdown in this environment, which would set the stage for the economy to achieve minimal growth.

In the positive outcome—where COVID-19 is controlled—we expect three scenarios to potentially play out. The bulk of these outcomes is between either a mild or strong recovery taking hold, driven by strong business conditions, easy monetary policy and a strong housing market. Our expectations is that it would likely be a mild recovery, as a number of lingering concerns around debt levels, deteriorating relations with China and the reduction of government stimulus would mean the recovery is not as strong as it could be.

We also believe in this environment a double-dip recession could occur, which was not assumed when COVID-19 is not controlled. The reason for this is there is a risk with a strong recovery that monetary or fiscal policy is tightened too quickly, causing an economic shock. While we see this as low odds, it would be similar to a 2011 scenario.

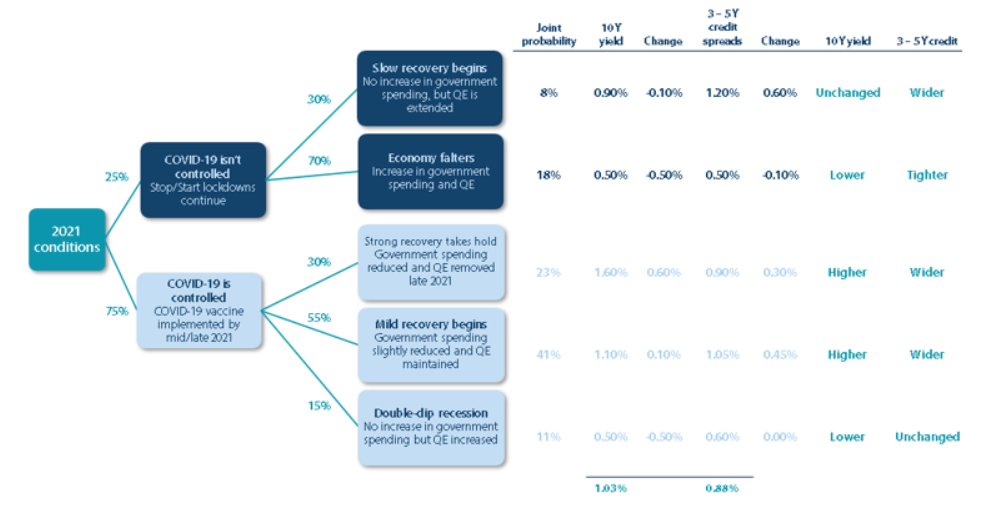

How would rates and credit perform in each scenario?

With our economic paths now defined, we assign expected interest rate and credit spread levels to each outcome. These are based off the relationship between bond yields and the cash rate, which typically trade in a defined range through the cycle. We forecast that in the event the economy is strong, interest rates rise and credit spreads sell off. In the event that the economy is weak, either because COVID-19 can’t be controlled or government support is removed too quickly, we assume interest rates rally. This gives the below outcomes for each branch of our tree.

Figure 2 - Decision tree with expected fixed income metrics

Source: Nikko AM

Using the information

While a large number of assumptions and calculations were made in our comprehensive outlook paper, we can use this decision tree to make a few comments about what the outlook for 2021 will be.

Firstly, the bulk of our probability distribution is pointing towards a mild or strong recovery beginning in 2021. This accounts for about 70% of the outcomes and relates predominantly to the fact that the news flow on the prospects of the vaccination have been promising. These outcomes bring with them higher interest rate levels, which means our most likely outcome for interest rates in 2021 will be a slight rise.

Secondly, we believe there is a moderate chance (around 30%) that either the economy slows or enters another recession. This reflects our thinking that either COVID-19 cannot be controlled or government support is removed too quickly. In these instances, we would expect interest rates to rally, and given where 10-year yields are trading (at the time of writing) it would see a drop of around 20 – 70 basis points depending on how severe the outcome.

Finally, the weighted average result of our decision tree places 10-year rates at around 1.03%. This is not far away from current market pricing and we believe it makes intuitive sense since the most likely outcome is for rates to rise, with a smaller risk of a large rally occurring if the vaccine proves ineffective (perhaps against the new strains of the COVID-19 virus).

So, the outlook at the moment is sunny with a chance of rain.

Stay one step ahead of the crowd

We don’t have to rely on picking market direction to capture returns. Instead, we look for the best relative value between securities and sectors that will deliver consistent positive returns for investors. Stay up to date with our latest insights by clicking follow below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra Capital Management in April 2021). Chris has over 9 years of experience in the fixed income market. He is also co-host of the popular Australian podcast series The Rate Debate.

Chris Rands

Co-Portfolio Manager, Fixed Income

Yarra Capital Management

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra...

Expertise

Chris Rands

Co-Portfolio Manager, Fixed Income

Yarra Capital Management

Chris is responsible for portfolio management, including portfolio construction and trading for various Australian fixed income portfolios including the Nikko AM Australian Bond Fund at Yarra Capital Management (Nikko AM was acquired by Yarra...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

2 stocks to drive future performance following a 35% return in six months

Katana Asset Management