The coming surge in Australia’s budget deficit and public debt – can we afford it?

This week would have been Federal Budget week and the Australian Treasurer would have been announcing budget surpluses. Of course, coronavirus intervened, and the surpluses rightly had to be sacrificed to support Australian households, businesses and jobs.

And it makes no sense to provide detailed budget forecasts given the extreme uncertainty about the impact on the economy and hence the budget for the coronavirus shutdown. So, the Treasurer has provided a statement to Parliament on the economic impact of the crisis, updated budget numbers will be provided in June and the Budget itself has been delayed to October.

As the economic impact of the crisis is well known I won’t go through that again here except to note two things from the Treasurer’s statement:

- First, more than 5.5 million Australian workers are now covered by the JobKeeper wage subsidy program which is coming close to the Government’s initial estimate that it would cover 6 million.

- Second, the Treasurer reiterated that the best way to pay back debt is through productivity-enhancing reforms focussed on workforce training and education, infrastructure, cutting red tape, taxation and industrial relations reform. So, reform to help the economy recover post coronavirus will likely be the key focus in the October Budget.

This wire looks at our own projections for the budget deficit, the impact on Australia’s net public debt and whether it’s affordable.

Budget deficit projections

The next table shows our rough budget deficit projections, taking the Mid-Year Economic and Fiscal Outlook projections from last December as the starting point.

Source: Australian Treasury, AMP Capital

Under “policy changes” we have allowed for the three policy support packages announced through March, the health package announced in March, various industry support packages including that for childcare and bushfire spending.

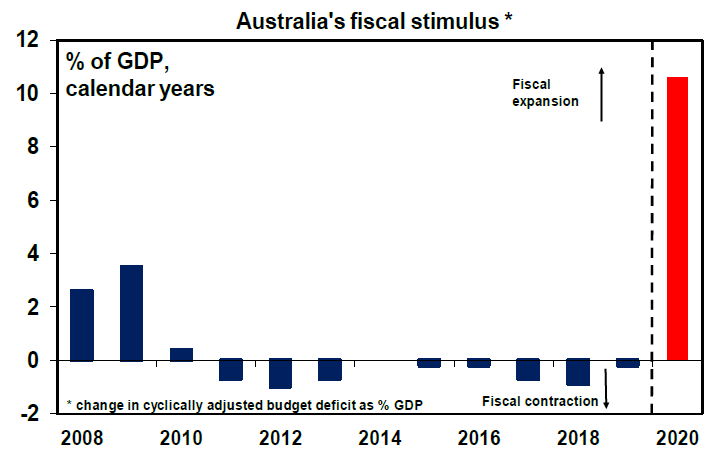

These are dominated by the $130bn JobKeeper program and are concentrated in this financial year and next, particularly for the period out to September. While the reopening of the economy may be coming a bit earlier than the Government had allowed for, we assume that the Government redirects some of the JobKeeper program from those who may no longer need it, to those who do, such that the full $130bn is still spent. In total and allowing for state fiscal stimulus this is resulting in a 10.6% of GDP fiscal stimulus for this calendar year, which swamps the stimulus seen in the GFC (and rightly so because the GFC posed a much smaller threat to the economy).

Source: IMF, AMP Capital

The hit to the economy will mean a hit to government revenue and increased spending demands under some existing spending programs and this is shown in the line called “parameter changes.” This is a guesstimate at present, because we are yet to get a firm handle on the size of the hit to the economy and how quickly it might recover. But the negative impact on the budget is likely to be bigger next financial year than this financial year because unemployment will average far more next financial year (around 8.5%) than this financial year (around 6.3%) and that provides a guide to lost Federal revenue and increased expenses.

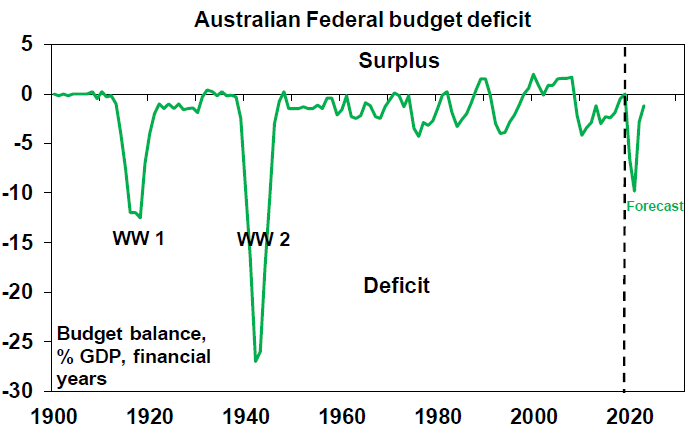

Put simply, the Government’s necessary fiscal support response and the hit to the budget flowing from the hit to the economy will see the budget deficit blow out to around $130bn this year and $200bn next financial year, before falling sharply from 2021-22, as support programs end and the economy recovers.

This would see the budget deficit as a share of GDP peak at around 10% of GDP in 2020-21, which would be its highest since World War 2.

Source: RBA, Australian Treasury, AMP Capital

Spread over several years, this will add nearly 20% of GDP to Australia’s public debt.

But can we afford the surge in the deficit and debt?

It’s not ideal, but it is affordable.

- First, it needs to be stressed that the stimulus is absolutely necessary. If the Government hadn’t imposed the lockdown the healthcare system could have been overwhelmed resulting in many more deaths than the 97 recorded so far. Australia has seen 4 deaths per million people, but the UK and Italy have seen around 500 deaths per million and if that had occurred in Australia it would mean the deaths of around 12,500 people. And if the Government along with the RBA and state governments had not moved to protect jobs, businesses and incomes, the prospective hit to the economy from the lockdown would be far greater, with a much slower recovery in prospect (and probably an even bigger blow out in the budget and public debt). Looked at another way the 10% or so hit to the economy this half year required a similarly sized stimulus program to offset it.

- Second, it makes sense for the public sector to borrow from households and businesses at a time when they are stuck at home and can’t spend due to the shutdown or won’t spend due to uncertainty, and for the Government to give the borrowed funds to help those businesses and individuals that are directly impacted. Using the funds to subsidise wages was a very smart move as it keeps people employed, keeps them linked to their employer and helps minimize confidence zapping unemployment headlines.

- Third, the support programs have been designed to support the economy when they are most likely needed – in the June and September quarters – and to phase down thereafter as is apparent in the table above showing policy stimulus falling sharply from 2021-22. So, under current law we have not seen a permanent step jump higher in government spending. This contrasts with what seemed to happen post the GFC.

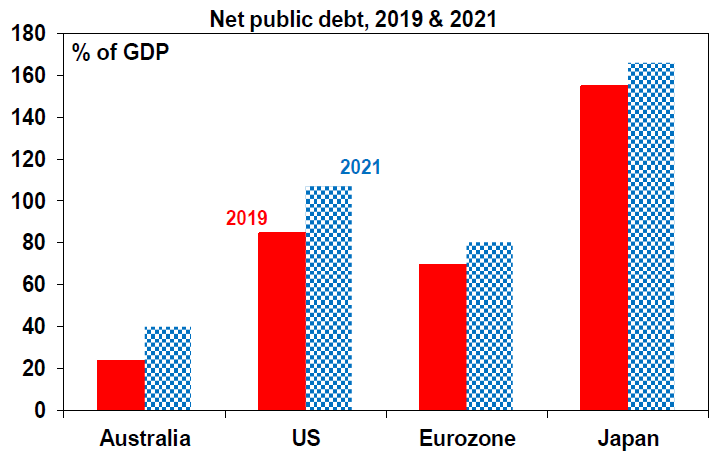

- Fourth, Australia’s net public debt is relatively low at 23% of GDP in comparison with the US at 84%, the Eurozone at 69% and Japan at 154%. See the next chart. And even with the projected budget deficit adding 17% of GDP to public debt by 2021, according to IMF projections Australia’s net public debt will remain relatively small at around 40% of GDP in two years’ time. So, Australia has far greater scope to do fiscal stimulus than other comparable countries.

Source: IMF, AMP Capital

- Fifth, the cost of borrowing for the Federal Government is very low at just 0.25% for three years and 0.95% for ten years. Of course, this is partly being facilitated by the RBA buying bonds in the secondary market, although even if it weren’t bond yields would be low anyway reflecting the massive hit to the economy from the shutdown. And the odd thing about the RBA holding more Government bonds is that much of the interest paid on the bonds by the Government to the RBA will flow back to the Government as a dividend.

- Finally, the Australian Government is borrowing to finance the deterioration in the budget deficit in Australian dollars and given the turnaround in Australia’s balance of payments from a large current account deficit to a surplus or around balance in recent years, it’s not as if we are dependent on foreign creditors risking some sort of foreign currency crisis.

Concluding comment

The blow out in the Australian Government’s budget deficit and public debt is not great. But it’s a necessary price Australia has to pay to minimise the loss of life from the virus and at the same time minimise the hit to people’s livelihoods from the shutdown. In terms of getting the debt back down, a temporary deficit levy would be preferable to tax hikes or the cancelation of tax cuts. But I agree with the Treasurer that the best approach to getting debt back down is to grow the economy aided by a reinvigorated economic reform agenda.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

3 topics

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Shane joined AMP in 1984 and is Chief Economist and Head of Investment Strategy. Shane has extensive experience analysing economic and investment cycles and what current positioning means for the return potential for different asset classes.

Expertise

Comments

Comments

Sign In or Join Free to comment