Concept stocks the professionals like

A significant amount of capital has flowed into concept stocks in recent months as hot themes caught the imagination of investors. This surge has pushed the smallcap index to almost 20 times 2018 earnings, with many stocks at a multiple of this. But high valuations mean high expectations, and given that most concept stocks ultimately fail to deliver, the stakes right now are particularly steep.

To help navigate the minefield, we asked three small-cap experts to put forward one concept stock that they thought looked attractive on a risk-weighted basis. Read on for three stock ideas from Oscar Oberg, Wilson Asset Management; Tim Hannon, Newgate Capital; and Harley Grosser, Capital H management.

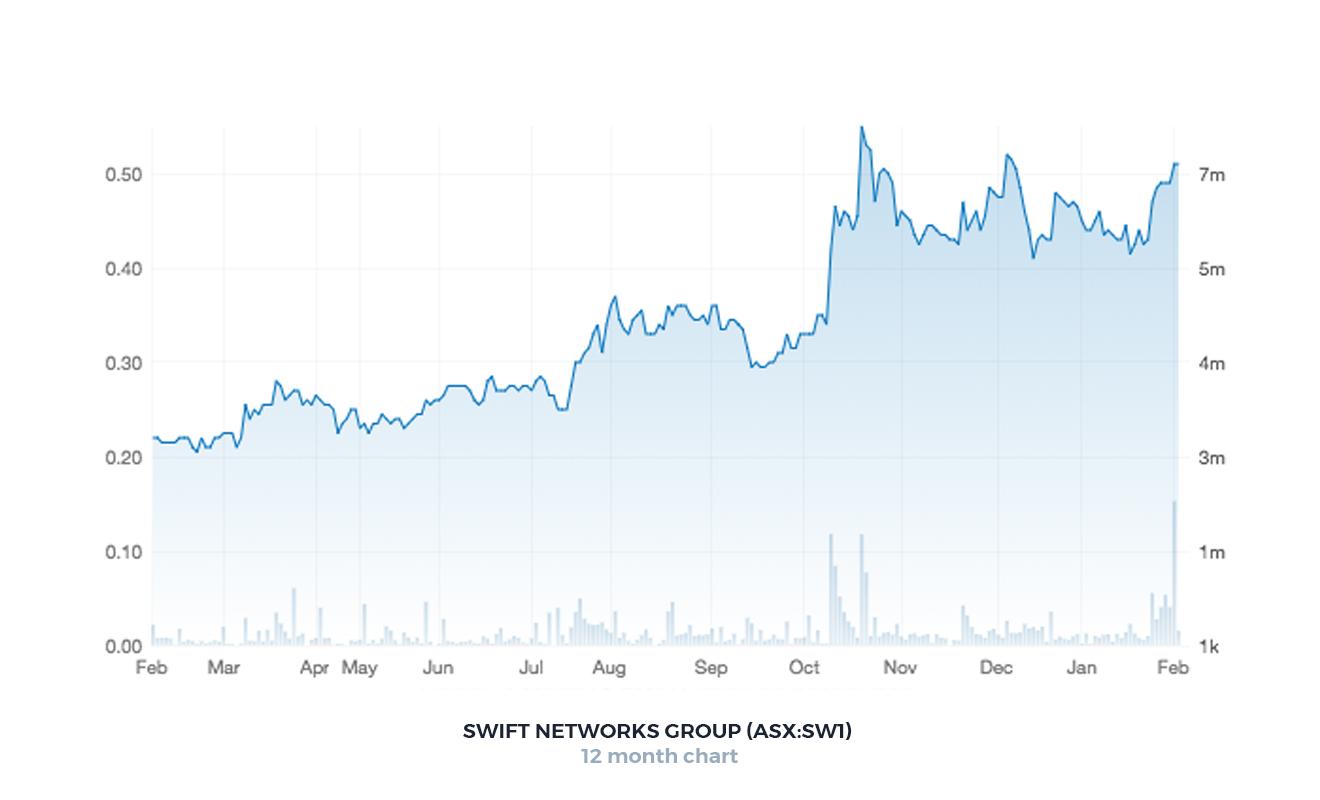

Swift just doubled its profit run rate

Oscar Oberg, Wilson Asset Management

Swift Networks Group (ASX:SW1) is an excellent example of a company that has successfully transitioned from a concept stock to profitable business. Swift provides content delivery platforms for accommodation providers in the hospitality, mining, oil and gas and aged-care sectors.

The company is run by a strong and experienced management team with a track record of developing businesses through acquisitions and organic growth. Over recent years, the company has consistently and regularly provided market updates demonstrating its pathway to profitability.

Swift recently announced unaudited EBITDA of $1.0 million for the first half of FY2018. This result compares with EBITDA of a little over $1.0 million for the last full financial year demonstrating strong profit momentum.

Entities managed by Wilson Asset Management own shares in SW1.

Buy when the market ascribes little success

Harley Grosser, Capital H

In terms of potential longs in early-stage businesses my preferred approach, being an outdated value guy, is to focus first on price and buy when little success is being factored in. One example might be 1st Group (ASX:1ST).

At $11m cap the market isn’t pricing in much success. There is substantial upside in their burgeoning advertising business if they get it right. Health engine is a highly valued comparable.

I could give you more than 10 short ideas on overvalued concept stocks, but timing them would be hard. If a company is willing to stretch the truth it can be a dangerous short. This is just part of the market cycle we find ourselves in.

As Jim Chanos summarised it:

“The fraud cycle follows the financial cycle with a lag. So that as bull markets progress peoples sense of disbelief drops and they get more and more willing to chase returns and too good to be true ideas.”

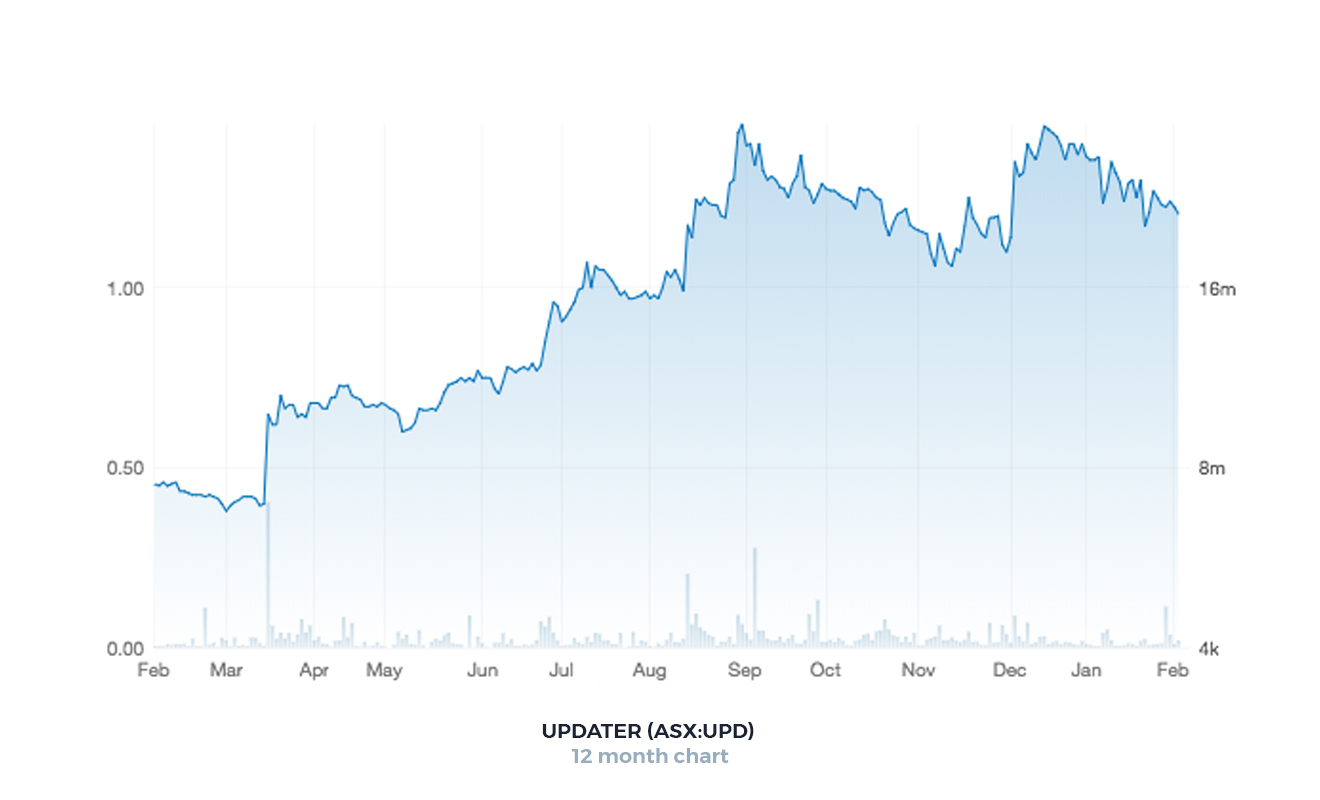

Updater moves into commercialisation phase

Tim Hannon, Newgate Capital

Updater provides a software platform that makes moving to a new house in the USA quicker and easier. Households using the platform can change contact details, organise removalists, and select utility, insurance, media and telecommunication providers. The evidence of the platform’s usefulness is that it processes 16.5% of all moves in the USA - a staggering 2.8 million moves each year.

While it is clear the Updater platform is popular with movers, how will it make money? More importantly, how will the company justify their $AUD 700 million market capitalisation? We explain:

When a household moves it spends on average $US7,400. Companies that provide these products will pay to go on the platform, and if a mover buys these products, the company will receive a commission from them.

If Updater can make just $US27 revenue per move* at a 50% profit margin, they will earn $AUD 47 million. If we multiply these earnings by 15 times, this will justify their current market capitalisation of $AUD 700 million. Is $US27 reasonable? We think so. This represents just 1% of the total value of a $US7,400 move if 40% of movers use the services on the platform. We can compare this to the 10-15% commission earned by insurance and mortgage brokers, and resellers of media and communication services.

It is easy to see if we assume it can earn a commission rate of 2%, or 3%, its market capitalisation should be significantly higher than it is now. Updater has conducted experiments with tens of thousands of users that prove statistically they will more than likely sign up for products that they recommend on the platform. Nonetheless, the caveat on our view is it is yet to scale up its business model and therefore remains a very high-risk investment.

This year Updater will be able to prove the revenue generating capability of its platform, as it moves into commercialisation phase.

This year we will find out.

Sorting the flyers from the flameouts

Click here to hear the processes used by our contributors to sift through concept stocks to help identify the future flyers from the flameouts.

Hot thematics and how to approach them

In the second part of this series, our contributors pass their verdicts on EVs, cannabis, and cryptocurrencies.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

3 contributors mentioned

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Livewire Markets

Livewire Exclusive brings you exclusive content from a wide range of leading fund managers and investment professionals.

Expertise

Comments

Comments

Sign In or Join Free to comment