The converging worlds and diverging interests of equity and bond investors

Investors are used to thinking of equities and corporate bonds separately. However, in reality, they are two sides of the same coin and actions which favour one can have implications for the other.

This is important as decisions taken by companies in the past decade have caused these two worlds to converge. As the cycle matures, companies are going to be forced to choose which side to favour.

Debt vulnerability is emerging in surprising places

Across developed markets, companies have capitalised on the decline in interest rates since the global financial crisis to increase their debt loads substantially.

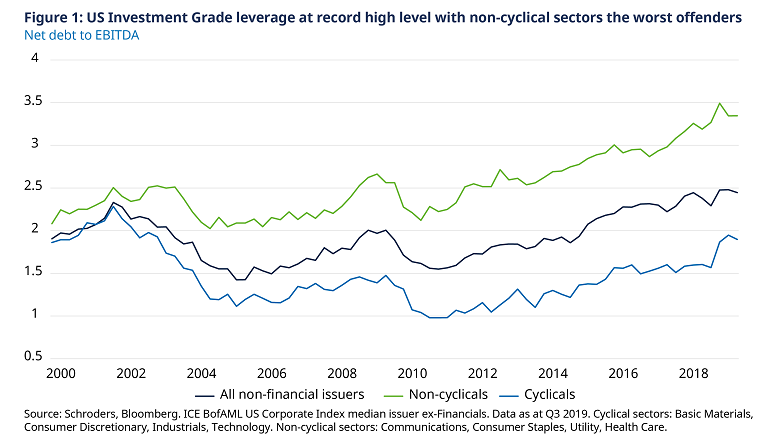

In the US, non-financial companies within the corporate bond market are more highly leveraged than they were during the financial crisis and dotcom crash (Figure 1, dark blue line).

Clearly, from the perspective of a credit investor, this is a worrying trend. However, it also increases risk for equity investors, as high levels of debt increase the risk of financial distress.

Importantly for both equity and corporate bond investors, this accumulation of debt has been most prominent in sectors that investors are used to thinking of as relatively safe.

Debt levels of non-cyclical companies have soared well past previous highs (green line). These include companies in the consumer staples, communications, utilities and healthcare sectors. By contrast, borrowers in more cyclical sectors have been relatively restrained (light blue line).

The dangers in low-risk equity strategies

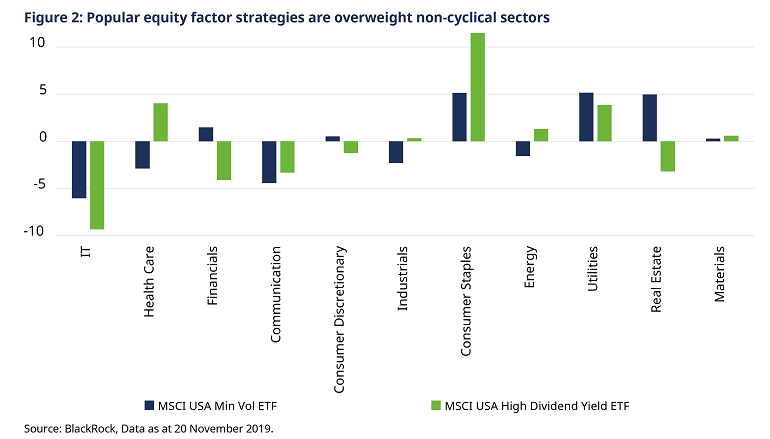

If you are a corporate bond or equity investor, you are used to thinking of these non-cyclical companies as being less sensitive to the economic cycle and, consequently, towards the lower risk end of the spectrum.

For example, consumer staples and utilities are popular sectors in low volatility and high dividend equity strategies (Figure 2).

However, their borrowing binges mean this can no longer be taken for granted. A simple approach of investing in a basket of non-cyclical companies could expose investors to more risk, not less.

Should these companies get in trouble, the performance of strategies which have been aggressively marketed as low risk could suffer.

Time for payback for buybacks?

Another important trend over the past decade has been for corporate management teams to increase pay-outs to shareholders through dividends and, notably in the US, share buybacks.

From the perspective of an equity investor, buybacks have at least two immediate consequences.

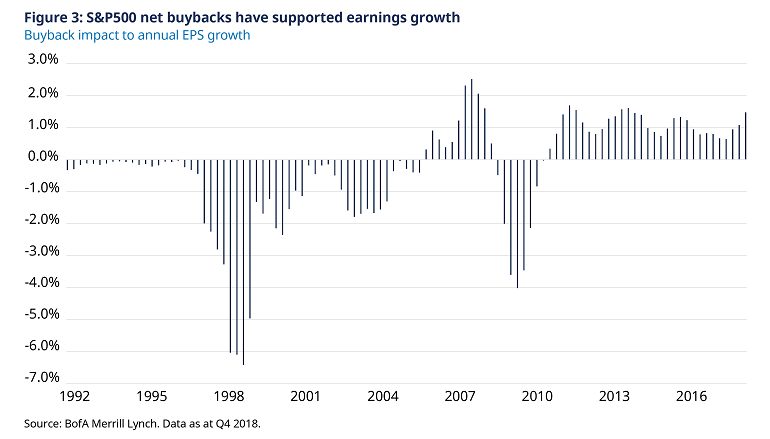

First, they reduce the number of shares outstanding, which provides a boost to earnings per share. Bank of America calculates that, since 2013, net buybacks have contributed 15% of US stock market earnings growth (Figure 3).

The second consequence is that buybacks inject an additional source of demand for a company’s shares and this higher demand can put upward pressure on share prices.

From the perspective of a debt holder, buybacks are unequivocally negative.

They reduce the amount of equity capital on companies’ balance sheets, meaning there is less of a buffer to take a hit before debt holders are exposed to losses.

At the cyclical peak to date in 2017, $150 billion or 34% of US buybacks were funded with debt, according to Goldman Sachs data as at 3 December 2019.

While it can be argued that the switch from equity to debt has been a rational choice given low interest rates, this behaviour might have now reached its natural limit, especially for the most vulnerable companies.

It might come as a surprise to some investors that, before 2004, new stock issuance regularly exceeded buybacks.

The reduction in flexibility can force companies to cut (discretionary) shareholder payments and potentially issue more shares down the line to shore up the gap.

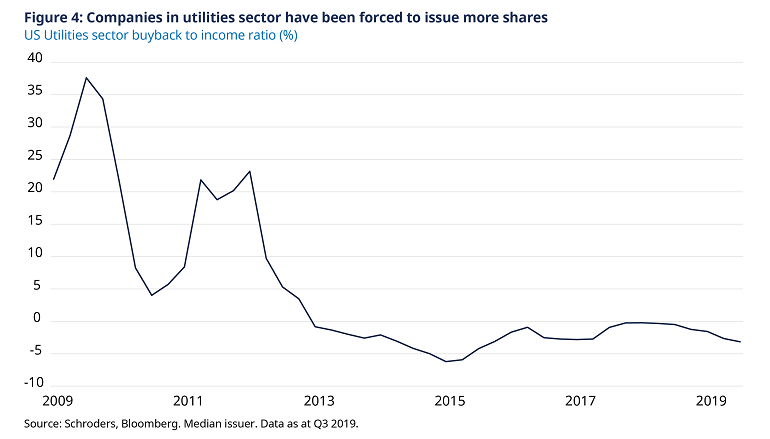

The utilities sector could be a canary in the coal mine in this regard. Since 2013, utility companies have issued more shares then they have bought back, going against the general trend in the market (Figure 4).

Watch out for BBBs

Another area of vulnerability for credit and equity markets is the BBB-rated segment of the corporate bond market.

These are the most vulnerable investment grade companies, on the cusp of sub-investment grade (high yield) status. This issue has grown in importance as the volume of BBB bonds has increased substantially.

They now make up more than 50% of the US investment grade corporate bond market. The potential volume of downgrades is significant.

This is clearly not the kind of uncertainty that investors expect when buying these bonds for stable income.

How to navigate a more challenging environment

Investors in both equities and bonds now face a number of common issues, suggesting that the two worlds are, to some extent converging.

To navigate this more challenging environment, we believe that shareholders will need to adopt more of the balance sheet perspective of credit analysts, with perhaps less of a focus on earnings growth.

Similarly, bond holders will increasingly need to focus more on the viability of current margins and future earnings, instead of falling back on the fragile crutch of high interest coverage.

Companies that continue to engage in equity-friendly actions could put bond holders under pressure. Credit spreads could increase as default and downgrade risk rise.

In contrast, companies that take actions which prioritise bond holders are likely to be less generous when distributing cash to shareholders.

Investors have a tendency to look at equity and credit investments in isolation, separate from one another. However, this is no longer appropriate (if it ever was).

As the economic and credit cycles enter their later stages, their worlds are converging but their interests are diverging.

Learn more

The wire above is an extract from our full report on "The converging worlds and diverging interests of equity and bond investors ". You can read the full version here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Established in 1961, Schroders in Australia is a wholly owned subsidiary of UK-listed Schroders plc. Based in Sydney, the business manages assets for institutional and wholesale clients across Australian equities, fixed income and multi-asset and global equities.

We believe in the potential to gain a competitive advantage from in-house global research; that rigorous research will translate into superior investment performance. We believe that internal analysis of investment securities and markets is paramount when identifying attractive investment opportunities. Proprietary research provides a key foundation of our investment process and our world-wide network of analysts is one of the most comprehensive in funds management.

1 topic

Schroders

Established in 1961, Schroders in Australia is a wholly owned subsidiary of UK-listed Schroders plc. Based in Sydney, the business manages assets for institutional and wholesale clients across Australian equities, fixed income and multi-asset and...

Expertise

Schroders

Established in 1961, Schroders in Australia is a wholly owned subsidiary of UK-listed Schroders plc. Based in Sydney, the business manages assets for institutional and wholesale clients across Australian equities, fixed income and multi-asset and...

Expertise

Comments

Comments

Sign In or Join Free to comment