The curious case of Fed normalisation

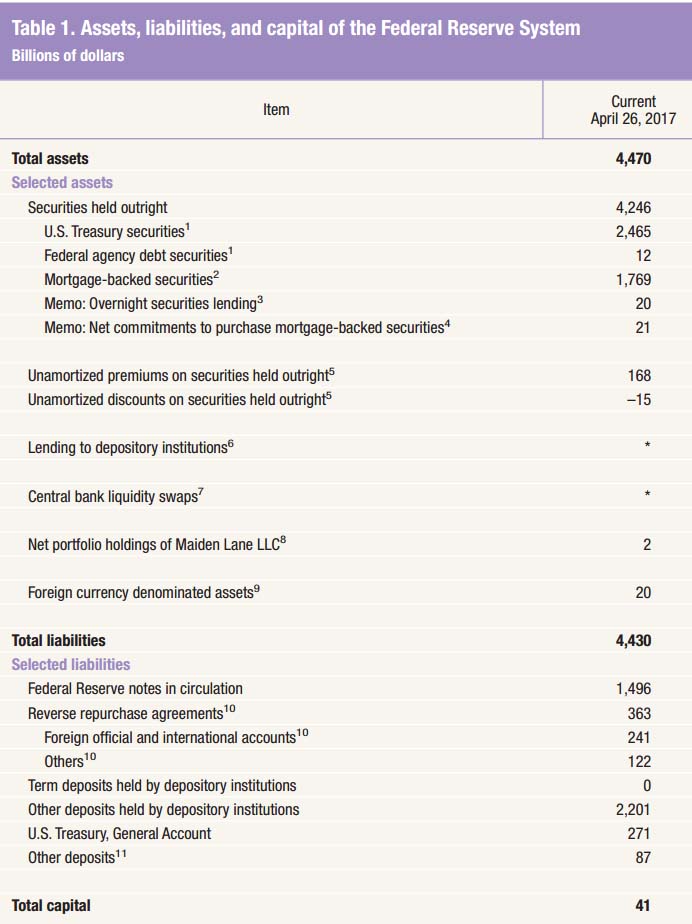

Last week, the Federal Reserve (Fed) hiked its target range for the federal funds rate for the second time this year to 1.00-1.25 percent. In a widely anticipated move, the Federal Open Market Committee (FOMC) said that the labor market has continued to strengthen, economic activity has been rising and household spending has picked up in recent months. But the interest rate decision was not the main event. The market was instead focused on how the Fed planned to deal with its US$4.5 trillion dollar balance sheet (shown below).

For the first time since the Fed began its quantitative easing program in 2009, the FOMC announced it would start a gradual unwind of its balance sheet sometime this year. For those who could benefit from a simple explanation of what this means, see the following bullet points:

- Prior to the Fed embarking on its new quantitative easing program, it routinely controlled the short-term interest rate as a means to influence the money supply in the economy. If the short-term rate was low, banks could fund their lending cheaply which would result in lower borrowing costs for households and corporates. These lower borrowing costs would, in turn, typically result in higher demand for credit. More credit equals more money in the economy which is inflationary. So this was the typical mechanism by which the Fed could influence inflation: if it wanted more, cut the short-term rate; if it wanted less, increase the short-term rate.

- A problem arose in 2009 when the Fed had already cut the short-term rate to zero and yet the economy was still in desperate need of additional stimulus. To achieve this, the Fed, for the first time, engaged in quantitative easing by which it acquired longer-term bonds in the form of Treasuries and mortgage-backed securities in the open market. By buying in such enormous quantity the Fed was easily able to push the price of these bonds upwards – which is equivalent to pushing the yield on these bonds downwards. By artificially forcing treasury and mortgage rates down, borrowing costs for households and corporates became lower and asset prices (in particular property and equities) started to rise.

- The goal here was to stimulate asset prices to create a positive wealth effect under which households feel wealthier and increase consumption. Given the US is such a consumption-led economy, stronger consumption is key to a healthier US economy.

- Now a quick important technical point: the nature of a bond is that it has a fixed maturity date at which point the bond principal is paid to the owner by the issuer. So the Fed, as the owner of a significant number of bonds, would receive enormous payments of principal from the maturing of these various bonds at different times. But the payment of cash to the Fed is akin to reducing the money supply from the broader economy which is disinflationary. To negate this effect, the Fed chose to reinvest all of the proceeds from principal repayments into new bonds.

Which brings us back to the recent announcement. The Fed has announced that, starting this year, the Fed would stop reinvesting all of its principal repayments back into new bonds. Specifically:

- For payments of principal that the Federal Reserve receives from maturing Treasury securities, the Committee anticipates that the cap will be US$6 billion per month initially and will increase in steps of US$6 billion at three-month intervals over 12 months until it reaches US$30 billion per month.

- For payments of principal that the Federal Reserve receives from its holdings of agency debt and mortgage-backed securities, the Committee anticipates that the cap will be $4 billion per month initially and will increase in steps of US$4 billion at three-month intervals over 12 months until it reaches US$20 billion per month.

- The Committee also anticipates that the caps will remain in place once they reach their respective maximums so that the Federal Reserve’s securities holdings will continue to decline in a gradual and predictable manner until the Committee judges that the Federal Reserve is holding no more securities than necessary to implement monetary policy efficiently and effectively.

On the one hand this is a very gradual normalisation: under this policy it would take approximately 8 years to completely normalise the Fed’s balance sheet. On the other hand, a major buyer of Treasuries and mortgage-backed securities is exiting the market. This should result in weaker bond prices and higher bond yields. And this means higher borrowing costs for corporates and households – which, in theory, can handle these higher rates since the economy has strengthened.

So, looking at the yield curve (a curve that charts borrowing costs on the vertical axis against term of those borrowings on the horizontal axis) over recent months, what might you have expected to see? Probably a “steepening” effect. While short-term rates have been slowly increasing over recent months, the combination of the improving economy and Fed’s planned balance sheet normalisation policy should result in higher longer-term yields.

And yet what have we seen? The precise opposite. Shown on the chart below is the difference between the 10YR Treasury bond rate and the 2YR Treasury bond rate. As you can see, since December 2016, this difference has been falling, and plummeted even further today.

How can this be?

To read more articles by me click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Comments

Comments

Sign In or Join Free to comment