The death of coal has been greatly exaggerated

A ‘Materially’ Different Take on Infrastructure: Betting Big Behind the Scenes on Coronado

Global Resources (CRN.ASX) +20% in 2 Weeks with More to Come!

--------------------

According to the Global Infrastructure Hub USD$3.3 trillion will be spent on infrastructure within the next ten years.

Of this amount, over USD$420 billion is earmarked for rail, USD$71billion will be spent on building new / upgrading existing ports and USD$1.1 trillion will go towards building out the energy grid.

Interestingly, the consensus is that these figures aren’t anywhere near enough, with an identified global gap of USD$600 billion between now and 2030 across all major infrastructure sectors.

In an environment of low interest rates, low productivity growth and an unequivocal need to ‘grow our way out’ of the economic havoc unleashed by COVID-19, it is fair to say that this gap will attract the attention of policy makers keen to get back on the front foot.

But how best to invest in this thematic? Where are the overlooked opportunities available right here and now?

Looking behind the curtain:

One way to go about this is to take a step back and look behind the scenes – what type of inputs are common to the majority of infrastructure projects that are already in the pipeline (pun intended!)?

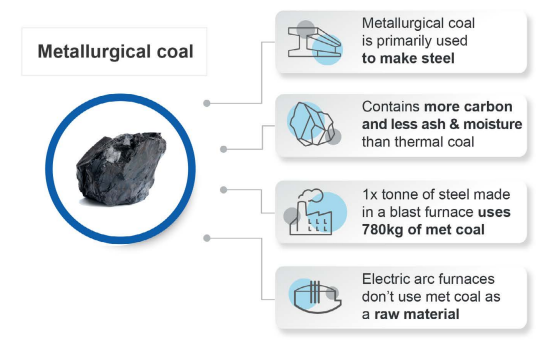

The obvious answer to this is steel. To make steel the two main inputs needed are iron ore (which has undergone a significant upward re-rating, even during the COVID-19 pandemic) and metallurgical coal (which hit a four year price low only a few months ago and, for the first time in 10 years, traded at a discount to iron ore).

Figure 1: Metallurgical Coal Prices

.png)

Naturally, metallurgical coal, on a pure pricing basis, looks attractive and, following June’s lows the price has rebounded strongly to approximately USD$118 per ton, with futures contracts indicating a further uptick to over USD$150 per ton by Q1 CY 2021.

Figure 2: Key Features of Metallurgical Coal

So how can investors gain exposure to metallurgical coal?

Most of the mid to large listed coal mining companies on the Australian Stock Exchange (ASX) offer thermal coal exposure with just a little metallurgical coal as a byproduct. Coronado Global Resources (Coronado) is the only Australian producer that offers an almost pure play metallurgical coal exposure (>80% of coal production being met-coal).

The distinction between the two types of coal is important.

Many private and institutional investors have shunned thermal coal in recent times, but the same can’t be said for metallurgical coal. Indeed, one of the biggest institutional shareholders of Coronado is Australian Super, the largest industry superannuation fund in the country!

The case for Coronado

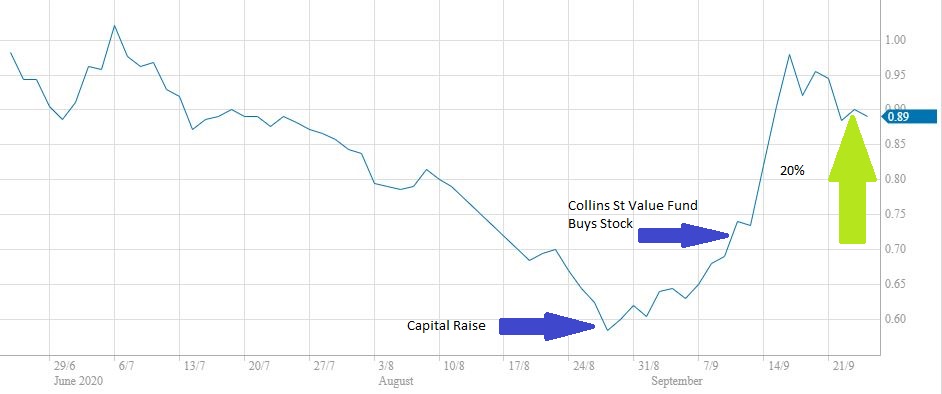

The Collins St Value Fund established a position in the stock in mid September 2020 at an average price of $0.72 per share. As of the date of writing, the stock is now worth ~$0.89 per share – a 20% uplift in two weeks which, in our view, is just the beginning of an immensely compelling investment opportunity that began in earnest after their recent USD$180 million capital raise at $0.60 per share in early September 2020.

Beyond the longer-term infrastructure tail winds supporting Coronado, there are three more immediate reasons why the stock represents a compelling investment opportunity.

1. Capital management

Post the recent capital raise the company has been able to bring net debt/equity down to below 50% with the company’s liquid cash position expected to be enhanced by a further $50M - $100M post the sale / lease back of assets at the Curragh mine in Blackwater, Queensland. With its balance sheet back in order, dividends are expected to return with the company dividend policy suggesting that 80% of free cash flow will be paid out each year – quite attractive given the reduced yield on offer elsewhere in the market.

Another relevant consequence of the recent capital raise is that the dilution of the major shareholder has seen the company’s free float stock increase to 44% (up from 20%), providing greater liquidity for investors as well as opening up the prospect for being included in the ASX300 index and attracting greater analyst coverage as well as passive ETFs coming onto the register for the first time.

2. Geographical Diversity

Coronado have eight operating mines, with one of those in Queensland and seven in the central Appalachian region in the United States of America (USA). This geographical diversity provides an excellent opportunity to cost effectively sell and export coal to a wide range of markets across South-East Asia, Europe and internally within the USA.

3. Operational excellence

Given the ‘price taker’ status afforded to most commodity producers it is important that costs are managed closely. Coronado are in the lowest cost quartile globally and have a strong executive team in place in order to maintain that position into the future.

Safety is also key. With Total Reportable Incident Rates (TRIRs) historically less than a third of the industry average it is clear that this is something the company takes seriously.

Outlook for the share price

With metallurgical coal futures pointing to a further 50% uplift in price into the first quarter of CY 2021, lower debt and increased liquidity the outlook is extremely positive. Notwithstanding the short term price action seen throughout September we maintain the view that Coronado could see further appreciation of 70% or more, with a price target north of $1.60 by this time next year.

Structural (again, pun intended!) tail winds driven by increased global infrastructure spending provide ample opportunity for Coronado’s long life mining assets to deliver for shareholders well beyond the next 12 months, representing an excellent example of how looking behind the scenes can uncover overlooked, under loved and misunderstood opportunities in a bigger value chain.

Like this wire? Let us know by hitting the 'like' button to the left.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Michael is the MD and one of the founding partners of the Collins St Value Fund.

The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by Mercer in 2019 & 2020.

With no fixed management fee, the investment team only benefit when our investors do.

4 topics

1 stock mentioned

Michael is the MD and one of the founding partners of the Collins St Value Fund. The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by...

Expertise

Michael is the MD and one of the founding partners of the Collins St Value Fund. The Collins St Value Fund is one of the best performing Funds in Australia - having ranked among the top 10 performing funds across all Australian Equity mandates by...

Expertise

Comments

Comments

Sign In or Join Free to comment