The highest-priced maturing SaaS name in the world?

Avoca Investment Management

Avoca Investment Management

A consensus is building in markets around global economic expansion, QE curtailment and an upward trajectory in rates. The OECD’s September 2017 outlook statement described it as “a synchronised short-term global upturn” with the recovery being “broad-based”.

Consistent with this rhetoric, the OECD’s forecast for 2018 global GDP growth was revised up to 3.7% from June (3.6%), the highest level since pre-GFC. They added the caveat, however, that “sustained medium-term growth is far from secured”. The GFC continues to cast a long shadow.

Growth vs Value? 3 ways to rationalise the current paradox

With this in mind, a question for equity investors is the perennial: growth vs value? Conventional wisdom would have it that with economic activity accelerating from the desultory post-GFC years, and with interest rates on the march (US 10-year yields up 100bp since June 2016), value should be outperforming growth and defensives. However, that has not been the case.

Rationalising this apparent paradox probably comes down to three factors:

- technological disruption (SaaS/cloud);

- the performance of FAANG (FB +27% vs S&P 500 since June 2016, AAPL +48%, AMZN +28%, NFLX +73%, GOOGL +20%); and

- quant’s preference for momentum over value.

Many tech names have been re-rated on the back of FAANG. Indeed, the S&P 500 now has more names at EV/sales > 10x than at any time since 2000 (8% of the index).

In Australia, 8% of the Small Industrials ex REITs is also on EV/sales > 10x. To us this is worrying, notwithstanding the digital paradigm.

A justified premium or hopelessly overpriced?

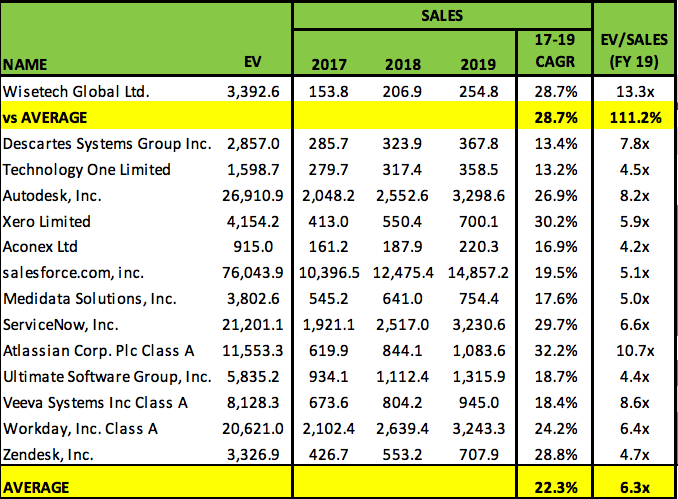

Focusing on one Australian SaaS name – Wisetech (WTC), a global leader in logistics SaaS. Its track record is strong and it has M&A potential.

Nonetheless, does it deserve to be rated as it is (13x EV/ FY 19 sales) – possibly the highest-priced maturing SaaS name in the world?

This is representative of the question investors in most of these highly-rated tech names need to ask. In some cases, the answer will be that the long-term growth profile justifies the high near-term rating. In many other cases, the answer will be that the name is just hopelessly overpriced.

Time will tell.

Wisetch vs Global SaaS

Source: Factset, Avoca

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

1 topic

1 stock mentioned

Avoca Investment Management

Avoca Investment Management

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

Expertise

Avoca Investment Management

Avoca Investment Management

Avoca Investment Management was established in 2011 by John Campbell and Jeremy Bendeich in partnership with Bennelong Funds Management. The team is focused on capital preservation through prudent, long-term investment in emerging leaders.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management