The Insurers: QBE versus IAG

There have been so many results which have provoked share price volatility, with the usual mix of outstanding results such as CSL balanced by disappointing results like Vocus. Or ones like Boral, where management convinced the market the outlook is bright despite a weak performance in key parts of the business.

With so many choices of notable results, I have opted to focus on a longer-term perspective of Australia's insurance giants QBE and IAG. This has been reinforced this reporting season, because I am much more focused on generating long-term outperformance, than worrying about short-term volatility. First a quick review of each player.

QBE's acquisitive model has unraveled

QBE is a major global general insurance company. After an emergency capital raising in the wake of the September 11 tragedy at the World Trade Centre where QBE faced major claims, the business became a market darling under Frank O’Halloran, buying insurance companies around the globe.

Each acquisition was touted as an excellent opportunity to achieve synergies and scale, and lowering the risk of the business by diversifying geographically. Investors were told that the company required less capital relative to the size of the business or premiums written, thanks to the magic of this geographic diversification. QBE’s acquisitions were much more about building a global empire and financially engineering the balance sheet.

However, over the past several years QBE’s acquisitive model has unraveled, with declining earnings and a balance sheet needing repair. They have undertaken several equity raisings to bolster its balance sheet that previously was supposed to not need so much capital because of all the diversification.

IAG: Evolved into a higher quality franchise

IAG, after a disastrous foray into the UK under Mike Hawker, also touted as a wonderful diversification to gullible investors at the time, has for many years been very much an Australasian general insurance company with a relatively small investment in some Asian countries. Having licked its wounds over the UK, new management under Mike Wilkins and now Peter Harmer have focussed on acquiring domestically (buying Lumley from Wesfarmers) or in New Zealand where the synergies are tangible in terms of reinsurance buying power, corporate and headcount efficiencies.

IAG has a much higher quality franchise where they largely deal directly with households who trust the brands such as NRMA and who generally renew their policies each year. QBE mostly deals with companies through large brokers who focus mostly on getting the best price. While QBE has struggled to maintain earnings and differentiate itself to customers, IAG by contrast has lowered the volatility of its earnings by signing a quota share agreement (effectively reinsurance) with Berkshire Hathaway.

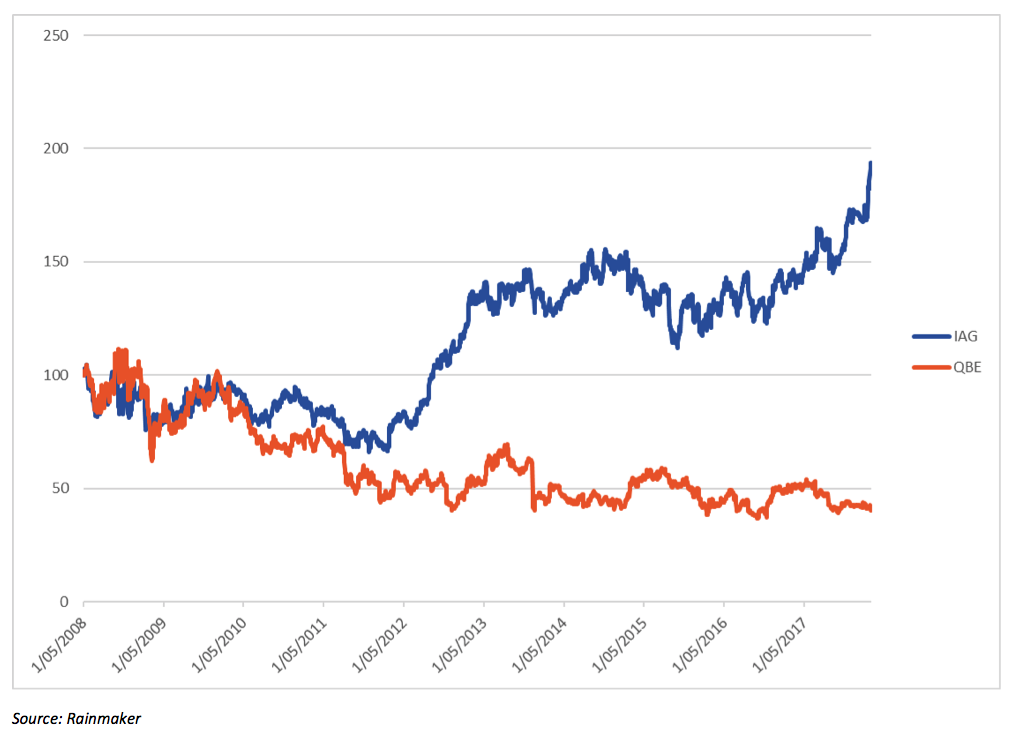

Ten-year chart of $100 invested in IAG and QBE

What this reporting season showed

In the latest reporting season, IAG surprised the market with strong earnings powered by their strong franchise in personal lines such as home and motor.

QBE produced another weak set of numbers and announced they are divesting their Latin American business. So much for the great global empire and supposed geographic diversification benefits.

Interestingly QBE made a bid for IAG which was rebuffed in 2008. The offer was 90c plus 0.145 QBE shares. That would be worth under $2.40 today, whereas IAG’s shares are worth over $8 thanks to a much stronger franchise than QBE and much stronger balance sheet.

For further market analysis from the team at Investors Mutual, please visit our website

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Hugh is co-manager of the IML Australian Share Fund and is Portfolio Manager of the IML Concentrated Australian Share Fund. He is also the Head of Research for IML. Hugh has extensive investment experience in equities, and holds a M. Phil Economics from Cambridge.

2 topics

2 stocks mentioned

Hugh is co-manager of the IML Australian Share Fund and is Portfolio Manager of the IML Concentrated Australian Share Fund. He is also the Head of Research for IML. Hugh has extensive investment experience in equities, and holds a M. Phil...

Expertise

Hugh is co-manager of the IML Australian Share Fund and is Portfolio Manager of the IML Concentrated Australian Share Fund. He is also the Head of Research for IML. Hugh has extensive investment experience in equities, and holds a M. Phil...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The Magnificent Seven can’t carry the market forever

Pzena Investment Management