The Meerkat Feasting on iSelect

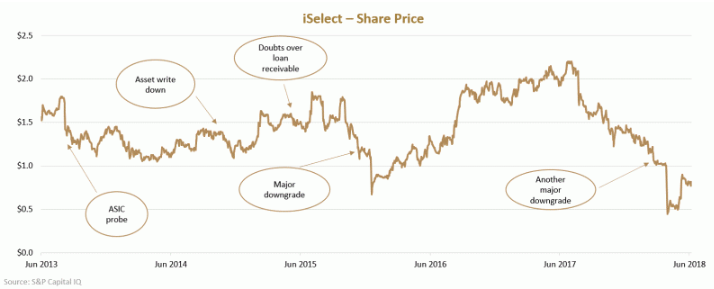

Earnings guidance slashed by 64%. CEO gone. The stock down 54%. That was the situation for iSelect (ISU) when we started buying the stock in April. And this isn’t their first time disappointing investors. That sounds horrible, so why does the Australian Fund now own 9% of the company?

While iSelect doesn’t compare all health insurers (Medibank and BUPA mostly stay off the site), there is a big range of policies to choose from. The consumer gets a better deal and iSelect gets paid to refer clients to providers. It seems simple. Unfortunately it isn’t quite that easy.

Since listing the business has disappointed in nearly every year. A missed prospectus forecast led to an ASIC probe in 2013. Expected future cash flows were written down in 2014. Financial year 2015 saw the failure of a health insurer to which iSelect lent money and there was another major downgrade in 2016. The business is now onto its fourth CEO in five years. And that’s not where the problems end.

Attracting consumers to the site is costly. And it’s getting costlier. A third of iSelect’s revenue went into marketing last year and about half of that was spent on paid search engine marketing with Google. With competing comparison sites and the health funds themselves spending to attract clients, the best words have been costing 15% more each year. As a result, iSelect has been spending more offline this year. But while a $10m TV campaign can generate $20m or more of revenue, it can also be a complete flop. And that’s what happened to trigger iSelect’s current downgrade woes.

The past and the future

Yet there are a few valuable assets and a viable future business in the mess. Start with the assets. Some insurers pay iSelect upfront for referring a client. Others pay each month while the client remains with the insurer. This means the business is collecting cash on work it did years ago. This cash flow stream, paired with some cash and a small investment in a similar business offshore, is worth about $0.58 per share.

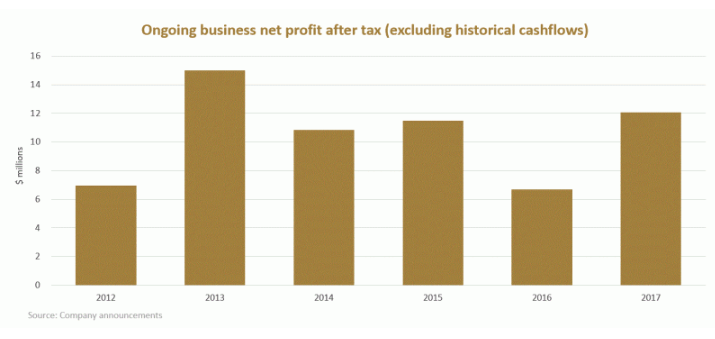

While iSelect’s earnings have been unstable, the business has averaged $10m in net profit per year excluding the historical payments. It still has high market share in new health insurance policies, brand recognition and a place in the marketing budgets of health insurers.

That was more than enough to get us interested. Then things really heated up.

The Meerkat feasting on iSelect

The owner of Compare the Market (think meerkats), the largest domestic competitor, took advantage of the downgrade to acquire 20% of iSelect. It has been a fierce rival in the last few years and is funded by a UK group which recently took in £675 million in funding. The combination of the two businesses would make a lot of sense. Duplicated costs could be removed. Marketing budgets could be trimmed. And the combined group would be a key distribution channel for private health insurers. With all these benefits, Compare the Market will have to pay up if they want to take full ownership of iSelect.

In the meantime iSelect will be tidying up its marketing spend and working on selling more products more effectively. A little improvement can go a long way on this one.

Further Insight

If you are interested in receiving the Forager monthly and quarterly reports, please register here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

.jpg)

.jpg)

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

Expertise

Alex is a Portfolio Manager at Forager Funds Management, responsible for managing the Forager Australian Shares Fund alongside CIO Steve Johnson

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

8 ETFs with the tick of approval from advisers for FY26

Livewire Markets

Equities

Are CSL's best days behind it?

Livewire Markets