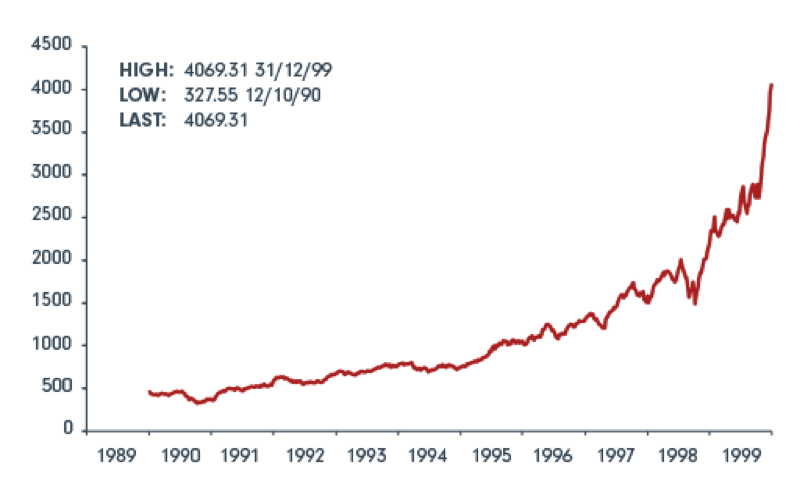

The Nasdaq: Will history repeat or will it rhyme?

There aren’t many advantages to being the wrong side of 50. One very clear benefit for investors of a certain age, however, is the fact that, whatever the market turns up, you’ve already seen something similar. My two charts this week are a perfect visual representation of Mark Twain’s famous adage that history doesn’t repeat itself but it often rhymes.

In both the ten years to date and the ten years from 1989 to 1999 the US’s main technology share index, NASDAQ, turned left and headed up the page. For those with the luck or foresight to get in early, this was pure alchemy and a far better way of making money than the dull business of having a job.

Last week, NASDAQ passed 6,000 for the first time. Inevitably, this milestone triggered a flurry of hand-wringing articles drawing parallels with the dot.com bubble of 17 years ago. Eight years into a bull market, it’s unsurprising that investors should be nervous about a re-run of the calamitous market slide between 2000 and 2003. Having lived and invested through both periods, however, I’m not convinced that we’re heading the same way just yet.

If you are looking for similarities, of course, you’ll find them. The first is the increasingly narrow focus of the market leadership. Technology stocks account for a disproportionate share of the market gains so far this year - a handful of shares account for about a third of the S&P 500’s year to date gain. The five largest US technology companies - Apple, Google-owner Alphabet, Microsoft, Amazon and Facebook - have seen the value of their shares rise by more than $400bn in the first four months of 2017. That’s roughly the GDP of Austria or Thailand.

Comparing the level of NASDAQ with that of the S&P 500, a rough gauge of investor enthusiasm for tech stocks compared with the stock market as a whole, the current multiple of about 2.5 is reminiscent of the headiest days of the dot.com boom. Valuations of tech stocks are also reawakening memories of the blind enthusiasm of the 1990s internet mania when no-one bothered looking at tedious old measures like profits and dividends.

The flotation of Snapchat’s parent company recently with a market capitalisation of nearly $30bn looked pretty crazy to me at the time so I was unsurprised last week when slightly disappointing user numbers and a bigger than expected loss resulted in a 25pc fall in the share price. Having soared by over 40pc on the first day of trading, however, even that was really just blowing some of the froth away.

Snap is not alone. Netflix is another good example of a company that we all love to use but might think twice about investing in. Cash is streaming out of the business - at an estimated rate of $2bn this year. And yet the shares have risen by more than 40pc so far in 2017. Investors are focused on the potential of its 100 million subscribers, up by a third in a year. The company is losing money on each of these customers but the market doesn’t care, just as it didn’t in 1999.

Finally, there’s the whiff of capitulation in the air, with even Warren Buffett apologising to Berkshire Hathaway shareholders about his failure to clamber aboard the tech stock bandwagon.

The most dangerous words in investment are ‘it’s different this time’, especially when the visual clue in the charts suggests the opposite. However, there are a few good reasons to think that 2017 is not 1999 redux. So why should we keep the faith with technology stocks for a while longer?

The first key difference between then and now is the massive growth in the internet and the increasing centrality of the web to our lives. In the late 1990s, only around 300 million people even had access to the internet. Today ten times as many do. Then, accessing the web was slow, clunky and tied you to your desk. Today we all carry around in our pockets a device with capabilities that we would never have dreamed possible a generation ago.

Second, the valuations of most tech stocks today are far less scary than they were in 1999. Back then, valuations were rising much more quickly than profits. Today they are falling behind. The world’s biggest company, Apple, trades on around 17 times earnings. Google and Microsoft are priced at roughly 30 times. Back in the day, Microsoft was valued at nearly 50 times earnings, Intel sported a PE ratio of 190 and Oracle 140. Indeed, comparing today’s valuations with those in the 1990s suggests that, on a dot.com clock, we are currently closer to 1997 than 1999.

A third key difference is the sheer scale of the opportunity thanks to new business models enabled by the ubiquity of mobile devices today. The recent valuation of $50bn implied by Uber’s recent fund-raising may look absurd compared with a global taxi market worth perhaps $11bn but enthusiasts argue that this is like trying to value eBay in 1999 against the revenues earned in car boot sales. Disruptive technologies create value where it never existed before - what if Uber is successful in related areas like food delivery?

Finally, it’s worth considering the speed of change that capital-lite business models like AirBnb can achieve. It took Marriott nearly 90 years to get to 700,000 rooms. AirBnb has reached 1.5 million in just seven years.

My charts make me as nervous as the next investor. What reassures me to a degree is the difference in the mood music between now and 17 years ago. Today’s enthusiasm for technology is not really about rose-tinted optimism but a grudging belief that in a sluggish world, the sector is one of the few places that investors can find reliable growth. The euphoria of 1999 is almost wholly absent.

--

This document is issued by FIL Responsible Entity (Australia) Limited ABN 33 148 059 009, AFSL No. 409340 (“Fidelity Australia”). Fidelity Australia is a member of the FIL Limited group of companies commonly known as Fidelity International.

Investments in overseas markets can be affected by currency exchange and this may affect the value of your investment. Investments in small and emerging markets can be more volatile than investments in developed markets.

This document is intended for use by advisers and wholesale investors. Retail investors should not rely on any information in this document without first seeking advice from their financial adviser. You should consider these matters before acting on the information. You should also consider the relevant Product Disclosure Statements (“PDS”) for any Fidelity Australia product mentioned in this document before making any decision about whether to acquire the product. The PDS can be obtained by contacting Fidelity Australia on 1800 119 270 or by downloading it from our website at (VIEW LINK). While the information contained in this document has been prepared with reasonable care, no responsibility or liability is accepted for any errors or omissions or misstatements however caused. This document is intended as general information only. The document may not be reproduced or transmitted without prior written permission of Fidelity Australia. The issuer of Fidelity’s managed investment schemes is FIL Responsible Entity (Australia) Limited ABN 33 148 059 009. Reference to ($) are in Australian dollars unless stated otherwise.

© 2017 FIL Responsible Entity (Australia) Limited. Fidelity, Fidelity International and the Fidelity International logo and F symbol are trademarks of FIL Limited.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Fidelity International provides world class investment solutions and retirement expertise to institutions, individuals and their advisers - to help our clients build better futures for themselves and generations to come.

Fidelity International

Fidelity International provides world class investment solutions and retirement expertise to institutions, individuals and their advisers - to help our clients build better futures for themselves and generations to come.

Fidelity International

Fidelity International provides world class investment solutions and retirement expertise to institutions, individuals and their advisers - to help our clients build better futures for themselves and generations to come.

Comments

Comments

Sign In or Join Free to comment