The next Black Swan

One of my favourite finance books was given to me by Mark Carnegie after a meeting where we discussed markets and valuation. That book is called The (Mis)behavior of Markets, and its author was none other than Benoit Mandelbrot – the father of fractal theory. Mandlebrot’s idea is that the traditional normal distribution does not properly capture empirical and “real world” distributions, and there are other forms of randomness that can be used to model extreme changes in risk and randomness. A somewhat humorous example of this failure of the normal distribution is the once-in-a-hundred-year flood, which we all regularly joke seems to happen every couple of years. Below, I discuss Nassim Taleb's 'Fooled by Randomness, and a major risk facing markets today.

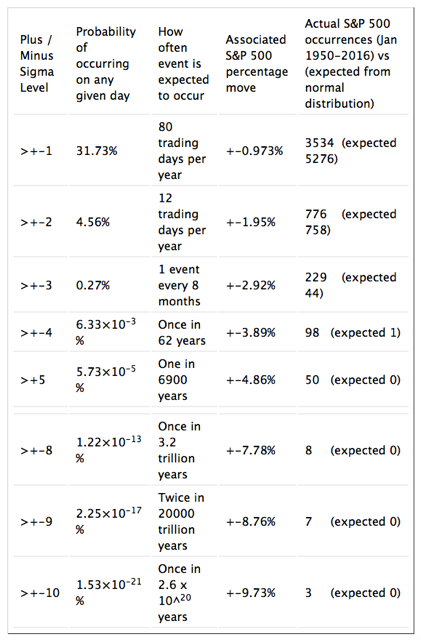

In finance, experts have adopted the ‘sigma’ notation to help put big market moves or valuation extremes into context. For example, if the S&P 500 drops 4.86 per cent in a day we can determine the sigma level of this event by dividing the percentage drop (4.86 percent) by the S&P’s historical standard deviation of about 0.973 percent. A 4.86 percent move would be described as a five-sigma event.

The Normal Distribution Curve is a convenient tool to explain the distribution of many things, but to a man with a hammer, all problems look like a nail, and today the normal distribution is used to help describe a plethora of observations.

It doesn’t fully inform an investor about the risks of investing in the market.

For example as the table shows, according to the normal distribution model, a five sigma event in the S&P500 is expected to occur once every 6900 years. However, between 1950 and the 24th of June 2016, the S&P500 recorded a 4.86 per cent move fifty times.

Source: Vance Harwood

Mandlebrot instead observed that randomness could become quite “wild” if the requirements regarding finite mean and variance are abandoned. Wild randomness corresponds to situations in which a single observation or a particular outcome can impact the total in a very disproportionate way.

Now to Nassim Taleb, the man who popularized the “The Black Swan” theory with his book of the same name. His book Fooled by Randomness states that the past cannot predict the future – invalidating technical analysis.

Reading Taleb and Mandelbrot one cannot help but arrive at a point where tail risk hedging to limit losses from an outsized market move makes sense.

In a recent interview with Julia La Roche, a finance reporter at Yahoo Finance. Taleb was asked for what he believes is the biggest risk that exists right now.

NT: “The fact that the world, as a result of quantitative easing, has seen an asset inflation that benefited the uber-rich, and that nothing has been cured. One cannot cure debt with debt, by transferring from private to public sectors. The markets will ultimately crash again, although this time, it will hurt a lot more people”.

YF: A lot of people throw around the phrase ‘black swan’ haphazardly. What do people most commonly get wrong when talking about black swans?

NT: They don’t get that what matters is to be protected against those tail risks, something easier to do than trying to predict them. The idea is to focus on portfolio robustness rather than forecasts.

You can read the full interview here: (VIEW LINK)

Article contributed by Montgomery Investment Management: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Roger Montgomery founded Montgomery Investment Management in 2010. Roger has more than three decades of experience in investing, financial markets and analysis. Roger also authored the best-selling investment book, Value.able.

3 topics

Roger Montgomery founded Montgomery Investment Management in 2010. Roger has more than three decades of experience in investing, financial markets and analysis. Roger also authored the best-selling investment book, Value.able.

Expertise

Roger Montgomery founded Montgomery Investment Management in 2010. Roger has more than three decades of experience in investing, financial markets and analysis. Roger also authored the best-selling investment book, Value.able.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management