Opportunity is ripe for active investors

The recovery we have seen in share markets since the low on 23 March 2020 has been the fastest rebound in history. Yet, the economic data has been dire with unemployment rising rapidly and both manufacturing and services industries suffering. According to the RBA, national output is likely to fall by around 10% over the first half of 2020, with most of this decline taking place in the June quarter and unemployment is likely to be around 10% by June.

So, what is driving the rally? The most obvious rationale is the US$8 trillion plus of monetary and fiscal stimulus from global governments and central banks to support their economies. The response has been larger and faster than the GFC. The S&P 500 for example, is up 32% since its March 23 lows and although markets are still 12% behind the market peak on February 19, given the scale of the pandemic and impact on supply chains many are asking if the rally can last.

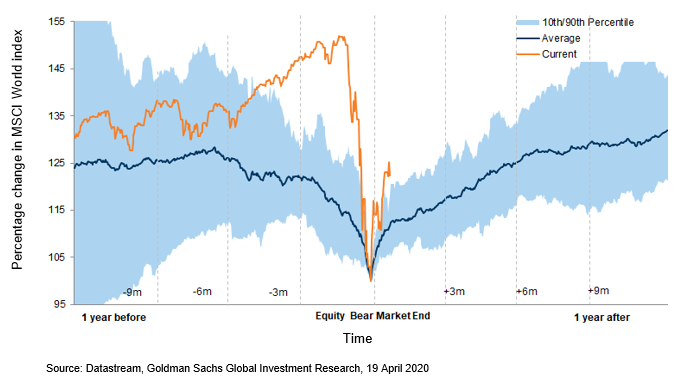

MSCI World Recoveries since 1970

For active investors, the opportunity set is ripe. During this period of economic uncertainty, the process to select companies for a portfolio is focused on which companies will not only thrive but survive the lockdown period. During periods such as this, opportunities arise. Currently three areas of current focus for opportunity include:

- Cyclical rebounds: Many industries have been decimated and those companies with strong operating cash flow, sufficient liquidity and manageable debt levels are more likely to survive. Determining which companies will rally when the cycle turns can provide an attractive source of alpha.

- Access to capital: With limited cash flow due to the lockdown restrictions many companies are raising equity. Some of these offers are not as attractive as others but this environment also offers active investors the opportunity to pick up quality companies at a significant discount.

- The yield trap: Stocks that have traditionally been the hunting ground for yield-hungry investors could look very different in the medium term. With many companies deferring or cutting dividends, further analysis of balance sheet strength and cash flow is needed to assess which companies can produce reliable dividends in the future.

The following will outline in greater detail these key points with case studies of companies that some of our Equity boutique investment managers at Fidante Partners are currently taking advantage of.

Identifying cyclical rebounds

Contrary to other economic downturns such as the GFC and Tech Wreck which have been dissected for clues on the potential path forward for the current crisis; this time there are sectors of the economy that have not only slowed down but ground to a halt. For sectors such as tourism, retail and aviation recent events may accelerate trends that would otherwise have taken years to eventuate such as the increasing trend towards online transactions and the move away from cash payments.

For some of these businesses cash flow has gone negative due to refunds for holidays that cannot be taken. Therefore, it is unsurprising that for many businesses in these categories their share price falls have exceeded the index. Some will not survive, others will need an injection of capital and others should perform well when restrictions are lifted. Fund managers are actively assessing which companies’ earnings are likely to turn around faster than the market is expecting. In many cases, it is dependent on consumer behaviour and what households will spend money on once lockdown restrictions are lifted. Investing in companies that are likely to beat expectations has proven to be a consistent source of alpha.

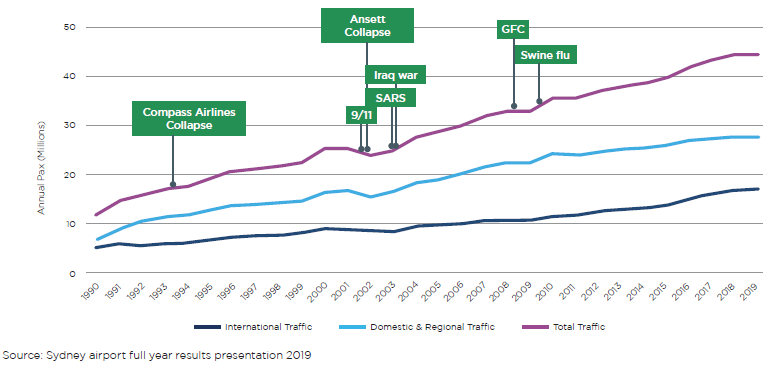

The tourism sector has been one of the heaviest hit by the pandemic and Qantas (QAN:ASX) has grounded much of its fleet and furloughed most of its staff. Active managers are assessing whether Qantas has enough liquidity to withstand the lockdown period, what history tells us about previous pandemics regarding consumer behaviour and how well Qantas can manage costs. Virgin Australia has entered voluntary administration and could pare back its domestic network and close its international operations if it emerges. This could give Qantas more domestic monopoly routes and reduce competition for international routes. Qantas has a strong balance sheet, entering this crisis with $2bn in cash, $1bn undrawn debt facilities and $4.5bn of unencumbered aircraft. With politicians already talking about relaxing international restrictions with New Zealand preceded by the opening of domestic routes, conditions are improving. While the recovery timeline is uncertain, what occurred during the SARS outbreak could provide some insights into consumer behaviour whereby domestic travel improved before international resumed.

Passenger Traffic

Companies with access to capital

The impact of the lockdown on corporate cash flows has led an increasing number of companies to tap the market for capital. In April 2020 alone, Australian companies raised over A$13bn of equity. For some, this will ensure their survival, for others it is an effort to shore up their balance sheets as falling revenue impacts their bottom line. Stock pickers must sift through these offers and consider whether they represent an opportunity to pick up shares in companies that they have long coveted but previously considered too expensive, or whether they should give it a wide berth based on company fundamentals or for portfolio construction reasons. In addition, at the end of March emergency capital raising relief rules were introduced which allows issuers to issue 25% of new shares provided placements are accompanied by a share purchase plan at the same or a lower price. In these circumstances, investors can buy shares at a substantial discount. Although these capital raisings dilute existing shareholders, they provide liquidity, a stronger balance sheet and better survival prospects for issuers.

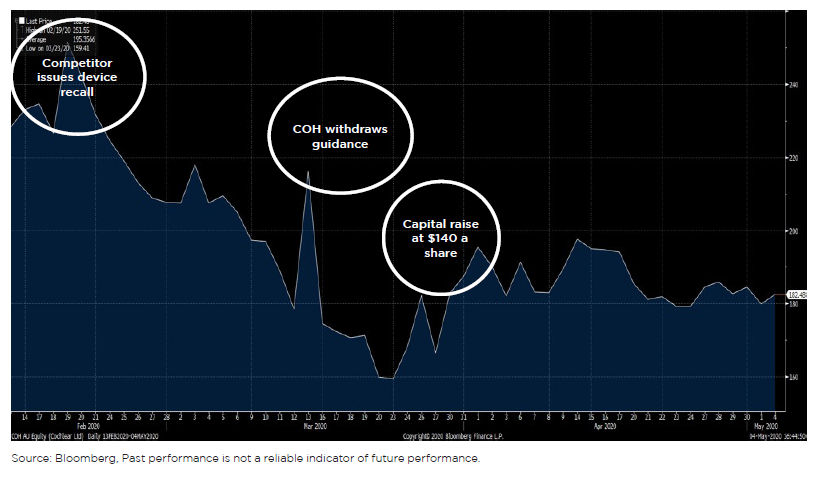

Cochlear (COH:ASX) has a dominant position in designing and manufacturing medical devices for profoundly deaf people. In late March Cochlear announced a, A$880m capital raising at A$140 a share. As shown in the chart below, when markets peaked on 19th February, their share price was trading at A$251, but the lockdown induced by COVID-19 led to a suspension of elective surgeries. Accessing these types of offers is not always easy and the majority are taken up by institutional investors (including active fund managers) who can provide the quantum of support to ensure that the raising is well supported. Furthermore, equity raisings that receive strong demand often are only available to existing shareholders. Active fund managers view capital raises as an opportunity to increase their holding in companies that they consider good quality. If Cochlear can resume their trajectory once global lockdowns end and the backlog of surgeries provides immediate as well as long-term revenue, investors in the equity raise could receive outsize returns.

The yield trap

With the collapse of company earnings at least in the short-term, it is not surprising that many corporates have announced dividend cuts or deferrals. Australian companies pay out over 70% of their earnings on average, a much greater proportion than their global counterparts due to Australia’s imputation system. As such, the impact of dividend cuts is likely to be greater. Many investors faced with low deposit rates and low bond yields look to these dividends and franking credits as a source of income. Traditionally the banking sector has provided attractive yields, paying out up to 90% of their earnings but this is changing with NAB (NAB:ASX) the first of the Big 4 banks to announce a large dividend cut. Investors looking for income will need to look more broadly across sectors going forward. The reliability of this income is one of the factors managers consider when choosing stocks to add to their portfolio. If growth and acquisition opportunities are low, paying out dividends to shareholders is an efficient use of capital.

The uncertain outlook for the Australian economy is putting pressure on bank dividends as some companies seek to preserve capital. When Australia emerges from the current recession the outlook for the banks is likely to be closely tied to the fortunes of the Australian economy. Furthermore, it must be factored that APRA provided the following guidance on 7 April 2020 encouraging reduced distributions. “During this period, APRA expects that Authorised Deposit-Taking Institutions and insurers will seriously consider deferring decisions on the appropriate level of dividends until the outlook is clearer. However, where a Board is confident that they are able to approve a dividend before this, on the basis of robust stress testing results that have been discussed with APRA, this should nevertheless be at a materially reduced level.’’ How fast the Australian economy recovers will determine when those businesses and mortgage holders who have received deferral of interest will resume payments and when businesses look to grow and need credit again. This assessment of future earnings combined with an analysis of company cash flows and balance sheets is needed to determine the prospects for dividend yields looking forward. The following chart shows that expectations for dividends from Australian companies is at the lowest level since 2008.

In summary

The range of potential outcomes across industries has become more diverse. For those skilled in stock selection, the opportunity is ripe to pick up quality companies at a discount not envisaged at the start of the year. As panic sets in, sell-offs can be indiscriminate as the correlation between assets increases. Speculative companies yet to produce a profit often fall further than the overall market and struggle to raise finance reducing their probability of survival. Active investors will avoid those companies that they view inviable. Professional investors who have experience over market cycles not only consider the outlook for these types of stocks but often gravitate towards large caps in the early days of a crisis and small caps later in the cycle. Investing in a downturn can reward those whose analysis of company fundamentals can separate the wheat from the chaff and size the opportunity carefully. The stock selection process must be combined with portfolio construction. Sizing positions according to their perceived risk can help to provide risk management when it is needed the most. The beginning of a new market cycle and the uncertainty around the market outlook under the cloud of the COVID-19 pandemic provides active investors and professional fund managers opportunities that would not have seemed possible at the start of the year.

Never miss an insight

Stay up to date with our latest thoughts by hitting the follow button below. You can also visit our website for more insights from Fidante's various boutiques. .

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sinéad joined Fidante in January 2020 and has 17 years experience in the investment management industry. Her role is to serve as a conduit between the fund managers and the financial advisory community, with a special focus on retirement strategies.

Featuring

Sinéad Rafferty,

Fidante

Sinéad joined Fidante in January 2020 and has 17 years experience in the investment management industry. Her role is to serve as a conduit between the fund managers and the financial advisory community, with a special focus on retirement strategies.

3 stocks mentioned

Sinéad joined Fidante in January 2020 and has 17 years experience in the investment management industry. Her role is to serve as a conduit between the fund managers and the financial advisory community, with a special focus on retirement...

Comments

Comments

Sign In or Join Free to comment